So you’re exploring S corp retirement plan options, and you want to make sure you’re on the right track. Good call. Owning an S corporation can open some great doors for retirement savings, but it does come with a few twists. For example, distributions from your S corp don’t count as earned income for retirement plan purposes (IRS). That means your contributions have to be based solely on the W-2 wages you pay yourself. Ready to find a plan that fits both your business structure and future goals? Let’s do it.

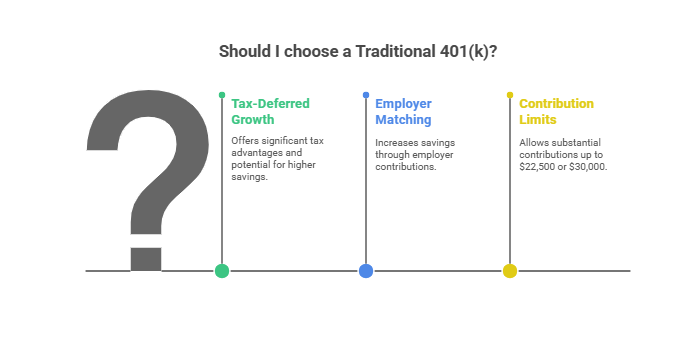

Consider a Traditional 401(k)

A Traditional 401(k) offers generous tax-deferred growth. You can contribute up to $22,500 in 2023 (or $30,000 if you’re 50 or older), according to the IRS. Employer matching is also in play, which can help you tuck away even more funds. Just remember that any contributions must be from your salary, not your shareholder distributions. If you want more guidance on choosing the right plan for you, check out our retirement advisor resource.

- Contributions: Tax-deferred

- Key Benefit: Immediate tax deduction on contributions

- Watch Out: Don’t try to use S corp distributions for this plan

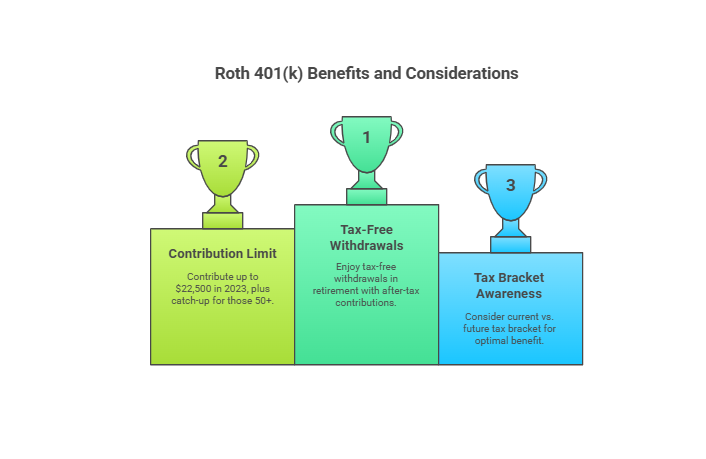

Think About a Roth 401(k)

If you prefer paying taxes now to enjoy tax-free withdrawals later, the Roth 401(k) is worth a look. You invest with after-tax dollars, so withdrawals during retirement normally come out tax-free. This setup can be a lifesaver if you anticipate landing in a higher tax bracket down the road. Just like with the Traditional 401(k), the contribution limit for 2023 is $22,500 (plus a catch-up for those 50 and over).

- Contributions: After-tax

- Key Benefit: Tax-free withdrawals in retirement

- Watch Out: Be mindful of your current vs. future tax bracket

Use a SEP-IRA

A Simplified Employee Pension (SEP) IRA can be easier to manage than a 401(k), especially if your S corp is on the smaller side. You can generally contribute up to 25% of your W-2 wages, which is often more than you’d set aside in a standard IRA. However, distributions from the S corp still don’t count toward those contributions. A SEP-IRA can be an attractive choice if you like simplicity and higher potential annual contributions.

- Contributions: Employer only (up to 25% of salary)

- Key Benefit: High contribution limits relative to your income

- Watch Out: No employee salary deferrals here

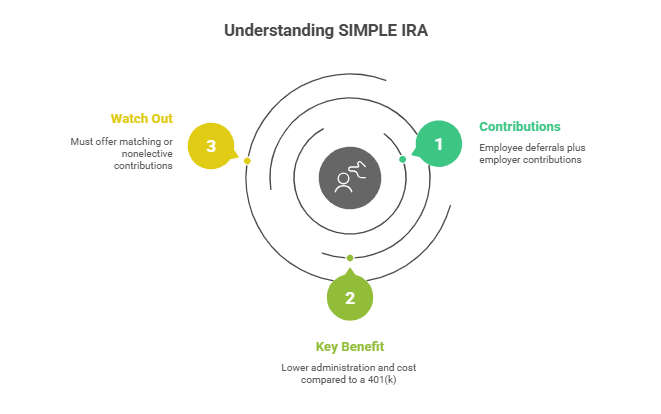

Start a SIMPLE IRA

A Savings Incentive Match Plan for Employees (SIMPLE) IRA lives up to its name by being, well, simple. This plan allows you and your employees to contribute, taking some administrative workload off your plate. You can match employee contributions or make a non-elective contribution for everyone. Limits for 2024 are rising, which could give you a bit more wiggle room in your savings strategy. This plan might work well if you have a few employees you want to take care of too.

- Contributions: Employee deferrals plus mandatory employer contribution

- Key Benefit: Lower administration and cost compared to a 401(k)

- Watch Out: Must offer matching or nonelective contributions

Explore a Solo 401(k)

If you don’t have any full-time employees (besides a spouse), the Solo 401(k) can help you save big. The employee deferral limit is the same as a Traditional or Roth 401(k). On top of that, as the employer, you can make profit-sharing contributions, potentially hitting higher totals. This setup is especially appealing to S corp owners who like maximum flexibility and want to stash away a nice chunk of change each year. To learn more about how self-employed professionals can tailor their retirement approach, see our best retirement plan for self employed.

- Contributions: Employee deferrals and employer profit-sharing

- Key Benefit: High savings potential for solo business owners

- Watch Out: Once you hire employees, you’ll need to adjust

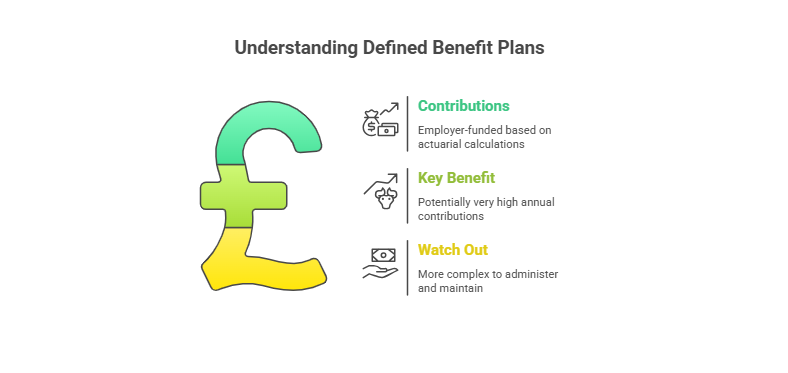

Tap a Defined Benefit Plan

If you’re aiming for large contributions and predictable payouts later, a defined benefit plan might be the right fit. These plans calculate your eventual retirement benefit based on factors like salary and years of service. They can be especially beneficial for high earners with stable cash flow, although they do come with more complexity and higher setup costs. Still, they pack a punch if you crave significant tax-advantaged saving.

- Contributions: Employer-funded, based on actuarial calculations

- Key Benefit: Potentially very high annual contributions

- Watch Out: More complex to administer and maintain

You might wonder: which plan offers the highest contribution limit, do distributions affect eligibility, how do employees benefit, can you mix plan types, and which plan is better for after-tax savings? Answering these questions often starts with understanding your cash flow, tax bracket, and long-term withdrawal goals. It also helps to check out our retirement planning for specific professions for deeper insights if you’re looking for specialized guidance.

When you’re ready to take the next step, consider chatting with a financial pro who understands S corps and can align your strategy with your lifestyle. After all, you’ve earned the right to retire on your own terms.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...