When I dive into retirement planning for specific professions, I realize there is no one-size-fits-all approach. Different careers, job demands, and benefit structures create unique challenges that call for specialized strategies. Below, I’ve put together a quick list of seven professions and some key considerations to help you shape a retirement strategy tailored to your work life.

Support Teachers With 403(b)s

Teachers typically rely on state pension systems, such as a State Teacher Retirement System (STRS). However, many districts also offer 403(b) plans, which can provide a valuable supplement for long-term savings (PlanMember). These plans often feature a roster of vendors, so it’s wise to compare fees and investment choices before enrolling. If you’re curious how a 401(k) might fit in as well, you can check resources like do teachers have 401k to see what options might exist.

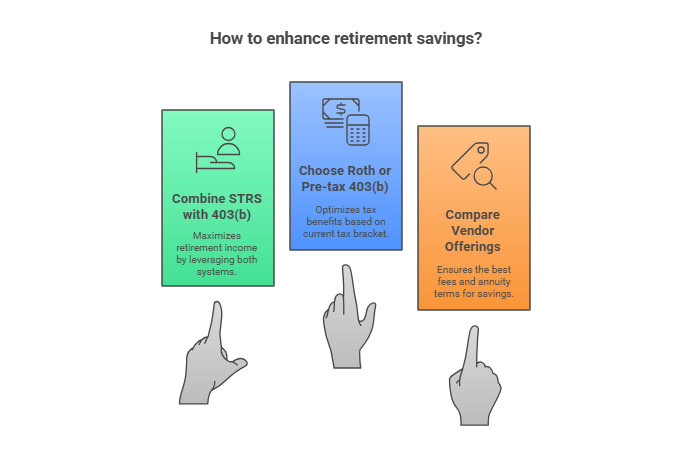

- Look into combining STRS with a 403(b) plan to boost total retirement income.

- Consider whether a Roth or pre-tax 403(b) contribution aligns better with your tax bracket.

- Compare vendor offerings carefully, especially regarding fees and annuity terms.

Shield Professional Athletes

Professional athletes face short career spans and sudden wealth, which can unravel quickly without disciplined planning. According to Athlete Family Office, challenges often include family pressure, lavish spending, and a lack of financial literacy. Careful budgeting, smart investment strategies, and early collaboration with a trusted advisor can help maintain multi-generational wealth.

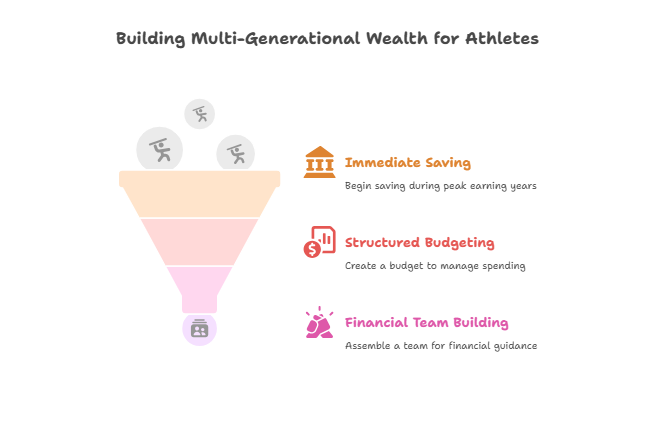

- Start saving immediately during peak earning years, typically the early-to-mid career stage.

- Create a structured allowance to avoid overspending on luxury items.

- Build a financial team for ongoing guidance, including data-driven investing and estate planning.

Assist Physical Workers

Physical laborers, such as construction or manufacturing employees, often find it harder to work until a traditional retirement age due to the demands of their jobs. Research from the Transamerica Institute highlights the need to plan ahead and possibly transition to lighter roles if health concerns arise.

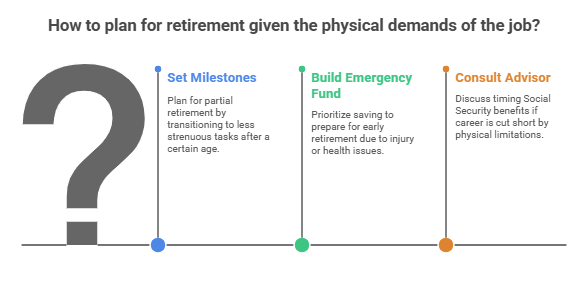

- Set milestones for partial retirement, like shifting to less strenuous tasks after a certain age.

- Prioritize building an emergency fund in case an injury or health issue fast-tracks retirement.

- Talk to a retirement advisor about timing Social Security benefits if your career is curtailed by physical limitations.

Help Freelancers Adapt

Freelancers juggle irregular incomes and lack employer-sponsored benefits. A combination of budgeting, large emergency funds, and accounts such as IRAs can create stability even when revenue fluctuates (First Commonwealth Credit Union, Sidepocket). Explore the best retirement plan for self employed if you want to maximize tax advantages.

- Track your income cycles, and set aside a consistent percentage for savings each month.

- Choose flexible retirement accounts, such as a SEP IRA, to adapt contributions when income is high or low.

- Keep three to six months of living expenses on hand to cover gaps between projects.

Bolster Healthcare Workers

Healthcare professionals often face demanding schedules, and the sector is projected to experience a significant workforce shortage (NCBI). This can mean extra hours, stress, and delayed retirement if understaffed facilities rely heavily on veteran workers. Planning for retirement in this environment might involve considering extended career paths or phased retirement options.

- Map out retirement timelines that account for the possibility of working longer due to staff shortages.

- Evaluate available retirement plans, such as employer-based 403(b) or 401(k), and check vesting schedules.

- Factor in the potential for health challenges related to prolonged shifts and high-stress roles.

Aid Nonprofit Employees

Workers in nonprofit organizations can access tailored 401(k) or 403(b) plans, but coverage may vary. According to some industry data, nonprofits often face budget constraints that limit match contributions. If you’re in this sector, consider 401k for nonprofit options where you can compare plan fees, employer matches, and the overall investment lineup.

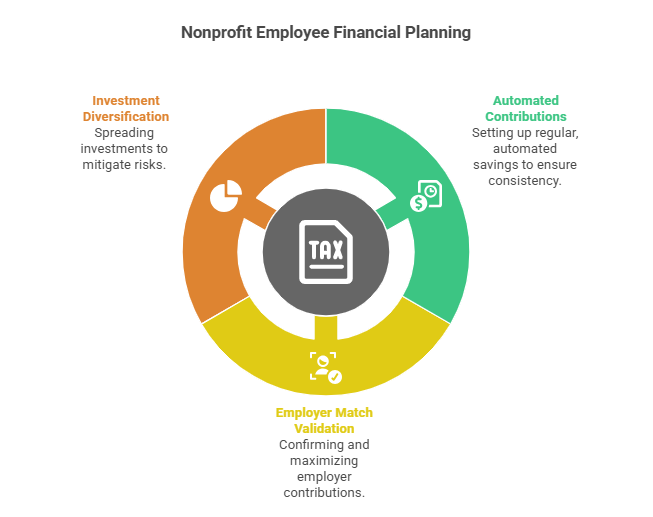

- Look into automated contributions to ensure a consistent savings habit.

- Validate the status of any employer match or profit-sharing, and contribute enough to capture full benefits.

- Diversify your investments to offset potential pay stagnation in tight-budget nonprofits.

Guide Self-Employed Owners

Business owners, including those operating S corporations, might have to juggle payroll, taxes, and retirement planning all at once. It pays to explore s corp retirement plan options early to maximize your tax efficiency. By setting a steady contribution schedule, you create a personal pension that isn’t tied to your company’s fluctuating fortunes.

- Investigate profit-sharing or cash balance plans if your business has consistent revenue.

- Consider combining a Solo 401(k) with employer profit-sharing contributions.

- Revisit the plan each year to adjust for business performance and personal goals.

Conclusion

I often get asked five big questions about retirement planning for specific professions in a single breath, such as “How do teachers coordinate 403(b) plans with 401(k) options, can physical workers retire early without straining finances, what’s the best approach for sudden wealth as a pro athlete, how do freelancers steady their savings amid income swings, and when should healthcare workers start adjusting for potential workforce shortages?” The bottom line is that each profession demands nuance and forethought. Talk with a certified retirement planner if you need a personalized approach, and don’t wait until the last minute to start. Your future self will thank you.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...