Business owners often juggle day-to-day operations, future growth, and personal financial stability. Wealth management for business owners involves strategies to secure personal assets, plan for retirement, and address potential risks, all while preserving the business’s momentum. By exploring the following approaches, entrepreneurs can protect what they have worked hard to build and keep an eye on future goals.

Understand Wealth Management Basics

Wealth management focuses on creating and preserving assets through a combination of investment planning, estate strategies, risk management, and tax efficiency (Nesso Group). Business owners frequently face complex financial decisions, such as handling concentrated stock positions or deciding when to sell a company. They also benefit from a trusted advisor when evaluating whether they need private or fee-only professionals to handle intricate tasks like legacy planning and portfolio adjustments. Those curious about how broad these services can be may look into wealth management services for an in-depth overview.

Key Components

- Investment management: Allocating resources in ways that match personal and business objectives (Investopedia).

- Tax efficiency: Minimizing liability through careful planning, credits, or deductions (Instrumental Wealth).

- Estate planning: Mapping out a clear plan for transferring wealth to designated heirs (Central Trust Company).

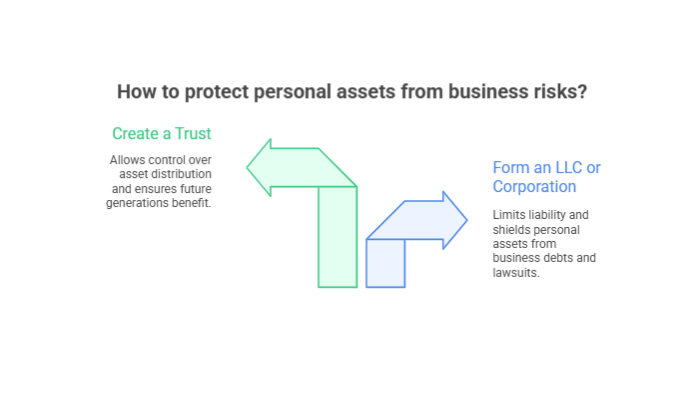

Protect Personal Assets

Separating personal and business finances is crucial for safeguarding wealth. Many entrepreneurs establish legal structures like limited liability companies (LLCs) or trusts to shield personal funds from business-related debts and lawsuits (Farther). These measures often help business owners maintain personal savings for future generations and reduce exposure to financial risk.

Possible Protection Methods

- Forming an LLC or corporation: Limits liability when unforeseen issues arise.

- Creating a trust: Allows business owners to set firm rules for asset distribution and maintain control during their lifetime.

Diversify Investments

Diversification goes beyond spreading funds between multiple business ventures. It can include stocks, bonds, real estate, or other alternative assets (Farther). Entrepreneurs are sometimes tempted to sink most of their wealth into their companies, yet balancing both personal and business portfolios can ease the impact of market volatility. According to Holborn Assets, risk tends to be lower when assets are spread out across different classes.

Approaches to Diversification

- Following an age-based guideline for asset allocation, such as the “100 minus age” rule (Investopedia).

- Rebalancing portfolios once or twice a year to maintain target allocations and risk levels (Investopedia).

Plan For Retirement

Retirement can look different for business owners, who frequently treat their companies as a main source of income. For those aiming to retire comfortably while maintaining an income flow, it is vital to coordinate personal and business finances or consider a partial sale. EP Wealth emphasizes how retirement planning should include potential sale timelines, business valuation, and the right time to transition ownership.

Long-Term Considerations

- Setting up retirement accounts, like Solo 401(k)s or SEP IRAs, to build a fallback fund (Harness).

- Consulting with credentialed advisors when determining how to balance tax obligations between personal and business interests (EP Wealth).

Address Risk And Estate Needs

Business owners face multiple forms of risk, from market volatility to interest rate fluctuations (Holborn Assets). Effective wealth management often includes insurance solutions for key individuals, legal safeguards through wills or trusts, and a plan to minimize estate taxes. Updating documents, especially after major life changes or business events, ensures smoother asset transitions (Central Trust Company).

Common Strategies

- Life and umbrella insurance: Protects family members and personal assets from unforeseen events (Central Trust Company).

- Succession planning: Ensures the business continues generating value, even if the owner retires or becomes incapacitated.

Recap And Next Steps

By protecting personal assets, diversifying investments, creating a solid retirement roadmap, and addressing risk, business owners can nurture lasting prosperity. Anyone unsure whether wealth strategies suit their unique circumstances can learn more in is wealth management worth it.

When it comes to wealth management for business owners, individuals often ask how it differs from basic financial planning, whether professional assistance is indispensable, what an appropriate level of risk tolerance looks like, how to set up effective retirement breakpoints, and how to secure personal assets in the most efficient way.

Staying proactive ensures that business owners can create a legacy for both their enterprises and their families. It may involve periodic reviews with trusted professionals, along with consistent adjustments to navigate shifting markets and life events. By doing so, they can enjoy peace of mind and focus on what they do best, knowing their wealth is in good hands.

Wealth Management in Los Angeles to Consider

Finding the right wealth management firm can make a lasting...

Wealth Management in New York to Consider

New York City stands as a global financial hub, attracting...