We often wonder, how much does a financial advisor cost, especially when we’re aiming to protect and grow our nest egg. The truth is, there isn’t a one-size-fits-all answer. That said, we can walk through a few practical steps that help us see if the price tag is worth the peace of mind and potential returns.

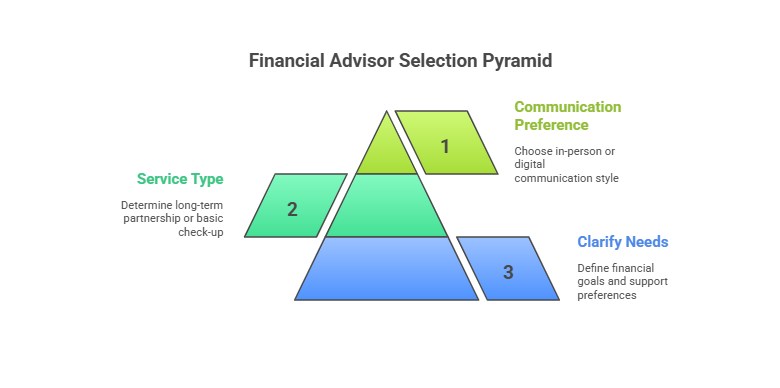

Step 1: Clarify Your Needs

Before diving into numbers, let’s figure out what we actually want from an advisor. Are we seeking a long-term wealth management partner, or do we just need a basic check-up for our portfolio? This is important because different advisory services come with different price points.

- Make a short list of your primary financial goals (retirement planning, business liquidity events, estate strategies).

- Decide if you need ongoing support or a one-time consultation.

- Ask yourself if you prefer in-person meetings or if digital communication works fine.

If you’re curious about how advisors typically earn revenue, check out our guide on how do financial advisors earn money.

Step 2: Compare Fee Structures

Financial advisors typically use one or more of these main models:

- Assets Under Management (AUM): A percentage of the total assets they manage, often 0.25% to 2% per year (NerdWallet).

- Flat or Retainer Fee: A set amount (for example, $3,000 annually), which may be best for complex financial situations.

- Hourly: Rates often range from $200 to $400 per hour.

- Commission: Fees earned through product sales, commonly 3% to 6% of the investment amount.

According to Kitces, 92% of firms incorporate AUM fees in some way. We should weigh each option based on our unique situation and comfort level.

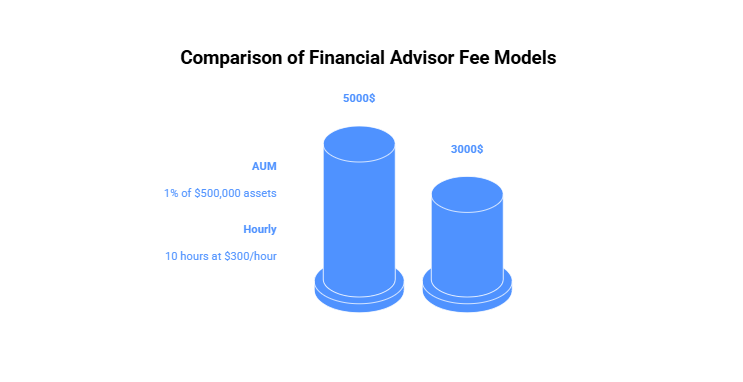

Step 3: Calculate Your Costs

Once you have a sense of which fee model interests you, the next step is simple math. For AUM, multiply your assets by the advisor’s percentage. If you’re leaning toward hourly or retainers, estimate how many hours of planning you might need per year or how many months of service you want.

- AUM example: 1% of $500,000 is $5,000 yearly.

- Hourly example: 10 hours at $300/hour is $3,000.

Need extra help? Try running quick figures with our investment cost calculator to see how different fee percentages might impact you.

Step 4: Protect Yourself From Extras

It’s not just about the primary advisory cost. Occasionally, there are product fees, trading fees, or wrap fees that can sneak onto your bill.

- Read your contract to ensure you understand trading costs.

- Check if overhead expenses or platform fees are included.

- If you want to consider tax implications, see our resource on are investment management fees tax deductible.

A little upfront detective work can help you avoid surprises later.

Step 5: Weigh Price Against Value

Ultimately, the best financial advisor for us balances fair costs with exceptional service. Some advisors might charge slightly more but offer deeper strategic planning, estate advice, or increased personal attention.

- Compare potential gains vs. fees paid.

- Check whether the advisor is fee-only or fee-based, especially if fiduciary standards matter to you.

- Remember that trust, long-term growth, and reduced stress can be worth a premium fee.

We should always prioritize an advisor who aligns with our goals, even if their quote is a bit higher.

Conclusion

You might still have questions like: do retainer fees vary by location, can advisor costs be deducted for taxes, do advisors charge a commission for each trade, is a flat fee CFP model a better deal, or how much do senior financial analysts typically earn?

By clarifying our goals, exploring different fee models, calculating potential expenses, checking for hidden charges, and comparing payoff vs. price, we’re in a strong position to decide if hiring a financial advisor makes sense. If the numbers add up and the advisor’s expertise meets our standards, the investment can be truly worthwhile.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...