Explore The Value Of Retirement Income Planners

We all want our golden years to feel comfortable and secure, and that’s where retirement income planners come in. They help chart a practical course toward the future, taking into account rising costs, longevity, and unexpected life events. According to the Department of Labor, only half of Americans know how much money they will need to retire, even though most spend about 20 years in retirement (EP Wealth). That’s a big gap in knowledge and highlights why a knowledgeable planner can be such a game-changer.

Retirement income planners focus on strategies to ensure you won’t outlive your nest egg. They consider factors like inflation, healthcare expenses, and asset allocation. If you want a primer on these concepts, we recommend a quick look at our retirement planning basics, which lays the groundwork for saving and investing smarter.

Address Key Retirement Challenges

How do we keep up with the soaring costs of healthcare and day-to-day essentials? Historically, healthcare costs increase at about twice the rate of inflation (Fidelity). That reality can quickly eat away at your savings if you’re not prepared. On top of that, we’re all living longer. Many people will enjoy 30-plus years of retired life, which can be wonderful but also increases the risk of outliving your resources.

Then there’s inflation. Even moderate inflation erodes purchasing power over time. We often advise clients to plan on meeting 70-90% of their pre-retirement income in order to maintain their lifestyle, in line with expert estimates (EP Wealth). It’s easy to see why carefully structuring your plan to account for multiple market cycles and future cost increases is vital.

Adopt A Strategic Approach

One of our preferred methods to handle risk is the “bucket strategy,” which separates funds into short-term, intermediate-term, and long-term allocations (The Peak Financial Partners). Here’s a quick look:

| Bucket | Time Horizon | Typical Assets |

| Short-Term | 0–4 years | Cash savings accounts, certificates of deposit |

| Intermediate | 5–10 years | Higher-quality bonds, income funds, preferred stocks |

| Long-Term | 10+ years | Growth-oriented equities, emerging market funds |

By dividing your portfolio in this way, we can protect near-term income needs from stock market fluctuations while still dedicating a portion of your estate to longer-term growth.

Naturally, no single strategy suits everyone. Some of us may need a more conservative approach, while others might prefer more aggressive assets. Working with a professional can help tailor the balance between risk and reward to suit your personal comfort level. If you’re ready to dig deeper, explore our financial planning in retirement resource.

Work With Your Chosen Advisor

Many of us find value in partnering with an advisor who understands not just the numbers but also our lifestyle and family goals. A study by ThinkAdvisor found that 52% of Americans working with a financial professional feel more secure than they did a year ago, compared to only 27% who go it alone (EP Wealth). Credentials such as Certified Financial Planner (CFP), Chartered Financial Analyst (CFA), and Chartered Financial Consultant (ChFC) can offer extra peace of mind, as these professionals meet rigorous education requirements and adhere to fiduciary standards (Tiller Financial Professionals Directory).

Before you commit, it’s smart to talk through retirement questions to ask. Those might include: How will they help align your investments with your personal goals? How do they handle market volatility? What’s their approach to tax efficiency? A transparent conversation right from the start helps ensure both you and your advisor share the same vision.

Stay Flexible And Review Often

Even the best-laid plans need revisiting. Life happens, markets shift, and your priorities change. A good retirement income planner will encourage you to update your projections, adjust your investments, and consider new strategies as you move through different stages of retirement. Flexibility lets us correct course if an unexpected event disrupts our financial blueprint.

Still have questions on how retirement income planners compare to best retirement planning books, whether does a pension run out eventually, how a retirement planning checklist might simplify things, why the best retirement software could matter, or what a truly purposeful life after retirement looks like? Keep exploring and sharing your concerns with trusted professionals. By staying informed and proactive, we can build a robust plan that stands the test of time.

Key Takeaways

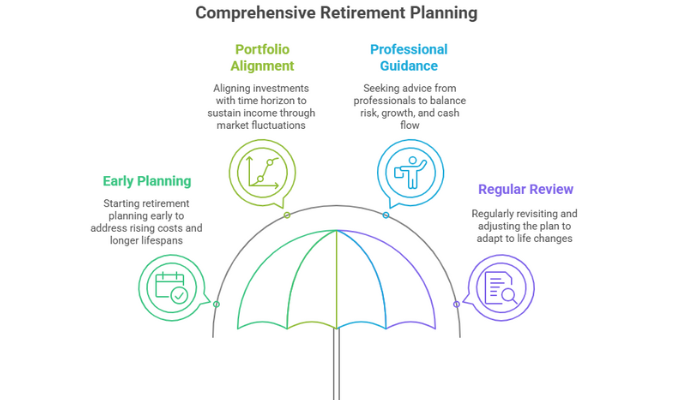

- Rising costs and longer lifespans make it essential to plan for retirement income early and often.

- Aligning your portfolio with your time horizon boosts your odds of sustaining income through market ups and downs.

- Professional guidance can help you balance risk, growth, and cash flow in ways that meet your unique needs.

- Regularly revisiting your plan ensures you’re always fine-tuning your strategy to fit life’s changes.

Our ultimate goal is to enjoy a fulfilling retirement, free from constant financial worry. By enlisting the expertise of retirement income planners, we can feel confident that our money will work as hard as we did all those years.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...