I’ve come to realize that retirement planning basics matter deeply to my financial future, especially as I juggle current responsibilities and envision the next stage of my life. By getting a handle on saving, investing, and strategizing early on, I can give myself a better chance of enjoying the flexibility and security that many people crave when they step away from full-time work.

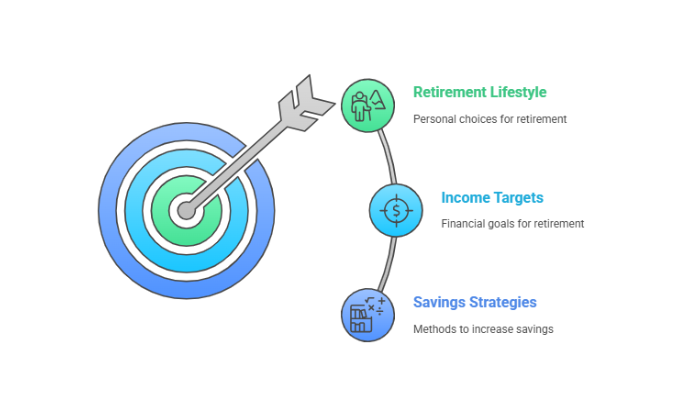

Defining My Retirement Goals

I like thinking of my retirement in terms of personal lifestyle choices—where will I live, what will I do every morning, and how often can I travel? Understanding why retirement matters to me helps frame my goals. For instance, if I want to keep a dynamic lifestyle or continue supporting loved ones, I need to get honest about my saving and spending habits today.

Depending on my objectives, I might start exploring why it’s essential to plan ahead by reading more about why is retirement important and figuring out how each financial decision might help me stay on track.

Setting Income Targets

From what I’ve researched, Fidelity suggests saving around 15% of my income each year, including any employer match (Fidelity). That number offers a good starting point to potentially reach 10 times my salary by age 67, but I understand it’s just a benchmark. My personal circumstances (like changing jobs or facing unexpected events) might mean I need to save even more.

Here are a few ways I’m looking at to raise my savings rate:

- Automate contributions so I never miss a deposit.

- Funnel extra money (like annual bonuses) directly into my nest egg.

- Use a retirement planning checklist to make sure I’m not skipping vital steps.

Choosing My Ideal Savings Accounts

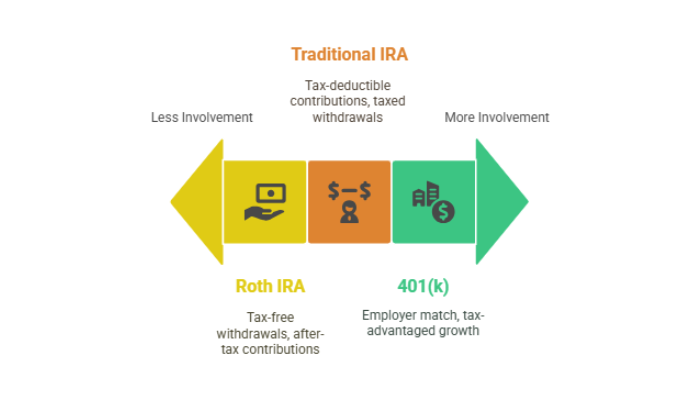

As I start saving, I recognize there are multiple account types that can help my money grow. The two big players are 401(k)s and IRAs, but other options exist if I’m self-employed or work for certain types of organizations.

401(k) Plans

My employer-sponsored 401(k) allows me to invest part of each paycheck in a tax-advantaged account. Employers often match my contributions up to a certain percentage, which is basically free money. Though I must keep an eye on early withdrawal penalties, I appreciate how these plans can accelerate my savings.

IRAs (Traditional, Roth, SEP, and More)

The IRA family has something for almost every situation. Traditional IRAs might let me make tax-deductible contributions, while Roth IRAs use after-tax dollars, giving me tax-free withdrawals later. For small business owners, SEP or SIMPLE IRAs might be more appropriate. Each account has its own rules, and if I handle them well, they can offer more control over my investment mix (Equifax).

Considering Other Options

If I work for a nonprofit or government entity, 403(b) or 457(b) plans might be relevant. Some companies also provide Employee Stock Ownership Plans (ESOPs). If I’m feeling overwhelmed, I can reach out to retirement income planners for guidance and a tailored plan.

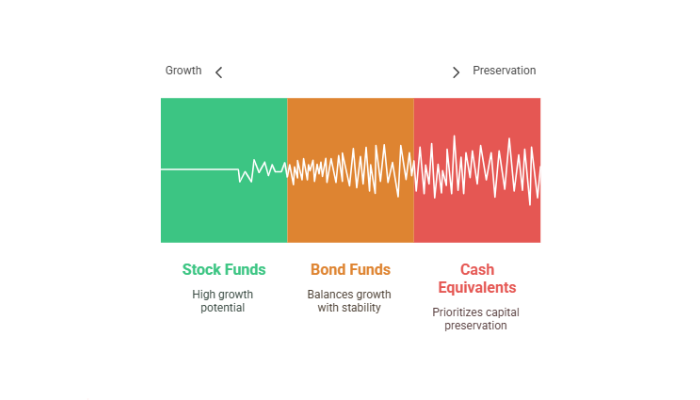

Structuring My Investments Wisely

Saving is half the battle. The other critical piece is deciding how to invest. Early on, it’s tempting to chase higher returns, but as I get closer to retirement, I’ll likely want to dial down the risk.

Allocating for Growth and Preservation

- Keep a mix of stock funds for long-term growth and bond funds or cash equivalents for stability.

- Make sure I rebalance my portfolio annually, especially if the market has been shaky.

- If I’m uncertain, I can chat with a Financial Advisor, according to Morgan Stanley’s guidance on pragmatic retirement investing (Morgan Stanley).

Understanding My Withdrawal Strategy

A proper drawdown approach ensures I don’t outlive my money. For instance, many experts suggest withdrawing 4% to 5% of my savings each year in retirement (Fidelity). With that in mind, how I finalize my strategy might depend on Required Minimum Distributions (RMDs).

RMDs and Taxes

- Most retirement accounts require me to take withdrawals starting at age 73 (Finance Senate).

- If I’m managing Roth IRAs, I won’t have RMDs, which can give me more control over my tax bill in retirement.

- It’s a good idea to include financial planning in retirement in my overall strategy so I don’t accidentally hit a large, unexpected tax burden.

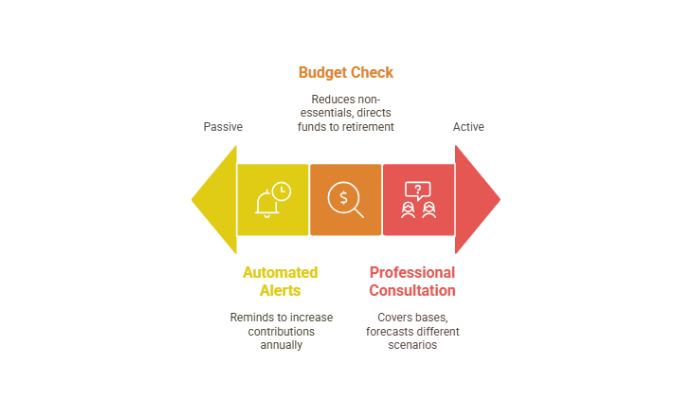

Staying On Track Over Time

My savings goals and investment strategy are not static. They may need adjustment every few years as my ambitions or resources change. If life events like a career shift or a major windfall occur, I want to take a step back and see if I need to boost my saving rate or tweak my retirement timetable.

- Automated account alerts can remind me to increase contributions annually.

- Checking my budget helps me see if I can reduce non-essentials and direct more funds to retirement.

- If I’m lost, I might consult retirement questions to ask to cover my bases or try out the best retirement software for forecasting different scenarios.

Embracing My Financial Future

I’ve discovered that continously revisiting my retirement planning basics can keep me motivated and prepared. In case you’re wondering about pressing concerns, here’s a single-sentence rundown of five common questions on everyone’s mind: when should I start saving for retirement, how much do I need to set aside, what types of accounts work best, will I run out of money too soon, and can I still rescue my plan if I start late?Though I sometimes worry about meeting these milestones, I feel empowered seeing how compounding interest and employer matches can propel me forward. It’s comforting to know there are so many different approaches, from does a pension run out to reading up on the best retirement planning books. No matter when or how I begin, the important part is starting—and continuing—so that my future self can enjoy the life I’ve envisioned. If I ever need a boost, I’ll look at resources like purposeful life after retirement to stay inspired.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...