I remember the moment I decided to get professional help with my finances and started looking into the cost of a financial advisor. It felt like stepping into a world of countless fee models, each more confusing than the last. I’m sharing what I’ve learned so you can make sense of it all more quickly than I did.

Discover Typical Advisor Costs

Before diving into details, it helps to know the industry ballpark. Traditional human advisors often charge around 1% of the assets they manage, while robo-advisors might come in lower, between 0.25% and 0.50% of assets under management (AUM) (NerdWallet). However, many advisors have minimum fees to ensure their time is well-compensated.

You’ll also find advisors who mix compensation structures. Fee-based advisors may charge both a percentage of AUM and earn commissions. Fee-only advisors generally do not earn any commissions. The cost can go up if you request more complex services, like a customized tax strategy or multi-generational planning.

Types Of Advisor Fees

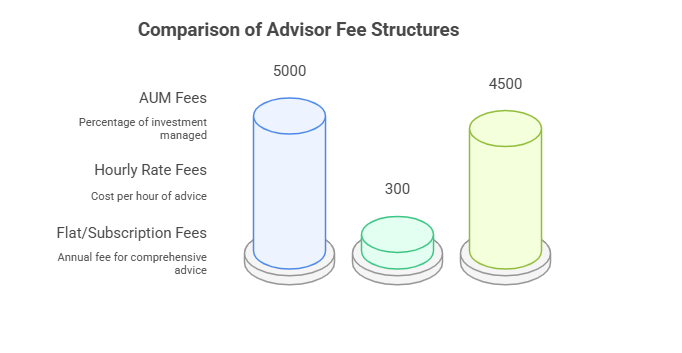

Asset Under Management (AUM) Fees

An AUM fee means you pay a percentage of what you invest for ongoing advice. For instance, if someone manages $500,000 at a 1% annual rate, the yearly cost comes to $5,000. According to the 2024 Kitces Report, many advisors use a graduated fee structure that starts around 1.00% for the first $1 million and shrinks for larger balances (SmartAsset). This setup often appeals to higher-net-worth individuals, but keep in mind bigger portfolios can lead to substantial fees, even if the percentage is the same.

Hourly Rate Fees

Some advisors charge by the hour, which can work well if you only need occasional advice. The median hourly fee as of 2024 is around $300, up from $250 a few years back (SmartAsset). This structure might suit you if you prefer to call the shots on your portfolio but still want an expert opinion from time to time.

Flat Or Subscription Fees

Flat fees or subscription-based arrangements can range from $2,000 to $7,500 annually (NerdWallet). While it might seem high, this approach can be efficient for people who want predictable bills and comprehensive advice. The 2024 Kitces Report shows subscription fees typically hover around $4,500 per year, although only 17% of firms rely on subscriptions alone (SmartAsset).

Consider Hidden Costs

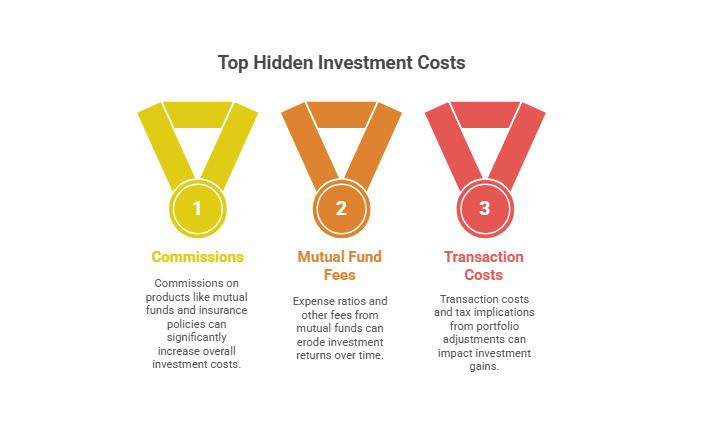

I learned that headline fees tell only half the story. Some advisors take commissions on certain products, and these can add up, especially when purchasing mutual funds or insurance policies. Fees from mutual funds, such as expense ratios, can quietly chip away at returns. If you’re curious, you can use an investment cost calculator or a mutual fund expense ratio calculator to see how these charges accumulate over time.

In addition, you might face:

- Transaction costs on trades.

- Tax implications when advisors adjust your portfolio.

- Flat fees for a detailed plan (averaging around $3,000 to $3,500) (SmartAsset).

It’s important to ask your advisor for a plain-English breakdown of what you’ll pay annually. For example, if you suspect add-on charges, check out how your advisor makes money. If you want a deeper look, consider reading about how do financial advisors earn money.

What I Learned

When I first sat down with an advisor, I discovered you can negotiate fee structures or at least clarify them. It took me a bit of courage to ask, but it was well worth the conversation. In the end, I decided a hybrid approach worked best: a flat fee for creating my overall plan, plus a modest AUM arrangement for day-to-day portfolio oversight.

I also realized it’s easy to underestimate the total cost if you only focus on a single number, like 1%. On a large portfolio, that can be significant money every year. At the same time, a good advisor might save you more than you pay by optimizing your investments or providing advanced strategies for tax efficiency. If you’re still curious, check out more insights here: how much does a financial advisor cost.

Five FAQs In One Sentence

People often ask: “What exactly is the cost of a financial advisor, which fee model is best, are fees ever negotiable, how do I compare advisors, and are fees tax deductible?”

(If you’re wondering about the last point, you might explore are investment management fees tax deductible.)

Final Thoughts

The cost of a financial advisor isn’t just a single figure, it’s a combination of fee structures and hidden expenses that can vary widely. If you want clarity on your own situation, ask plenty of questions about the advisor’s pricing, their revenue sources, and the type of services they include. In my case, I found that matching the right compensation model to my unique needs was well worth the time. It empowered me to focus on growing and safeguarding my assets, rather than constantly worrying about line-item fees. If you’re heading down this path, comparing different fee models and doing a bit of homework can make a noticeable difference in your long-term wealth strategy.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...