Picture yourself looking ahead to a comfortable, worry-free retirement. If you want to set aside funds gradually rather than in one large lump sum, a flexible premium deferred annuity could fit perfectly into your overall plan. It lets you contribute smaller amounts over time, which can help reduce the stress of committing a big chunk of money all at once.

Understand A Flexible Premium Deferred Annuity

A flexible premium deferred annuity is, at its core, a long-term retirement tool that grows during an accumulation phase. You make incremental payments on a schedule that suits your finances. Later on, when you’re ready to receive payouts, it transitions into the payout phase and offers a steady income. According to Western & Southern, this approach is ideal if you have several years before retirement and want to spread your financial commitment over time (Western & Southern).

Because contributions are spread out, you have flexibility. You can make smaller payments whenever your budget allows, rather than tying up a big sum. Taxes on your annuity growth are deferred until you withdraw money, so it can help you keep more funds compounding for the future.

Know How It Works

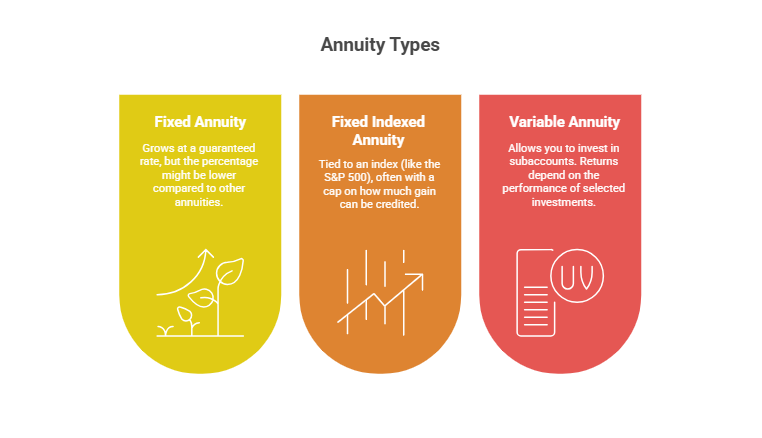

During the accumulation phase, your payments steadily build value within the annuity. Different types of flexible premium deferred annuities dictate how your money might grow:

| Type | Key Features |

| Fixed Annuity | Grows at a guaranteed rate, but the percentage might be lower compared to other annuities. |

| Fixed Indexed Annuity | Tied to an index (like the S&P 500), often with a cap on how much gain can be credited. |

| Variable Annuity | Allows you to invest in subaccounts. Returns depend on the performance of selected investments. |

Each type offers unique risk and reward trade-offs. For instance, a fixed indexed annuity has upside potential linked to the market, but any gains are capped. Meanwhile, a variable annuity may deliver higher returns if markets soar, but you’ll feel the hit if they dip (Thrivent).

Explore The Benefits

The main draw of a flexible premium deferred annuity is convenience. You can contribute at your own pace, which eases the load on your monthly budget. Because this annuity typically has a tax-deferred growth component, every dollar you add can keep working behind the scenes.

You also have some freedom to align payments with your broader retirement asset allocation strategy. For instance, if you come into a bit of extra cash one quarter, you can up your contribution. Over many years, consistent deposits really add up.

Consider Potential Drawbacks

One big consideration is your discipline in making ongoing contributions. If you stop making payments or make them too infrequently, your annuity’s growth may be limited. Another factor is liquidity. Taking money out too early usually triggers surrender fees and a 10 percent early withdrawal penalty if you’re under 59 1/2 (Western & Southern).

On top of that, no single annuity product is one-size-fits-all. If you like to handle a lump sum at once, you might lean toward a single premium deferred annuity. And if you want more immediate income, you might explore immediate annuities or consider whether you can layer a flexible premium deferred annuity with other retirement investment options.

Decide If It’s Right For You

Deciding on this type of annuity hinges on your timeline, cash-flow needs, and overall financial goals. Flexible premium deferred annuities tend to appeal to folks reaching their late 50s or early 60s, who want to spread contributions over the remaining years until retirement. If you have concerns about specific market risks or inflation, you’ll want to compare fixed, indexed, and variable options to pinpoint the best fit.

Review Common FAQs

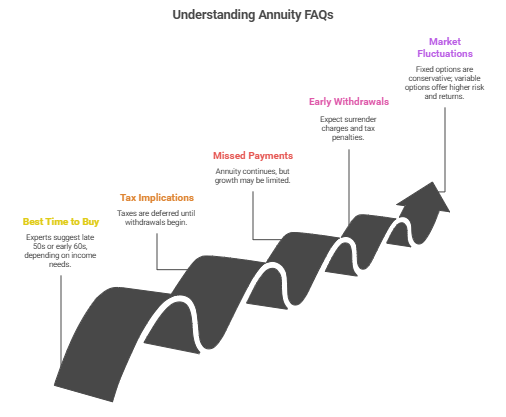

You might be asking, “When is the best time to purchase a flexible premium deferred annuity, how do taxes work, what if you can’t make payments, is it possible to withdraw early, and does it protect you from market fluctuations?” Here are quick answers:

- Best Time to Buy: Many experts suggest making the purchase in your late 50s or early 60s, but it depends on how soon you need an income stream.

- Tax Implications: Taxes are deferred until withdrawals begin, so you typically pay when you start receiving income.

- Missed Payments: Your annuity can still exist, but its overall growth may be limited. Think of regular payments as the fuel for long-term growth.

- Early Withdrawals: Expect surrender charges plus extra tax penalties if you withdraw before 59 1/2.

- Market Fluctuations: Fixed and fixed indexed options are more conservative. Variable annuities carry higher market risk, but they also offer higher potential returns.

Try to weigh these pros and cons alongside other options, like pension vs annuity, so you can see how each approach affects your future income.

Remember, a flexible premium deferred annuity can be a strong addition to your retirement toolkit if you want to invest gradually and let your contributions compound over time. Once you reach retirement, you’ll be glad you took steps now to secure a steady income stream later.

Feel free to chat with a trusted financial advisor about the details. This move could give you more confidence as you continue building a path toward the retirement lifestyle you deserve.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...