We often ask ourselves, “Can I retire at 60 and still maintain the life we’ve built for our families?” It’s an exciting thought, but smart planning is key when we’re looking to trade the 9-to-5 grind for more personal pursuits. In this ultimate guide, we’ll walk through the main steps to help all of us—especially those with high-net-worth portfolios—consider whether stepping away from work at 60 is truly the best move for our future.

Assess Your Financial Readiness

Retiring at 60 might require us to plan more carefully than someone working until 65 or beyond. While general guidelines cite saving around 10x our salary by age 67 (Fidelity), retiring earlier means we could need that same cushion a few years sooner.

Measure Potential Retirement Costs

- Consider both personal and family expenses, including mortgages, potential college tuition for younger dependents, and any aging parent support.

- Factor in travel or hobbies that might increase spending. Some retirees spend more in the early years of retirement on leisure activities.

- Remember inflation. A budget that seems solid now may not hold up if costs rise faster than expected.

By age 60, we want to have a comfortable nest egg that can cover at least 35–40 years of living expenses, since some of us could live well into our 90s. Using a retirement calculator, such as the one from NerdWallet, can help clarify how much we might need, adjusting for inflation and lifestyle changes. If we feel unsure about the numbers, it might be worth consulting early retirement planning resources for a deeper discussion on saving strategies.

Factor In Rising Healthcare Costs

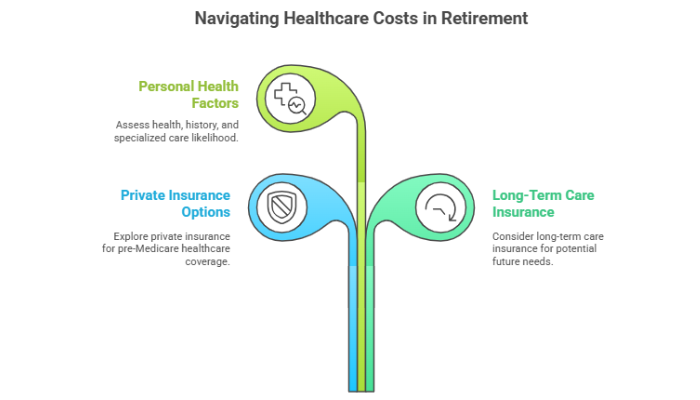

Healthcare is one of the biggest uncertainties for anyone retiring at 60, because we likely won’t qualify for Medicare until 65. According to Merrill Lynch, a 55-year-old couple today could face more than $1 million in healthcare expenses during retirement. Meanwhile, research from Invest for Tomorrow highlights how faster-than-expected inflation can drive these costs even higher.

- Evaluate private insurance options or employer-provided coverage if you plan to stop working before Medicare eligibility.

- Consider long-term care insurance, as nearly 70% of people turning 65 may need some form of long-term care during retirement.

- Factor in current health, family medical history, and the likelihood of needing specialized care later.

If the thought of increasing medical bills concerns us, it might be helpful to see how much to retire early to determine if our savings align with healthcare projections.

Consider Social Security Timing

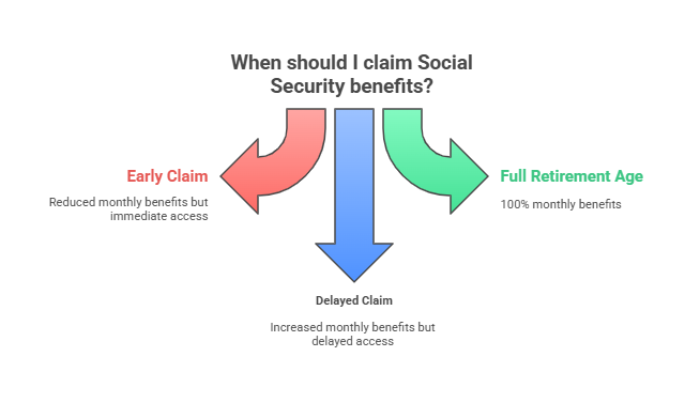

When we retire at 60, Social Security might not be immediately available at full value. We can start benefits as early as 62, but the monthly amount will be reduced for every month before our full retirement age, which typically ranges between 66 and 67 (Social Security Administration).

- Waiting until our full retirement age grants us 100% of our monthly benefits.

- Delaying benefits up to age 70 boosts our payout even further.

- Deciding when to claim is a balancing act: we must consider our health, our spouse’s benefits, and how much other income we have.

Some of us use a strategy of tapping into retirement savings for a few years, holding off on Social Security until full retirement age or later. Understanding government retirement age guidelines can also help us make a more informed choice.

Adjust Lifestyle Expectations

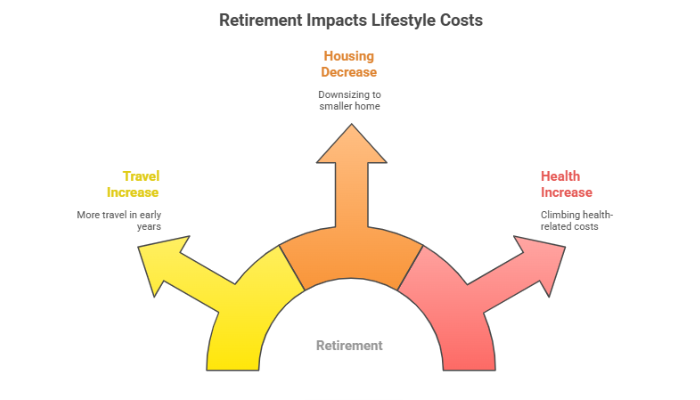

Dropping out of the workforce at 60 often means more time to enjoy our families, hobbies, or to travel. On the flip side, our lifestyle costs could shift substantially:

- We may travel more in the early stages of retirement while we feel energetic.

- Over time, housing expenses might decrease if we downsize to a smaller home.

- Health-related costs could eventually climb as we age.

Researchers at Fidelity report that retirees often spend more on leisure during their initial retirement years and then experience a sharp drop in overall spending as they age. However, these changes vary widely, so we need a plan that fits our personal goals. If emotional readiness is also a question, you might check emotional signs you need to retire to see if it’s time to step away from work.

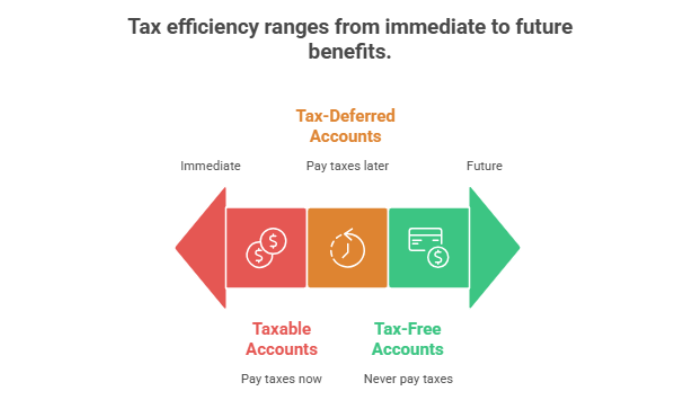

Implement A Tax-Efficient Strategy

Tax planning becomes even more critical when we have larger portfolios or multiple income streams. According to findings from Invest for Tomorrow, creating tax-efficient withdrawal strategies can save us significant money down the road.

- Use a blend of taxable, tax-deferred, and tax-free accounts, such as IRAs or Roth IRAs, to spread out taxes over time.

- Coordinate outlays: tapping accounts in the wrong order could trigger higher tax brackets unnecessarily.

- Reassess investment allocations to ensure we’re not taking on more risk than we can handle.

If we need more detailed suggestions, how to prepare for retirement in your 60s offers practical tips on managing investments, pensions, and social security benefits.

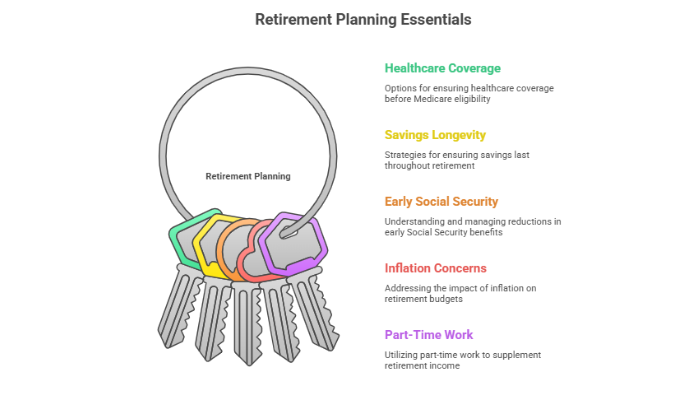

Explore Common Retirement Questions

Five Key Questions

In one breath, people often ask us: “How do we cover healthcare if we retire at 60, do we have enough savings to last, how do we handle early Social Security reductions, will inflation derail our budget, and what if we choose part-time work?”

- Healthcare Coverage: We can either use private insurance, stick with a previous employer’s plan if possible, or explore marketplace options until Medicare kicks in.

- Savings Longevity: Aiming for 10x our salary by our mid- to late 60s is a good start, but retiring at 60 may require more.

- Early Social Security: Expect a permanent reduction if you claim before your full retirement age. Some retirees opt to bridge the gap with personal savings.

- Inflation Concerns: A 3% annual inflation rate assumption is common, but healthcare costs have been known to rise faster.

- Part-Time Work: Consulting or partial employment can supplement our retirement fund and help us stay active.

Conclusion

So, is retiring at 60 a smart move for our future? It can be, provided we’ve assessed our finances, planned for medical costs, and are comfortable with the potential trade-offs around Social Security timing. We also need to be honest about what our day-to-day lifestyle might look like when we no longer head to an office.

Early retirement is a personal choice, and for many high-net-worth families, it involves a complex blend of tax considerations, healthcare planning, and lifestyle goals. If everything lines up, stepping away from work at 60 could give us the freedom to enjoy more of what matters most. If we’re still feeling uncertain, we can explore when is the best time to retire to further clarify our decision.

Either way, having an informed plan means greater peace of mind. Here’s to a bright future—whenever we choose to embrace retirement!

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...