Explore Teacher 401(k) Options

Do teachers have 401k plans, and how do they fit into a broader retirement strategy? We often encounter this question when discussing financial security with educators. While many public school teachers rely on 403(b) accounts or traditional pension plans, there are situations where a teacher might still access a 401(k). Let’s walk through the essentials, from key eligibility points to comparing these different savings vehicles.

Why Some Teachers Access 401(k)s

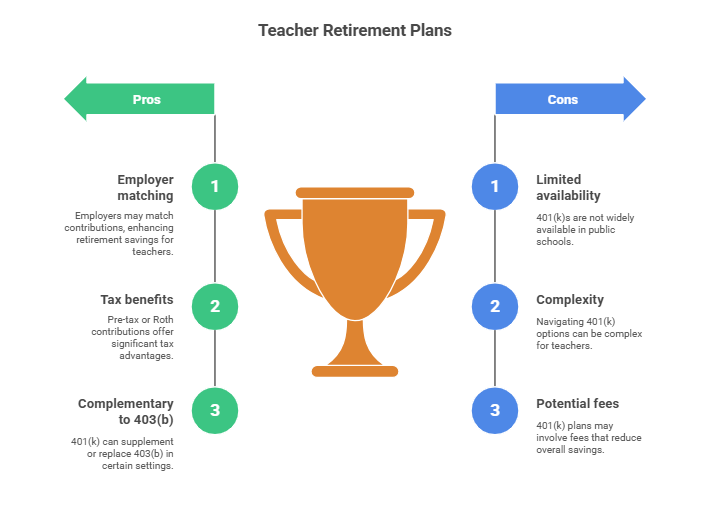

Educators working in for-profit or certain tax-exempt private schools can be offered a 401(k) plan. This plan allows pre-tax (or sometimes Roth) contributions, and employers may provide matching funds to encourage participation. According to the IRS (IRS), a 401(k) is a qualified profit-sharing plan that employees can fund directly out of their wages. For teachers in these settings, a 401(k) can complement or, in some cases, replace a 403(b).

The Role of 403(b)s in Public Schools

In most public schools, 403(b) accounts are the main defined-contribution option. A 403(b) plan is structurally similar to a 401(k), allowing tax-deferred growth on contributions, but it’s generally exclusive to public educational institutions and nonprofit organizations (Investopedia). Although many teachers assume public school employment means no 401(k), that’s not always true: for-profit charter schools or private institutions can still provide a 401(k).

Compare 403(b) And 401(k)

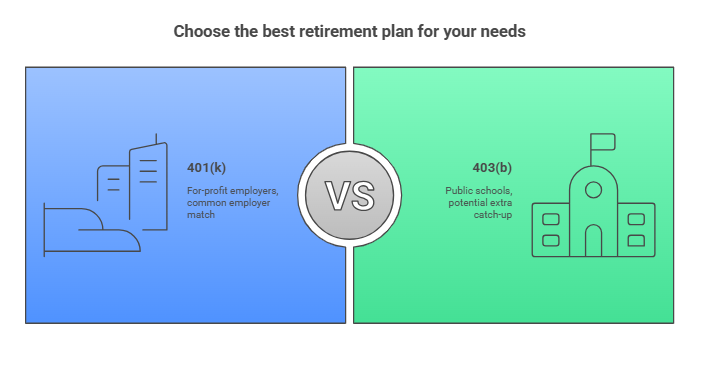

Comparing 403(b) and 401(k) can be helpful when planning your retirement path as an educator. Both are employer-sponsored defined-contribution plans, but they carry some differences.

| Plan Type | Typical Sponsor | Key Advantages | Unique Catch-Up Contributions |

| 401(k) | For-profit employers, some private or charter schools | Employer match is often common | Standard catch-up for age 50+ |

| 403(b) | Public schools, nonprofits | Easier access for educators, potential extra catch-up for long-standing employees | Special 15-year service catch-up plus age 50+ catch-up |

Teachers can choose to participate in either plan if both are offered, as long as they respect overall annual contribution limits. In 2022, the elective deferral cap was $20,500 for each plan, with an additional $6,500 if you were age 50 or older (Beagle).

Evaluate Pension Versus Defined Contributions

Many teachers still enjoy a pension, especially if they remain in one district for decades. Pensions promise guaranteed payouts and, according to the UC Berkeley Labor Center, can often provide more valuable benefits than an “idealized” 401(k) for certain long-tenured educators (UC Berkeley Labor Center). However, newer tiers in some states provide reduced benefits, shifting more responsibility onto the teacher to build personal retirement savings through 401(k)s, 403(b)s, or other supplemental accounts.

Considering Social Security Gaps

Around 40% of public school teachers do not pay into Social Security. That means some educators may not receive Social Security payments in retirement (Investopedia). If that’s you, then investing in a 401(k) (when available) or 403(b) becomes even more critical to ensure a comfortable retirement.

Consider Special Catch-Ups

Extra Contributions in a 403(b)

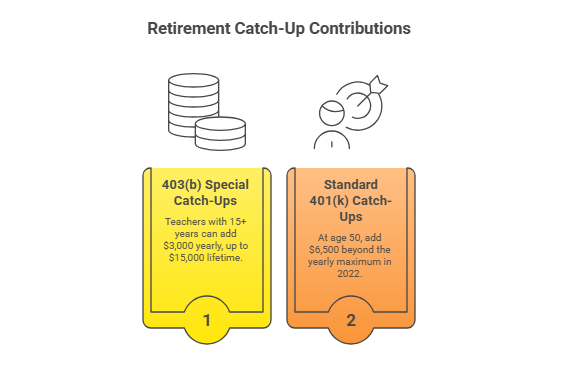

For teachers who’ve worked 15 or more years with the same employer, some 403(b) plans allow an additional $3,000 per year, up to a $15,000 lifetime limit, on top of the regular age-based catch-up. This feature does not exist in 401(k) plans (Beagle). If you’re approaching the end of a long teaching career, it can significantly increase your retirement nest egg.

Standard 401(k) Catch-Ups

Meanwhile, 401(k)s permit a “standard” catch-up once you reach age 50. In 2022, you could add another $6,500 beyond the yearly maximum (Investopedia). If you have the option of both a 401(k) and a 403(b), you can leverage their respective limits to maximize total contributions if your budget allows.

Avoid Hidden 403(b) Fees

One reason some educators prefer a 401(k) is that many 403(b) plans are not covered by ERISA’s safeguards, which can lead to higher fees and less transparency (GAO). That said, it depends on school district regulations and state laws, since some states impose strict oversight on 403(b) offerings to protect teachers from excessive costs.

Plan For The Future

We remind all high-net-worth families, especially those in the education sector, that retirement choices aren’t one-size-fits-all. Here are a few tips:

- Combine Plans If Feasible

You might be able to maximize your contributions by pairing a 403(b) with another defined-contribution plan if your employer offers both. - Review Pension vs. Personal Savings

Even with a valuable pension, calculating additional savings can help you avoid gaps in retirement funding. - Seek Professional Guidance

Every teacher’s situation is unique. Talking with a retirement advisor or a certified retirement planner can clarify how 401(k), 403(b), and pension plans fit into a long-term strategy.

If you’d like more insights on planning for educators, check out our resources on retirement planning for specific professions.

Conclusion

Whether 401(k), 403(b), or a traditional pension, teachers have several paths to build a secure retirement. We’ve seen that a 401(k) may be possible under for-profit private or charter schools, while public school teachers typically rely on 403(b)s and pension systems. In one sentence, five FAQs many educators ask are: “Do teachers have 401k, can they contribute to both 401k and 403(b), do they pay Social Security, how does a pension compare, and are catch-up contributions available?” We hope this article clarifies how each plan works and helps you choose the best approach for your financial future. If you’re still unsure, we encourage you to explore all available options and reach out for guidance.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...