Open the Pension Conversation

We often hear the question: does a pension run out for us, especially if we anticipate living longer than average? Pensions can be reassuring, but we want to understand how they work so we feel confident about our retirement income. According to the Department of Labor (Department of Labor), Defined Benefit pensions typically provide lifetime income. However, the monthly benefit might not track inflation over time, meaning our dollars could lose purchasing power as prices rise.

Just as we ask why is retirement important, it’s also helpful to ask how pensions fit into the broader picture. Let’s look at the key elements that affect whether a pension can run short, the role of inflation and longevity, and how we can supplement our income as needed.

Consider Lifetime Coverage

If we have a Defined Benefit plan, it generally pays out for life, so we’re unlikely to exhaust the principal in the strict sense. Yet, that doesn’t mean we’re totally protected. Cost-of-living adjustments might or might not be included, so we should check the details. Without those adjustments, our pension could feel smaller each year if prices keep climbing.

- Revisit our plan documents and confirm if there’s an inflation provision

- Ask about survivor benefits if we share retirement resources with a spouse

- Explore ways to integrate our pension with financial planning in retirement

Won’t we have enough if our plan is “lifetime guaranteed?” Possibly, but the guarantee only promises payout longevity, not spending power. In other words, the check might still come every month, but it could buy fewer groceries over time if inflation keeps ratcheting upward.

Note Inflation’s Impact

When we consider retirement budgets, inflation can be a big hurdle. Even a steady 2% to 3% rise in living costs can eat into our pension’s real value. That’s why some retirees add personal savings or investments to fill the gap.

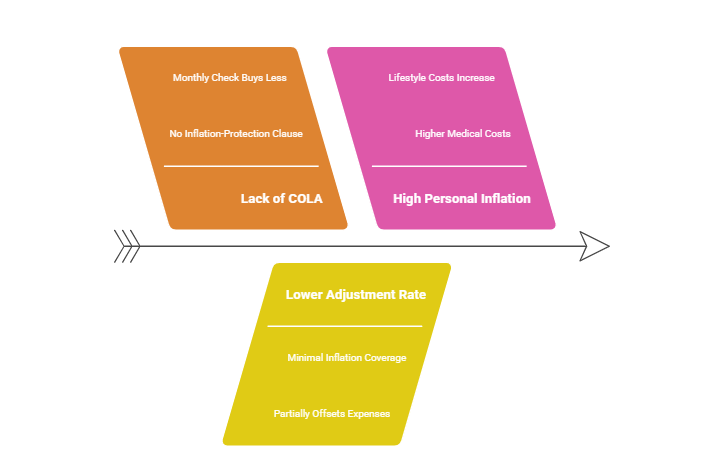

Here’s a quick look at potential pension pain points:

| Potential Issue | Cause | Potential Impact |

| Lack of COLA (cost-of-living adjustment) | No inflation-protection clause in plan | Monthly check buys less as prices climb |

| Lower adjustment rate | Minimal inflation coverage | Partially offsets rising expenses but not fully |

| High personal inflation | Higher medical or lifestyle costs | Pension may not stretch for all unique needs |

Sometimes we worry, “Does a pension run out if inflation surges?” Even if the pension continues, our lifestyle might be squeezed. A practical approach is coordinating different streams of retirement income, such as IRAs, annuities, or investment portfolios. We can also reflect on retirement questions to ask to determine whether our pension and other resources can handle emergency expenses.

Plan for Surprises

Life never goes strictly by the book. Economic downturns, unplanned medical bills, or family responsibilities can create additional strain. Even though a Defined Benefit pension itself might not end, we might feel financially strapped if our spending outpaces the monthly payout.

In one breath, we might ask: do we risk outliving a pension, how does inflation factor in, do job changes affect payouts, can we lose benefits in a recession, or do we need to top up with personal savings? According to the Corporate Finance Institute (Corporate Finance Institute), economic contractions can pressure businesses and individuals alike. While public pensions usually remain intact, private plans could be at risk if the sponsoring company faces severe financial troubles.

If we do have concerns about coverage gaps, we can:

- Boost personal savings alongside our pension

- Keep a cash reserve for emergencies

- Maintain a long-term view on investments

- Stay current with retirement planning basics

Wrap Up and Key FAQs

Balancing peace of mind with practical planning is often the best path forward. While most pensions don’t “run out” in the sense of stopping payments, inflation can quietly reduce their effectiveness over time, and company solvency might introduce additional worries. By diversifying income and planning carefully, we can help ensure we have enough resources to enjoy our post-work years.

Below are five quick FAQs bundled into one simple line. We ask ourselves: How does a pension keep up with inflation, do monthly benefits ever truly stop, can we supplement with personal savings, what if our employer changes funding, and will early retirement reduce monthly amounts?

Our best next step is to align our pension with other resources. Reading up on strategies in best retirement planning books or consulting retirement income planners may help refine our approach. We can also create a personalized retirement planning checklist to stay organized. Let’s remember that thoughtful planning helps us safeguard our future, so our pension can be a reliable cornerstone of a fulfilling retirement.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...