If you’ve been thinking about the retirement questions to ask so you can safeguard your future, you’re not alone. Planning for life beyond your career involves more than just putting money aside; you’ll want to consider tax strategies, estate plans, healthcare costs, and lifestyle goals. Below is a curated list of smart questions high-net-worth individuals often raise when eyeing a comfortable, secure retirement.

Evaluate Your Retirement Timeline

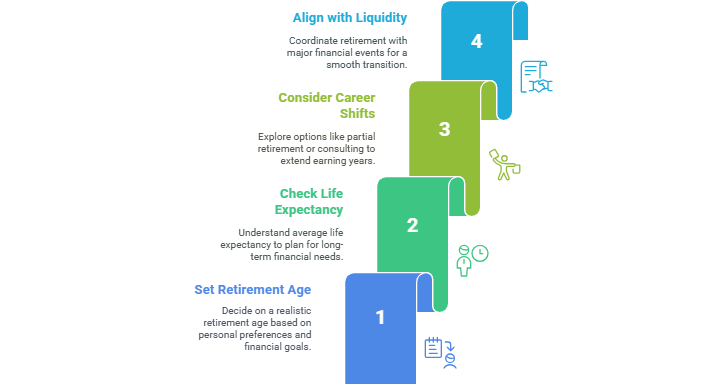

Your first step is deciding when you realistically want to retire. Some individuals aim for 65 (the median age many plan to retire, according to Citizens Bank), but you might prefer leaving the workforce earlier or extending your career. Either way, a solid timeline shapes your yearly savings goals.

- Check life expectancy. According to the Social Security Administration, men turning 65 in 2025 often live to about 84.3, with women reaching about 86.9.

- Think about potential career shifts. Could partial retirement or consulting extend your earning years?

- Align your exit date with major liquidity events or the sale of a business.

Target the Right Savings Rate

Most experts (including Fidelity and T. Rowe Price) recommend saving 15 percent of your annual income for retirement. For high earners, that figure may need to be even higher.

- Verify if you’ll need seven to 13 times your preretirement annual income by age 65.

- Use calculators from sources such as FINRA or Citizens Bank to fine-tune your personal target.

- Discuss your strategy with retirement income planners if you anticipate outpacing the typical benchmarks.

Assess Your Investment Vehicles

A 401(k) plan, an individual IRA, or even a combination of the two can supply critical retirement momentum. Each option offers distinct tax advantages and contribution limits, as Equifax points out.

- 401(k) perks: Employer match and high annual limits.

- IRAs (Traditional or Roth): Flexibility in investment choices but lower contribution thresholds.

- If self-employed, explore SEP or SIMPLE IRAs for higher ceilings on tax-advantaged contributions.

Check Potential Healthcare Costs

Healthcare expenses can balloon in retirement, especially in your later years. According to Citizens Bank, retired couples may need between $188,000 to $366,000 just to largely cover medical bills over time.

- Evaluate Medicare enrollment. Remember to sign up around age 65 to avoid penalties.

- Factor in premiums for supplemental policies if you want broader coverage options.

- Consider financial planning in retirement with a professional to predict and manage healthcare spending.

Plan for Tax Efficiency

High-net-worth individuals often juggle complex tax considerations, so structuring your portfolio wisely can save you substantial sums. That might mean balancing Roth contributions with tax-deferred accounts.

- Look at your future bracket. The type of account you choose can hinge on your presumed tax bracket at retirement.

- Explore strategies for business owners. Early corporate exits or concentrated stock holdings require dealing with potential capital gains.

- Combine these steps with a retirement planning checklist so you don’t miss crucial deadlines.

Think About Social Security Timing

The age you start taking Social Security deeply impacts your monthly benefits. If you wait until full retirement age (or later), your monthly check gets bigger (around 8 percent more per year until 70).

- Use a my Social Security account to see how different start ages affect your benefits.

- Remember that your family members may also qualify.

- Weigh whether postponing benefits is worth the trade-off for your goals, especially if you’re comfortable delaying income.

Look for Hidden Fees

Investment management fees can eat into your nest egg over the long run. FINRA urges you to keep an eye on mutual fund expense ratios, trading costs, or advisor charges.

- Run your portfolio data through FINRA’s Fund Analyzer to see how fees stack up.

- Factor in 401(k) administrative fees; they vary widely between providers.

- If costs are becoming unmanageable, reevaluate your plan or discuss adjustments with a fiduciary.

Stay Flexible and Adaptive

You might face new life events, changes in health, or shifts in financial markets. It’s wise to revise your plan every few years. Keep your approach dynamic, so you can adapt if you receive an inheritance, sell a company, or decide to create a purposeful life after retirement.

- Monitor your portfolio allocations regularly.

- Consider pivoting to more conservative investments as you near retirement age.

- Continue building know-how by checking out best retirement planning books.

Quick Takeaways

- Decide your retirement age and align it with life expectancy plus career opportunities.

- Set a robust savings rate, potentially over 15 percent of your yearly income if you’re a high earner.

- Choose the correct savings vehicles (401(k), IRA, etc.) for tax advantages and employer matches.

- Anticipate healthcare expenses, which can rapidly escalate in later years.

- Time your Social Security carefully for maximum lifetime benefits.

- Keep an eye on fees to avoid diminishing your returns.

- Build flexibility into your strategy to handle surprises or shifting goals.

For one-sentence clarity on five FAQ about retirement questions to ask, consider: “Are you wondering how much to save, when to retire, which accounts to open, what happens if you retire early, and how to handle rising healthcare costs?”

If you’d like more background on fundamentals, explore retirement planning basics to ensure you’re well-informed from the start. Also, see why is retirement important if you need a deeper view of how retirement can shape your legacy. By posing the right questions now, you’ll be poised for a future that’s both financially secure and personally fulfilling.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...