I remember the first time I asked myself, “How long is pension paid after death?” It felt like a curveball, especially when juggling everything else in estate planning. You might also wonder who qualifies for death benefits, whether a lump sum is possible, if taxes apply, and what happens if there’s no living spouse. Let me show you the steps I’d take to figure it all out.

Confirm Plan Status

Before anything else, I always start by reviewing the specific pension plan details. Is it an employer-sponsored plan, a private annuity, or protected by the Pension Benefit Guaranty Corporation (PBGC)? Each setup has different guidelines for distributing benefits after the plan holder dies.

- Check the Summary Plan Description (SPD). It spells out who can receive payments and for how long.

- If the plan is terminated (or taken over by PBGC), you might have to follow PBGC’s processes that often protect spousal rights.

- Look for any mention of “joint-and-survivor” or “pop-up” annuities. These can greatly affect ongoing benefits.

Wondering what to do if the plan doesn’t spell out your situation? A quick call to the plan administrator usually clears it up.

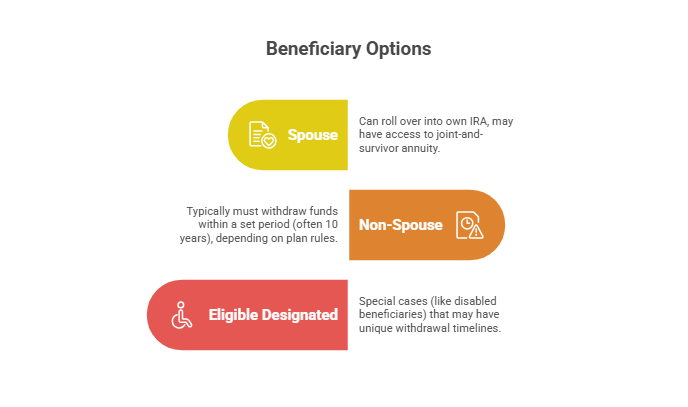

Identify Beneficiary Type

Determining whether you’re a spouse, non-spouse, or “eligible designated beneficiary” (as the IRS calls it) influences how long payments continue. According to the IRS (IRS.gov), spousal beneficiaries often enjoy extra flexibility, like the option to roll the inherited pension into their own retirement account.

Here’s a quick look:

| Beneficiary | Options & Rules |

| Spouse | Can roll over into own IRA, may have access to joint-and-survivor annuity. |

| Non-Spouse | Typically must withdraw funds within a set period (often 10 years), depending on plan rules. |

| Eligible Designated | Special cases (like disabled beneficiaries) that may have unique withdrawal timelines. |

If you’re unsure which category applies, confirm it by contacting the plan administrator. You’ll also need a certified death certificate at hand for official verification.

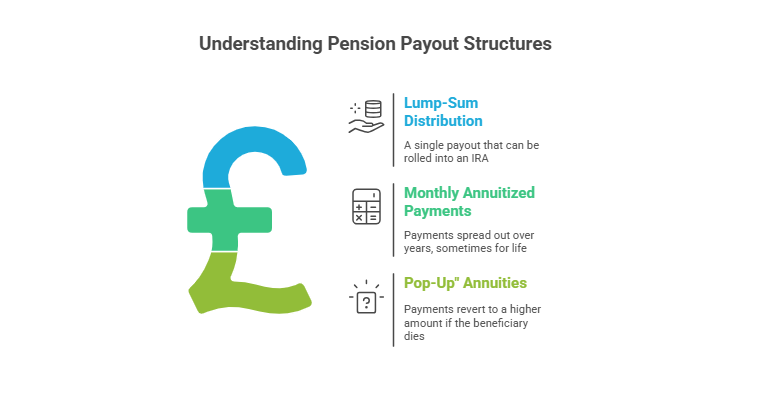

Check Payment Options

Next, I see what the plan allows for payout structures. Some pensions end right when the participant dies, while others keep paying a survivor’s pension or offer one-time death grants (Your Europe – European Commission).

- Lump-Sum Distribution: Some beneficiaries prefer a single payout, which they can roll into an IRA.

- Monthly Annuitized Payments: This spreads payments out over years, and sometimes for life.

- “Pop-Up” Annuities: If the beneficiary dies before the pension recipient, the monthly payment may revert to the higher “straight life” amount.

Does your plan specify how many years a spouse or dependent can keep receiving payments? Those details determine if your pension extends for decades or ends fairly soon.

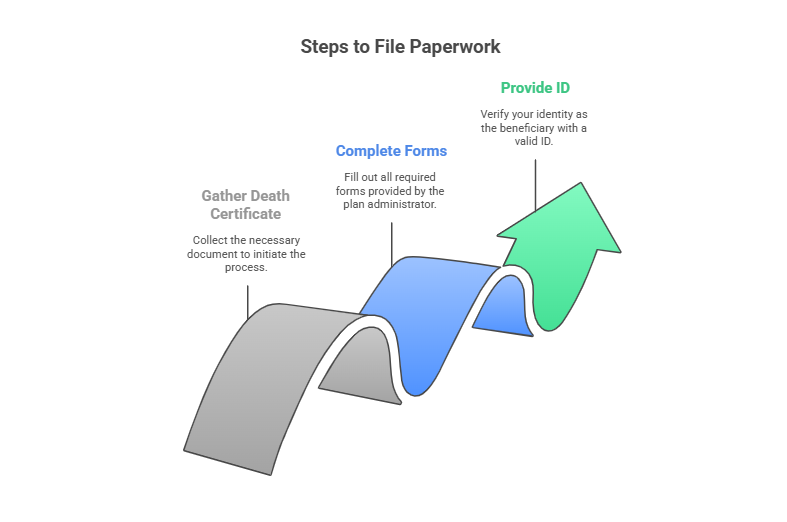

File The Required Paperwork

Filing can feel like a chore, but without it, you won’t receive what’s due. You should:

- Gather the death certificate. It’s usually the first item required.

- Complete any forms the plan administrator sends. They might go by different names, but they all finalize your claim.

- Provide a valid form of ID to confirm you’re the correct beneficiary.

I learned how easy it is to miss a crucial form in the chaos surrounding a loved one’s passing. Having a checklist is vital. If you need more tips on broader strategic options, check out my notes on retirement planning for specific professions.

Manage Taxes And Final Steps

Finally, address potential tax bills. Pension proceeds can be taxable at ordinary income rates, though spousal rollovers or IRAs offer ways to postpone or reduce taxes (Protective). It’s wise to speak with a tax professional or a certified retirement planner to decide how best to preserve your inherited benefits.

- Review RMD (Required Minimum Distribution) rules. Even inherited Roth IRAs might have RMD obligations.

- File state and federal tax forms properly if the payout is considered taxable income.

- Update your own will or estate plan. Life events like inheriting a pension can reshape your financial outlook.

Feeling uncertain about taxes? I get it. Having a quick chat with a trusted retirement advisor can be a big weight off your shoulders.

By following these steps, I’ve seen how straightforward it can be to answer the question “How long is pension paid after death?” It all hinges on plan specifics, spousal rights, and timely paperwork. If you’d like more hands-on guidance, consider connecting with a professional or exploring topics like best retirement plan for self employed. Above all, remember that knowledge is your ally in securing the future you deserve.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...