I still remember the day I turned 60 and realized retirement was more than just a distant dream. If you’re anything like me, you’re probably looking for straightforward advice on how to prepare for retirement in your 60s. Let’s be honest, this stage can feel a bit intimidating: shifting market trends, healthcare costs, and the whole question of whether you’ve saved enough. My goal here is to make the path clearer and show that a few intentional steps now can help your dollars work smarter later.

Start With a Realistic Financial Snapshot

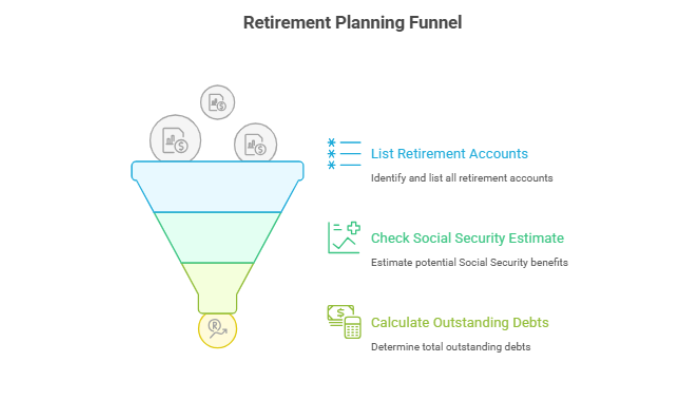

The first step I took was to lay out all my income sources, savings, and potential expenses in one neat table. I jotted down what I have in IRAs, 401(k)s, and other investments, then compared that to my target retirement lifestyle. Experts often say you’ll want around 75–85% of your final working-year salary (Annuity.org), but that may shift depending on personal goals or ambitions.

- Make a quick list of your retirement accounts (401(k), IRA, pension).

- Check your Social Security estimate. The average monthly benefit might be about $1,657, but it varies (Securian Financial).

- Calculate any outstanding debts.

By the way, if you’re toying with the idea of leaving the workforce even earlier, you might want to learn how to save for early retirement so you can pivot now rather than later.

Review and Boost Your Income Sources

I like to think of income sources as puzzle pieces. There’s Social Security, which you can claim as early as 62, though waiting until 70 maximizes the benefit (Thrivent). If you have a pension, that’s another piece, but only about one-third of American retirees still receive such plans (Annuity.org).

Potential Income-Boosting Moves

- Part-time or freelance work: Nearly half of Americans aged 60 to 75 plan to keep working in some capacity (Forbes).

- Annuities or other investments: Stocks, bonds, and mutual funds can offer extra returns if managed wisely.

- Delaying retirement: If you’re itching to leave work but not quite there financially, you could explore whether you can retire by 40 or even hold off until when is the best time to retire.

Sometimes I get five FAQs in one breath about how to prepare for retirement in your 60s: whether to work part-time, how to handle skyrocketing healthcare costs, when to claim Social Security, how much savings is enough, and if I need a backup plan if I run out of money.

Prepare for Health Expenses

Healthcare is often the wild card. You might need more than $300,000 just for medical costs in retirement (Securian Financial). But that’s only an estimate. If you can, consider an HSA (health savings account) while you’re still working and in a high-deductible plan. Once you’re on Medicare, contributions must stop, yet the funds you built up can remain a valuable safety net (Merrill Lynch).

Ideas to Manage Health Costs

- Research Medicare: Being aware of enrollment windows and coverage saves you from penalties later.

- Look into long-term care insurance: There’s a 70% chance of needing some form of long-term care (Merrill Lynch).

- Healthier habits: Daily movement and preventative checkups can help keep bills lower in the long run.

If you’re unsure about your own signs of winding down, reflect on these emotional signs you need to retire. They can be as crucial as financial signals.

Fine-Tune Your Strategy With Tax Efficiency

Perhaps the biggest eye-opener for me was realizing how taxes still loom large after you retire. Required Minimum Distributions (RMDs) kick in at age 73, and missing them can lead to hefty penalties (Vision Retirement). Pulling funds wisely from taxable versus tax-deferred accounts can save a surprising amount, so it’s worth getting some professional guidance.

Quick Tax-Efficiency Moves

- Diversify account types (pre-tax, Roth, taxable).

- Stagger your withdrawals (take from the most tax-friendly account first).

- Time your Social Security or pension payouts based on your current bracket.

If you’re curious about bigger goals, you could check how much to set aside so you can how much to retire early. It’s all about balancing saving and spending.

Stay Flexible and Proactive

Retirement planning isn’t a set-it-and-forget-it process. Inflation might run at 3% or more, trimming your purchasing power every year (Securian Financial). Regular check-ins let you adapt investments, reset milestones, and ensure your strategy fits your lifestyle. Also, if you’re evaluating whether to leave work soon, you might ask yourself, can I retire at 60? Everyone’s timeline is different.

- Explore shifting your retirement date if needed, or scale down hours at work.

- Reassess your monthly costs every six months.

- Look into early retirement planning if you want a head start.

Wrapping Up

All in all, reaching 60 doesn’t mean it’s too late to thrive in retirement. With a firm grasp on your finances, a solid healthcare plan, and some mindful tax strategies, you can head into your retirement years feeling more secure. I’d suggest sitting down once a year to review these points and adjust as you go. Life has a habit of surprising us, but a flexible, proactive plan goes a long way toward a comfortable retirement.

Got a unique strategy that’s helped you? Feel free to share. I believe we all learn best when we compare real-life experiences. And if you’re starting to wonder how long it takes to feel comfortable after leaving your decades-long career, you might find insights at how long does it take to adjust to retirement. It’s all about discovering your sweet spot and enjoying this next chapter with confidence.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...