You’re probably wondering how do financial advisors earn money and whether their compensation aligns with your best interests. The short answer: advisors can get paid through commissions, fees, or a blend of both. Let’s dig into each approach, so you can figure out what works best for you. This quick tutorial walks you through five steps, offering tips and a few handy resources.

Step 1: Know The Main Structures

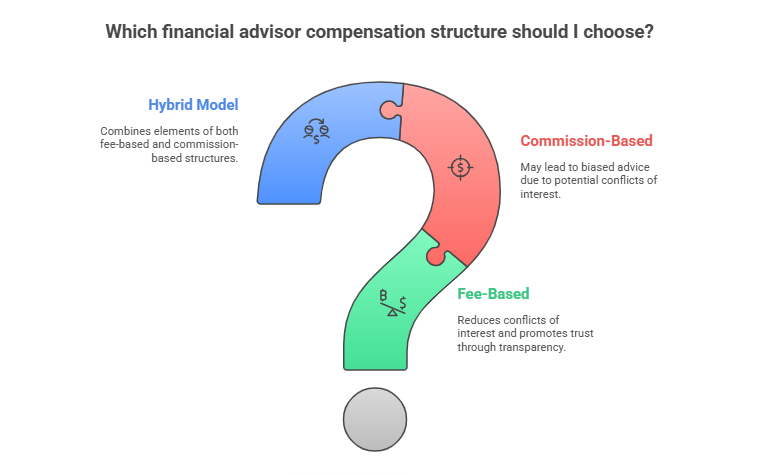

Before you hire someone to advise you on your finances, it helps to know the different ways they get paid. Each structure comes with its own upsides and potential pitfalls. And yes, it can affect the advice you receive.

Why Structure Matters

- Each compensation model shapes how an advisor thinks about your portfolio.

- Some structures reduce conflicts of interest more than others.

- It’s easier to trust guidance when you understand what’s driving it.

If you’d like a deeper dive into the cost of an advisor, check out this quick read on the cost of a financial advisor.

Step 2: Explore Commission-Based Models

Commission-based advisors earn money whenever they sell certain products, like insurance policies or mutual funds. You might never see an upfront bill for their service, but the advisor gets a cut from the transaction. According to Investopedia, these commissions can go from 3% up to 6% of your investment.

Common Commission Rates

- Mutual funds often have loads (a percentage fee) at purchase or sale.

- Insurance products like annuities sometimes pay out higher commissions, around 5–6%.

- These can add up if you make multiple transactions.

Commission-based advisors might be a fit if you rarely trade or need specific products. But they can face pressure to sell items that generate higher commissions, which can be at odds with your best interests.

Step 3: Understand Fee-Based Models

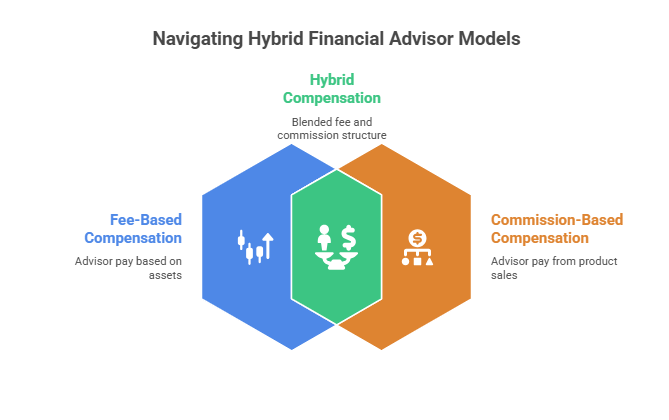

Fee-based advisors charge you a fee—often a percentage of your assets under management (AUM)—but they may also get commissions from certain products. This hybrid setup can offer holistic financial planning, yet there’s a potential conflict: part of their pay could still come from product sales.

Potential Conflicts Of Interest

- Additional incentives may nudge an advisor toward one product versus another.

- Make sure you confirm if commissions factor into their recommendations.

- Always ask if they’re acting as a fiduciary, which requires them to put your interests first.

If you want to see how ongoing fees might affect your investments, you could give our investment cost calculator a try.

Step 4: Dive Into Fee-Only Models

Fee-only advisors, on the other hand, charge purely for their advice—either as an hourly rate, flat project fee, or a percentage of your AUM. They don’t earn commissions from financial products. Because they aren’t financially incentivized to promote a particular investment, they tend to face fewer conflicts of interest.

- Hourly fees make sense if you want one-off consultations.

- Flat fees or retainers can be budget-friendly if you need ongoing support.

- AUM fees often hover around 1% for human advisors (per Nerdwallet) but may scale down for high-net-worth portfolios.

If you’re curious about whether certain costs could be deducted during tax season, you might glance at this piece on are investment management fees tax deductible.

Step 5: Put It All Together

Now that you’ve explored these models, it’s time to figure out which one matches your financial situation. Ask yourself what kind of help you need—comprehensive planning, product recommendations, or both. Then, compare costs and conflicts. Remember to factor in your level of comfort with each approach.

Here’s a one-sentence FAQ covering five common questions at once: “How do financial advisors earn money, are they required to act in your best interest, can you negotiate lower fees, is fee-only better than commission-based, and do you pay more for a fiduciary?”

Ultimately, the right advisor will make you feel listened to, present transparent costs, and deliver solid guidance based on your personal goals. If you want to drill even deeper into the numbers, you can explore how much does a financial advisor cost.

Feel free to keep this tutorial handy for your next advisor meeting, and don’t hesitate to ask direct questions about how they get compensated. After all, it’s your money and your future.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...