Is Fidelity a fiduciary? We understand that question is top-of-mind for many high net worth investors looking to preserve and grow their wealth. After all, having a fiduciary on your side can mean more transparent fees and a clear commitment to acting in your best interests. Today, we’ll take a closer look at Fidelity’s approach so you can make a more informed decision for your family’s financial future.

Even though Fidelity routinely serves many investors, its fiduciary status depends on the specific capacity in which the company operates. We’ll explore the nuances behind that structure and share tips on spotting the right fit for your high-touch, long-term wealth management needs.

Understand Fidelity’s Fiduciary Role

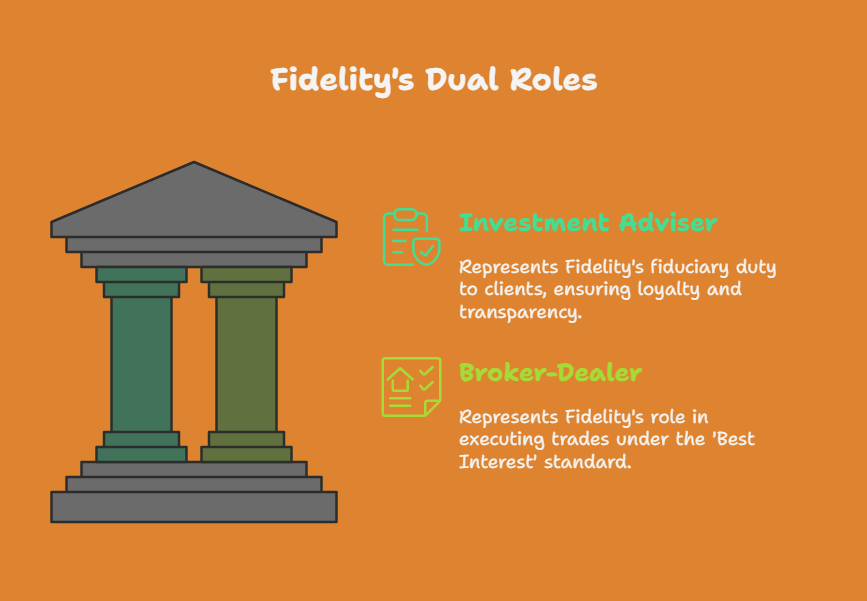

Fidelity can act as a fiduciary when it provides services under its investment adviser capacity. In those scenarios, Fidelity is generally regulated by the Investment Advisers Act of 1940. This means that, as an adviser, Fidelity must adhere to higher care and loyalty standards—putting client interests first at every turn.

However, Fidelity is not always bound by the fiduciary standard. When it serves clients as a broker-dealer (for instance, placing trades in a brokerage account at their direction), Fidelity often follows Regulation Best Interest (Reg BI). Reg BI requires brokers to act in a client’s best interest at the time of financial recommendations. It does not necessarily oblige them to assume fiduciary duties across every aspect of the client relationship.

Fidelity also notes that it does not provide legal or tax advice in any capacity. If you’re seeking counsel on trusts, estate planning, or tax strategy, it’s wise to consult an attorney or tax professional to navigate those specialized areas.

Different Standards For Brokers

Broker-dealers historically operated under a “suitability” standard, which stated that a recommended investment should suit the client’s financial situation and goals. In recent years, Regulation Best Interest (BI) has replaced or supplemented much of that standard, raising the bar for brokers. Yet Reg BI is still not as strict as the full fiduciary commitment, which requires advisers to put client welfare above their own profit motives at all times.

Meanwhile, the Department of Labor’s fiduciary rule—originally meant to hold anyone handling retirement accounts to a more comprehensive fiduciary standard—underwent a bumpy rollout. Parts of the rule were vacated by the courts, and additional proposals have been debated. For now, it’s up to each investor to confirm whether a provider truly operates under a fiduciary standard or a best-interest requirement for certain types of accounts.

What High Net Worth Investors Need

As high net worth investors, we want to be sure our wealth manager is consistently acting on our behalf. That’s where choosing a firm that clearly operates under a fiduciary standard can make a big difference. When a company charges fees based on assets under management—rather than on commissions from product sales—it helps reduce conflicts of interest.

Fidelity does offer fee-based advisory solutions, but you’ll want to confirm exactly how your specific account is structured. If you’re currently evaluating whether a wealth management relationship is the right move, you may also explore is wealth management worth it. And if you’re curious how another prominent firm measures up, be sure to check out is ameriprise a fiduciary.

Compare And Choose Wisely

Ultimately, deciding if Fidelity is your best fit means looking at the fine print. That includes reviewing the firm’s Form ADV (an SEC disclosure document) to see how they’re compensated and whether any conflicts of interest may crop up. High net worth individuals often benefit most from a provider who keeps sales, client service, and portfolio management in separate lanes—minimizing overlap and ensuring personalized attention.

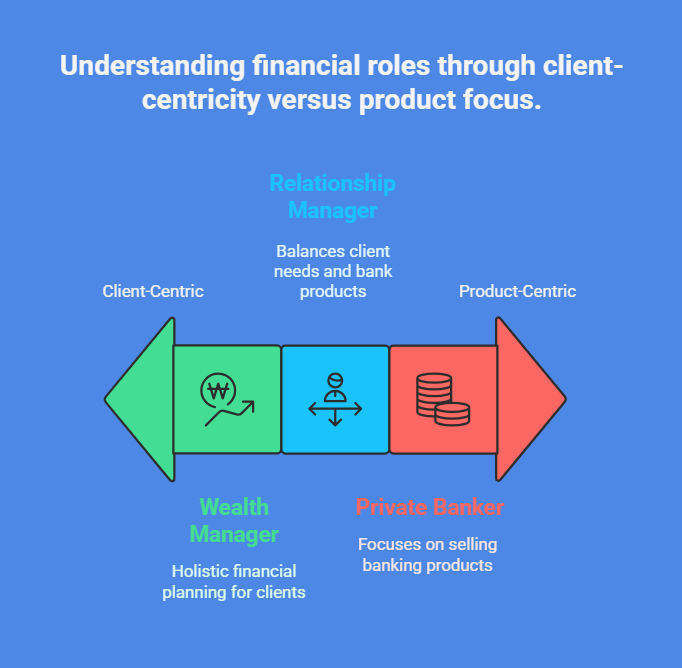

Of course, it’s more than just verifying fiduciary status. For a deeper dive into selecting the right advisory partner for your particular strategy, check out how to choose a wealth manager. You can also compare financial service roles, like private banker vs relationship manager, to better understand who best meets your needs.

Frequently Asked Questions

- Why does fiduciary status matter for high net worth investors?

Fiduciaries must place your interests above their own, which can foster greater trust and alignment with your long-term goals. This is especially important when large sums and complex assets are involved. - Can Fidelity be both a fiduciary and a broker-dealer?

Yes. Fidelity may act as a fiduciary under its investment adviser arm. However, it also functions as a broker-dealer, in which case it’s not necessarily held to the same fiduciary standard. - How do fees work under a fiduciary arrangement at Fidelity?

Typically, a fiduciary advisory service charges fees based on the assets it manages, rather than commissions from trades or product sales. This fee structure helps minimize conflicts of interest. - Is Fidelity a fiduciary for all retirement accounts?

Not automatically. While Fidelity follows Reg BI for brokerage accounts, certain advisory relationships may carry a fiduciary standard. Always confirm the specific arrangement you’re using. - What happens if a fiduciary fails to uphold their duties?

Breaching fiduciary duty can lead to legal and regulatory consequences. If you suspect fiduciary misconduct, you may want to contact legal counsel or the SEC to learn more about possible next steps.

We hope this discussion clarifies Fidelity’s fiduciary role and what it means for those of us seeking thorough, personalized wealth management. Whether you opt for Fidelity or another advisory firm, placing your trust in a fiduciary-centric model can help safeguard your assets for the long run. Remember to review service agreements, compare structures, and stay proactive about finding the best fit for your financial vision.

Wealth Management in Los Angeles to Consider

Finding the right wealth management firm can make a lasting...

Wealth Management in New York to Consider

New York City stands as a global financial hub, attracting...