Many high-net-worth individuals often ask, “Is wealth management worth it?” Studies show that the average individual investor underperforms the broader market by a wide margin, earning about 3.69% annually over 30 years compared to the S&P 500’s average of 11.1% (MarketWatch). This gap arises from limited market knowledge, emotional decisions, and inadequate portfolio management. Wealth managers aim to address these issues by offering professional guidance, but does their expertise justify the cost?

Understand Wealth Management

Wealth management is a comprehensive approach to handling significant assets. It typically combines investment strategy, tax planning, estate planning, and more to protect and grow a client’s portfolio. Professionals in this field often have access to specialized data and research tools that guide better-informed decisions. Many experts argue that this knowledge advantage can reduce costly mistakes and lead to higher returns over time.

Why It Can Add Value

- A disciplined strategy helps investors avoid emotional buying or selling.

- Objective advice counters common biases such as loss aversion or confirmation bias.

- Studies from Vanguard and Russell Investments suggest a wealth manager may add 3% or more in annual returns (The Balance).

- Comprehensive services include portfolio diversification and estate planning, improving overall financial health.

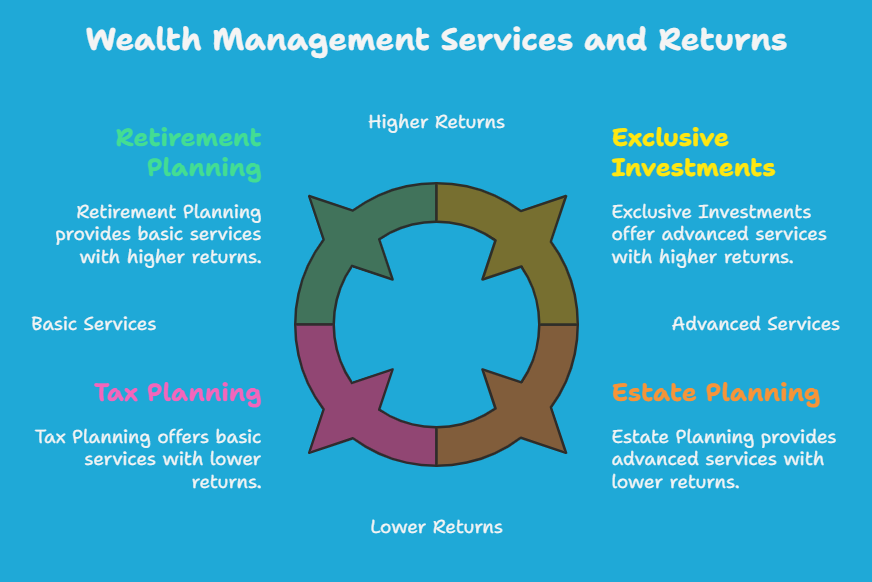

Key Services Offered

- Tax Planning: Minimizing liabilities through tax-loss harvesting and charitable-giving strategies (Amerant Bank).

- Estate Planning: Arranging wills and trusts to protect generational wealth and reduce estate taxes.

- Retirement Support: Ensuring distributions, pensions, and lifestyle expenses align with long-term goals.

- Access to Exclusive Investments: Hedge funds and private equity offerings can broaden potential gains (NerdWallet).

Weigh The Fees

Despite potential benefits, many individuals worry about wealth management fees. An annual charge of around 1% of assets under management (AUM) is common, though this rate can vary based on portfolio size. Such fees might appear steep, but wealth managers often bundle critical services like tax optimization, estate planning, and legal advice.

AUM Vs Other Structures

Wealth management costs may follow different models:

- AUM Fee: About 1% for moderate portfolios, dropping for larger sums (Long Angle).

- Flat or Retainer Fee: A set cost that covers specified services.

- Performance-Based Fee: Linked to investment gains, though less common in standard wealth management.

Some high-net-worth individuals split their assets between a wealth manager and a lower-fee brokerage, entering a cheaper fee tier while still receiving professional oversight (Long Angle). Investors also have the option to negotiate fees with prospective advisors if their portfolios exceed certain thresholds.

Consider The Alternatives

For individuals unwilling to pay a 1% AUM fee, alternatives like robo-advisors and self-directed investing exist. Robo-advisors charge around 0.25%–0.50% of AUM and often allow minimal account balances. Meanwhile, self-directed investors rely on personal research and online trading platforms.

| Aspect | Wealth Manager | Robo-Advisor | Self-Directed |

| Fees | ~1% of AUM | ~0.25–0.50% of AUM | Varies (commissions) |

| Minimum Investment | Often high | Low or none | Not applicable |

| Complexity Support | Comprehensive | Limited human input | Entirely individual |

When Professional Advice Matters

A professional approach is especially useful for high-net-worth individuals juggling complex assets, business income, or multigenerational estate plans. Managing these factors alone increases the risk of compliance errors, overlooked deductions, or missed opportunities for growth. Certain firms, such as Morgan Stanley, offer dedicated advisors as part of their wealth management services (Morgan Stanley). Individuals who want to understand minimum investment requirements may explore resources like wealth management minimum, which explains common thresholds for establishing professional relationships.

Decide If It Is Worth It

The true worth of a wealth management service depends on each individual’s financial complexity and comfort with self-directed investing. Professional guidance can provide discipline, sophisticated analysis, and holistic wealth planning. For those who prefer to maintain control while consulting an expert, reading about how to choose a wealth manager can clarify what to look for in a trusted advisory relationship. Others, particularly families prioritizing inheritance strategy, might explore family wealth managers to handle broader generational goals.

Ultimately, the decision stems from personal circumstances, including financial literacy, available time for portfolio oversight, and the desire for personalized support. If fees align with a manager’s expertise and the potential for improved returns, wealth management could be a worthwhile investment.

Frequently Asked Questions

- What Is the Typical Wealth Management Fee?

Many firms charge about 1% of assets under management, although fees may decrease for larger portfolios (Long Angle). Some charge flat or hourly fees instead. - How Do Wealth Managers Justify Their Cost?

They provide expert advice that taps into specialized knowledge, professional data sources, and disciplined investment strategies. Studies indicate these services may improve returns by about 3% annually (The Balance). - Do Wealth Managers Only Focus on Investments?

No. They often include tax strategies, estate planning, insurance reviews, and other services to address the broader financial picture (Amerant Bank). - Can Investors Negotiate Fees With Wealth Managers?

Yes. Individuals with substantial portfolios may find it easier to request lower rates or alternative fee structures due to higher investable assets (Long Angle). - Is Robo-Advisory a Comparable Substitute?

Robo-advisors can be less expensive and conveniently automated, but they may not offer in-depth guidance on complex financial needs or family wealth considerations (Investopedia).

Wealth Management in Los Angeles to Consider

Finding the right wealth management firm can make a lasting...

Wealth Management in New York to Consider

New York City stands as a global financial hub, attracting...