At first glance, a flat fee CFP (Certified Financial Planner) may seem like a straightforward approach to managing your wealth. You know what you will pay, and there are no surprises tied to portfolio performance or complex commissions. For high-net-worth families, this method offers transparency and can help avoid conflicts of interest often associated with other financial advisor models. If you have ever asked about the cost of a financial advisor, understanding how flat fees work may clarify when and why this option makes sense.

We have seen that this pricing structure resonates with individuals who want predictability and personalized guidance. Because the advisor’s compensation does not rely on your investment size, you can focus on long-term wealth strategies instead of worrying that your growing assets might drive up fees.

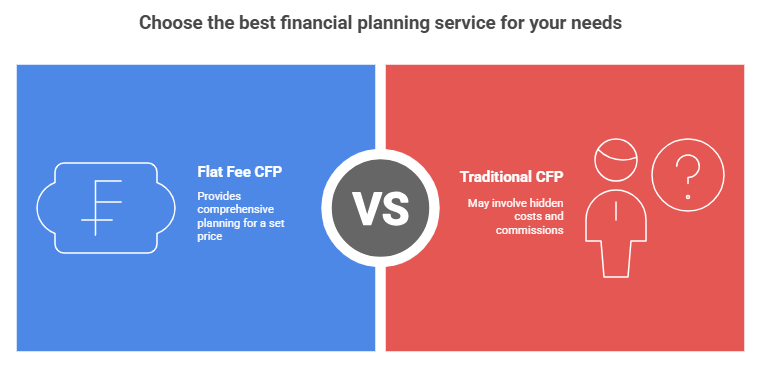

Understand Flat Fee CFP Services

A flat fee CFP provides comprehensive financial planning for a set dollar amount. According to Farther, the scope often includes retirement forecasting, tax optimization, and estate planning. This approach suits business owners, tech executives, and families overseeing multi-generational portfolios who want holistic guidance without monthly or annual cost fluctuations.

- Fixed Pricing: You pay one clear rate, whether you are organizing a complex estate plan or restructuring your investment approach.

- Service Transparency: There is no hidden expense or commission, so you know exactly when, why, and how much you are paying.

In addition to predictability, flat fee advisors may also serve as fiduciaries, meaning they must put your best interests first. When compensation does not hinge on asset volumes or product sales, we find that clients gain more peace of mind about the integrity of the advice.

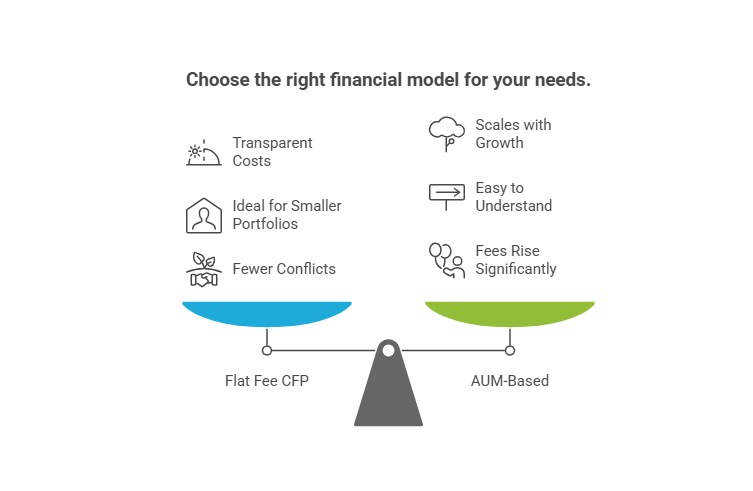

Compare Flat Fee vs AUM

How does a flat fee CFP stack up against an assets under management (AUM) model? While both can serve your family’s needs, each has advantages and drawbacks.

| Model | Fee Calculation | Pros | Cons |

| Flat Fee CFP | Fixed dollar amount per engagement | Transparent costs, fewer conflicts | Not always ideal for smaller portfolios |

| AUM-Based | Certain percentage of portfolio | Scales with growth, easy to understand | Fees can rise significantly for large asset holders |

Some prefer an AUM arrangement because costs align with portfolio performance. Still, for households with large liquidity events or evolving trust structures, those ongoing percentage-based fees may outperform a straightforward flat arrangement. If you are uncertain, we cover more about how financial advisors earn money in another resource.

Minimize Conflicts Of Interest

A major motivation for choosing a flat fee planner is to avoid bias rooted in commission structures or asset-based incentives. When an advisor’s pay depends on trades or pushing products, high-net-worth families can feel pressured to invest in ways that do not align with their values.

Conversely, many fee-only CFPs have pledged to follow fiduciary standards as required by organizations such as NAPFA. This higher level of ethical commitment centers on your well-being, from constructing tax-efficient trusts to outlining multi-generational giving strategies. By paying a fixed price, you remove the concern that investment decisions might be influenced by the advisor’s payout.

Assess Key Credentials

Looking beyond fees, it is important to assess an advisor’s expertise. Many families require sophisticated planning for charitable giving, business succession, or estate settlements. Credentials like the CFP mark or CFA charter can be indicators of advanced training. You can also look up an advisor’s background using resources such as the SEC’s Investment Adviser Public Disclosure database.

We have covered the details about cost in our guide on the cost of a financial advisor. While cost remains critical, you also want to confirm whether the advisor’s background, experience, and resources match your long-term objectives.

Wrap Up And Next Steps

If you are new to the idea of a flat fee CFP, you might be asking: “What does a flat fee CFP typically charge, how does it differ from AUM-based advisors, do they handle large portfolios, are there hidden fees, and can they also manage estate planning?” For high-net-worth families, a flat fee arrangement can reduce conflicts of interest, keep costs transparent, and let you plan according to your unique goals.

By knowing your advisor’s fees upfront, you get to budget effectively and maintain clarity about the recommendations they provide. The result can be a partnership focused on wealth preservation, tax strategies, and family legacy. We encourage you to evaluate an advisor’s credentials, track record, and fit with your family’s vision. Open conversations about fees and services will help ensure an enduring, productive relationship with your planner.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...