Understanding Certified Retirement Planners

Anyone planning for long-term financial security may encounter the term certified retirement planner early in the process. A professional with specialized credentials in retirement income strategies can help individuals secure reliable cash flow, manage taxes, and protect assets. High-net-worth families, in particular, often look to these experts for objective guidance on preserving wealth across generations.

Certified retirement planners hold designations that indicate rigorous training, exams, and ethical standards. While FINRA does not endorse or approve credentials, it does list recognized designations, such as the Certified Specialist in Retirement Planning (CSRP) and the Certified Retirement Counselor (CRC) (FINRA). By reviewing these listings, individuals gain clarity on each certification’s requirements and scope.

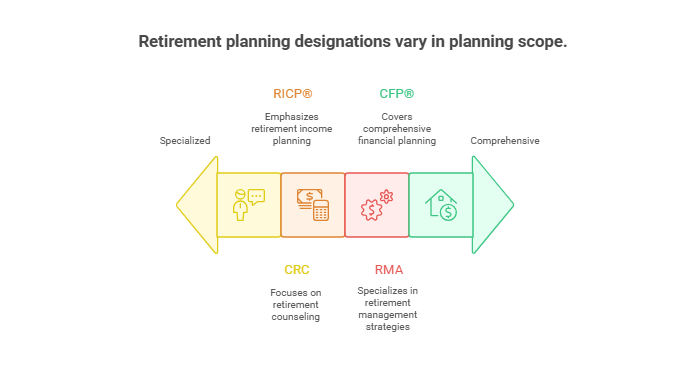

Comparing Popular Designations

Designations in retirement planning vary in focus, depth, and prerequisites. From the CERTIFIED FINANCIAL PLANNER™ (CFP®) mark to the Retirement Income Certified Professional® (RICP®) and others, each has a unique emphasis. The table below highlights four well-known credentials:

| Designation | Main Focus | Key Requirements |

| CFP® | Comprehensive Financial Planning | College-level coursework, pass certification exam, meet experience/ethics standards |

| CRC | Specialized Retirement Counseling | Proctored exam, continuing education, experience requirements (FINRA) |

| RICP® | Retirement Income Planning | Three online courses, or two if CFP®/ChFC®, plus experience (The American College) |

| RMA | Detailed Retirement Management | Specialized training on retirement strategies, exams, and ongoing education |

Each credential indicates additional study in investments, retirement risk management, and income distribution. Although the CFP® exam touches on retirement topics, only about 18% of its content centers on retirement-specific strategies, so certifications like the RICP® drill deeper into retirement income processes.

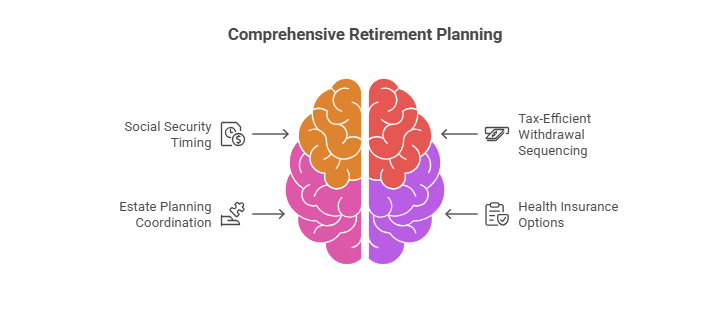

Recognizing Specialized Training

Working with a retirement-focused professional can be especially valuable for those nearing or in retirement. In many cases, these specialists advise on:

- Social Security timing

- Tax-efficient withdrawal sequencing

- Coordinating estate planning elements

- Assessing health insurance options after age 65

According to some advisory firms, a retirement planner may run hundreds of individualized scenarios each year, seeking to preserve capital while ensuring steady cash flow. Such a nuanced process goes beyond creating a traditional accumulation-focused plan.

Evaluating Fee-Only Advisors

Many high-net-worth individuals prefer a fee-only structure. Fee-only planners do not receive commissions from financial products, which can help preserve objectivity. For those concerned about conflicts of interest, it may be wise to consult a fee-only retirement advisor to avoid product-driven recommendations and instead focus on comprehensive wealth strategies.

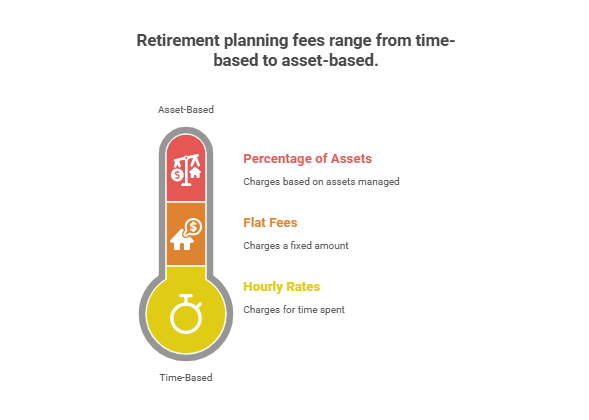

Examining Costs And Value

Fees for retirement planning services might follow multiple models:

- Hourly rates

- Flat fees for a complete retirement income plan

- A percentage of assets under management

Professionals often charge around 1% of managed assets or a few thousand dollars for a one-time plan, though this can vary depending on the advisor’s specialties and the complexity of the client’s portfolio. In return, individuals gain personalized strategies designed to address longevity risk, inflation, and changing market conditions.

Conclusion And Next Steps

A certified retirement planner can guide families and executives through the complexities of retirement income strategies, ultimately offering confidence in their financial outlook. Whether exploring an RICP® program’s in-depth training or relying on an experienced CFP®, individuals often benefit from specialized insights into tax efficiency, estate structures, and ongoing adjustments to ensure a sustainable income stream well into the golden years.

In a single sentence, five key questions prospective clients often ask about a certified retirement planner include clarifications on what sets them apart, how they structure fees, which credentials they hold, the scope of their retirement focus, and the potential impact on an individual’s broader financial goals.

Those seeking advice on a targeted career path might explore more specialized content on retirement planning for specific professions. Whether someone is self-employed, a teacher, or a corporate leader, tapping into a retirement professional’s expertise can deliver tailored strategies for lasting financial security.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...