Many individuals contemplate how they might retire by 40, picturing decades of additional freedom and flexibility. However, early retirement at that age requires substantial financial preparedness, disciplined saving, and careful planning. The following sections outline core strategies for building a stable path toward an earlier exit from full-time employment.

Envision The Retirement Goal

Achieving an early retirement begins with clarifying long-term objectives. Some prefer a life of global travel, while others focus on family or passion projects. According to Farther, it can be helpful to calculate the funds needed by outlining possible living expenses and building a plan around that estimate. This first step grounds retirement planning in a specific vision that becomes the benchmark for all subsequent financial decisions.

Set Financial Milestones

Financial milestones offer markers of progress and help track whether an individual is on course for an early exit from the workforce. Some guidelines recommend having three times one’s annual salary saved by age 40, with more aggressive approaches advocating ten to fifteen times an annual salary to make retiring at 40 feasible (Farther). Individuals who seek detailed strategies for accelerating contributions can consult how to save for early retirement and learn about maximizing employer-sponsored plans or other tax-deferred accounts.

Prioritize Aggressive Saving

Retiring early typically involves saving and investing a considerably higher percentage of income than the traditional 10-15 percent. Many early retirement seekers target saving 20-30 percent, while others strive for 50 percent or more (Kiplinger). Side businesses often boost cash flow, which can be funneled directly into retirement accounts. Consistent, disciplined saving habits take advantage of compound growth, helping the portfolio to expand more rapidly and sustain individuals for decades beyond age 40. Those wondering exactly how much might be required can explore how much to retire early to understand various recommended nest egg targets.

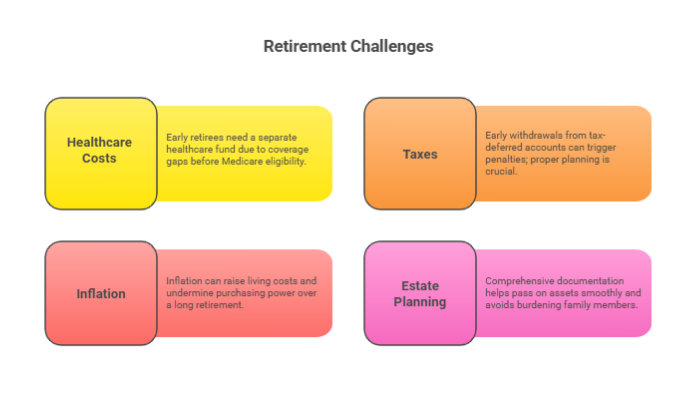

Address Common Challenges

No early retirement plan is complete without preparing for potential obstacles that might erode savings:

- Healthcare Costs: A typical 65-year-old retiree faces an average of $165,000 in medical expenses (Kiplinger). Individuals retiring at 40 may need a separate healthcare fund to fill coverage gaps in the decades before traditional Medicare eligibility.

- Taxes: Withdrawing from tax-deferred accounts too soon can trigger penalties, and tax rates can change over time. Proper planning is crucial, especially if part of the strategy relies on 401(k)s and IRAs.

- Inflation: Over a long retirement span, inflation can raise everyday living costs and undermine purchasing power. Diversified portfolios and conservative withdrawal rates can help mitigate this effect.

- Estate Planning: Comprehensive documentation helps pass on assets smoothly and avoids burdening family members with legal hurdles.

Optimize Investment Strategies

Diversifying investments adds stability to any long-term plan, particularly for individuals leaving the workforce in their 40s. Equities, bonds, real estate holdings, and mutual funds can balance risk and growth potential. According to New York Life, rebalancing a portfolio regularly ensures that it aligns with one’s evolving risk tolerance, especially as retirement draws closer.

Consider Lifestyle Adjustments

Some opt to relocate to areas with a lower cost of living, a move sometimes called geographic arbitrage, to stretch their retirement savings further (Yahoo Finance). Others reduce expenses significantly during working years, funneling the saved funds into investments. Maintaining a sense of purpose can also be important, as one 40-year-old who retired ended up returning to rewarding work after only five months due to boredom (CNBC). For those grappling with the psychological shift, how long does it take to adjust to retirement explores the emotional transition in more detail.

Steps Toward Early Retirement at 40

Planning to step away from work at 40 hinges on building a clear vision, following clear financial milestones, adopting aggressive saving habits, and making well-informed investment choices. It also helps to prepare physically and mentally for the changes that early retirement brings. Some frequently asked questions about how individuals might retire by 40 revolve around recommended nest egg sizes, ideal saving timelines, possible healthcare requirements, ways to manage taxes, and strategies for ensuring funds last.

Ultimately, the journey to early retirement is a deeply personal one, influenced by goals, resources, and risk tolerance. Individuals dedicated to meeting sizable savings targets, navigating potential pitfalls, and creating a balanced lifestyle can boost their chances of successfully exiting full-time employment before the traditional retirement age. For an even deeper exploration of timelines, resources, and emotional readiness, consulting additional guides like early retirement planning can provide more specific steps and insights.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...