Meet The Mutual Fund Expense Ratio Calculator

If you’ve ever eyed a mutual fund and wondered how much you’re truly paying in fees, a mutual fund expense ratio calculator can be your new best friend. When it comes to this handy tool, you might ask yourself, “What exactly is it?,” “Why does it matter for my returns?,” “Is it reliable for every type of fund?,” “Am I missing fee waivers or reimbursements?,” or “How do I use these results to plan my investments?” By the end of this guide, you’ll have answers to all of these questions, plus an easy way to see if you’re on track to minimize unnecessary costs.

Understand The Basics Of Expense Ratios

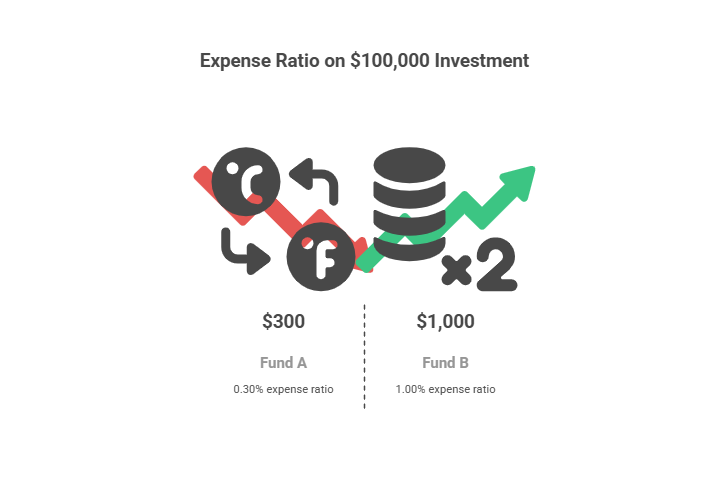

An expense ratio represents the percentage of your investment that goes toward covering a fund’s annual operating costs. According to Bankrate, a 0.30 percent ratio equals $30 per year for every $10,000 you invest. That might not sound dramatic until you compare funds charging 0.30 percent versus 1 percent. The first is just $300 on a $100,000 investment, while the second is $1,000—more than three times as much. Over multiple years, that difference can cost you thousands in lost returns.

How High Is Too High?

- If a fund’s expense ratio hovers above 1 percent, it’s often considered pricey.

- Many funds, especially passively managed index funds or ETFs, charge below 0.10 percent. Some even dip as low as 0 percent to lure cost-savvy investors.

Net Expense Ratio vs. Gross Expense Ratio

Some fund companies waive a portion of their fees, which lowers the net expense ratio you actually pay. For instance, a fund might advertise a gross expense ratio of 1.2 percent but then waive 0.3 percent, leaving you with a net expense ratio of 0.9 percent. It’s worth keeping an eye on fee waivers, because if they end, your fund’s costs can jump quickly.

Why Expense Ratios Matter

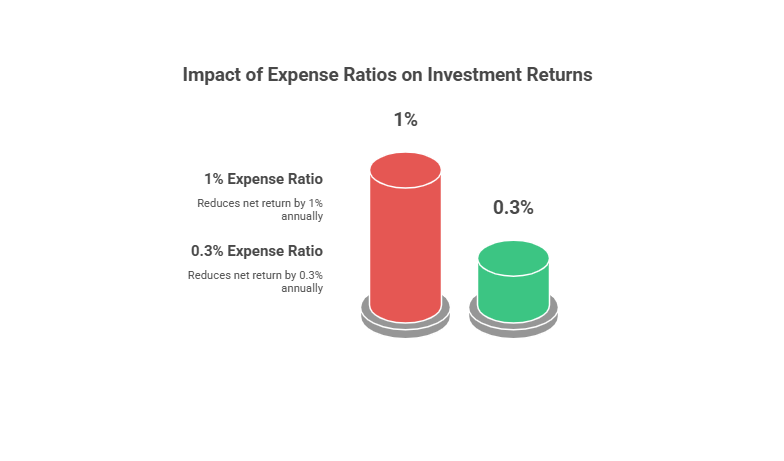

Expense ratios directly reduce your net return. If you earn 10 percent in a year but pay 1 percent in fees, your real take-home growth is closer to 9 percent. Over time, those extra percentage points compound, meaning a high expense ratio can erode your potential nest egg.

- A small difference in fees can add up: Investing $100,000 in a fund that charges 1 percent could cost you about $1,000 in the first year. In contrast, a 0.30 percent ratio would cost $300.

- Over 20 or 30 years, these seemingly tiny percentages can add up to hundreds of thousands of dollars in lost returns, especially for high-net-worth individuals who invest large sums.

Use A Calculator For Clarity

You do not need to be a math whiz to figure out your ongoing costs. A mutual fund expense ratio calculator shows how much of your money goes toward fees annually, and how that figure compounds over time. Numerous sites, including Nerdwallet, offer such tools.

Inputs You Need

- Initial Investment: How much you’re putting into the mutual fund from the get-go.

- Annual Contribution (If Any): Are you adding extra money each year?

- Estimated Return: Your expected yearly growth rate for the fund.

- Expense Ratio: The key figure you’re trying to track and compare.

Reading The Results

The calculator will typically show:

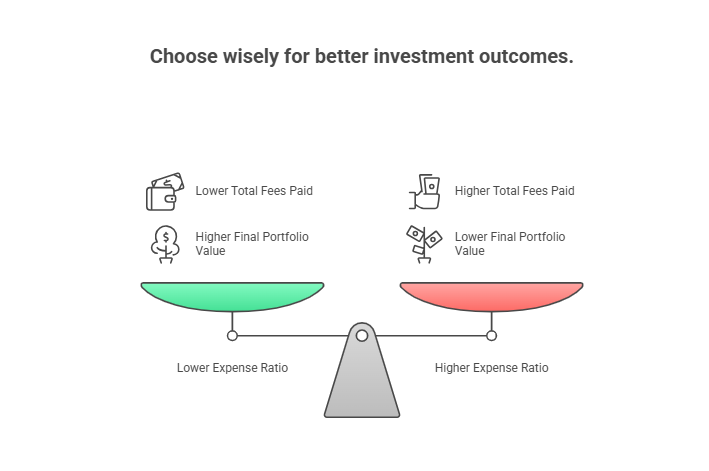

- Total fees paid over a set period.

- The final portfolio value after accounting for these fees.

- How your returns would look if you paid a different expense ratio.

If you spot high costs, consider exploring alternatives with a lower ratio, such as certain index funds or ETFs with expense ratios around 0.05 percent. You could also talk with a fiduciary advisor about strategies to reduce investment-related fees. And if you’re curious whether your broader advisor costs are fair, you may want to learn more about the cost of a financial advisor.

Minimize Fees For Better Returns

Keeping more of your money invested can help you achieve long-term goals, whether that’s to protect your business assets or secure a comfortable retirement. Here are a few tips:

- Shop Around: Sometimes, two funds tracking the same index can have vastly different expense ratios.

- Check For Waivers: Keep an eye on net expense ratios that might change if waivers are removed.

- Compare Active vs. Passive: Actively managed funds can charge 0.75–1.5 percent, while passive index funds may dip below 0.10 percent.

- Use Tools Routinely: A mutual fund expense ratio calculator or an investment cost calculator is worth revisiting every year to see if new, cheaper options emerge.

Plan Your Long-Term Strategy

By focusing on lower-cost investments, you can preserve more of your returns and reinvest them. Over time, that margin of growth can be massive. For major wealth-building efforts, such as managing concentrated stock holdings or navigating a liquidity event, a fee-only advisor can tailor strategies that optimize tax efficiency and reduce costs. You might also explore whether are investment management fees tax deductible. It’s all part of making sure your money works harder for you—not for the fund company.

Have questions or experiences with comparing fund fees? Share your thoughts in the comments. Reducing costs now can pay dividends for decades to come. When you put the numbers into a mutual fund expense ratio calculator, you’ll see just how powerful a fraction of a percent can be. Enjoy the extra savings as you build your financial future!

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...