Investors nearing retirement often compare pension vs annuity options to ensure they have a reliable source of income. Deciding between these two can shape long-term financial stability, especially for individuals with substantial assets or complex portfolios. Each approach offers unique benefits and trade-offs, so understanding their fundamental differences can guide an informed choice.

Understand Pension Vs Annuity

Defining A Pension

A pension is an employer-sponsored plan providing retirement income based on age, years of service, and salary history. Many government jobs still include pensions, but private-sector offerings have become less common over the years (Annuity.org). Once a worker qualifies, the plan typically guarantees set monthly checks. Alternatively, some plans allow a lump sum payout that can be rolled into another account.

Defining An Annuity

An annuity is an insurance contract purchased from an insurer. Individuals either invest a lump sum or make periodic payments, and the insurer then disburses a stream of income. These payouts can be fixed or variable, immediate or deferred, depending on the contract’s structure. Annuities appeal to those who want greater flexibility and control in tailoring their retirement income (SmartAsset).

Consider Key Differences

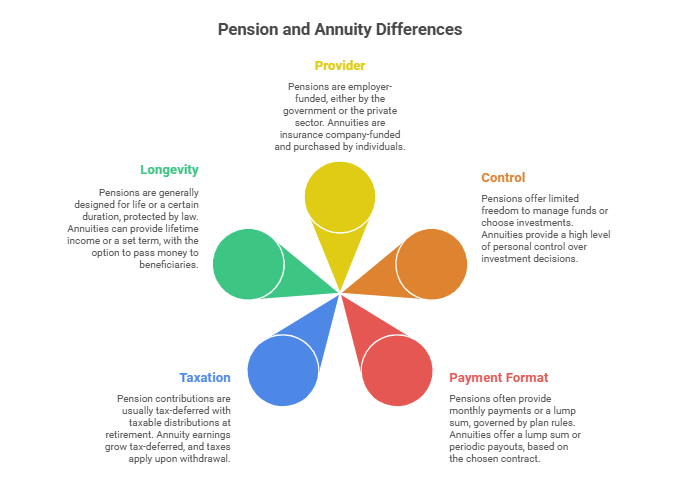

Below is a quick comparison to highlight how pensions and annuities stand apart:

| Factor | Pension | Annuity |

| Provider | Employer-funded (government or private sector) | Insurance company-funded, purchased by individuals |

| Control | Limited freedom to manage funds or choose investments | High level of personal control over investment decisions |

| Payment Format | Often monthly payments or lump sum, governed by plan rules | Lump sum or periodic payouts, based on the chosen contract |

| Taxation | Usually tax-deferred contributions with taxable distributions at retirement | Earnings grow tax-deferred, and taxes apply upon withdrawal |

| Longevity | Generally designed for life or a certain duration, protected by law in many cases (SmartAsset) | Can provide lifetime income or a set term, with the option to pass money to beneficiaries |

Funding And Control

Pensions often require minimal effort once established, as employers handle contributions. Annuities, on the other hand, rely on individual contributions and risk tolerance. Some investors combine pensions with a flexible premium deferred annuity to balance guaranteed income with potential tax advantages.

Payout Structures

A pension typically offers a monthly check for life. Annuities allow multiple choices, including immediate income or deferring payments until a chosen date in retirement. Both can also be taken as lump sums that can be invested in retirement asset allocation strategies for potentially more growth.

Tax Considerations

Contributions to pensions often come from pre-tax income, reducing taxable earnings during working years. However, retirees must pay income tax on pension withdrawals at retirement, unless after-tax contributions were made (SmartAsset). Annuities also feature tax-deferred growth, but distributions are taxed when drawn. Under current tax rules, required minimum distributions generally begin at age 73 for qualified plans, though certain omissions apply if an individual continues working beyond that age.

Deciding The Better Fit

Pensions can suit those who prefer a more hands-off approach supported by legal guarantees. Individuals confident in their employer’s long-term stability may appreciate a straightforward monthly check. Annuities may be more suitable for those who want portable retirement investment options, extra layers of customization, or the capacity to choose an insurer. Some retirees with significant resources also explore whether they can maintain multiple plans, for instance by asking questions related to can you have a pension and 401k.

Selecting between a pension vs annuity often comes down to personal financial goals and risk tolerance. For those who hold large or complex assets, the potential for strategic tax planning with an annuity can be very appealing. On the other hand, a pension’s relatively predictable income reduces the worry of outliving savings. Some individuals also consider partial lump sums to preserve immediate access to capital and invest the remainder into an annuity or other vehicles like retirement investment options.

Frequently Asked Questions

Many individuals wonder, “Can pension and annuity benefits be combined, which taxation method applies best, does a lump sum or monthly payment offer more security, what fees might occur, and how flexible are retirement options in volatile markets?”

In practice, retirees can blend both a pension and an annuity to protect against longevity risk while still pursuing strategic growth. Each arrangement should ideally be reviewed with a financial advisor, particularly for those managing significant wealth or facing complicated liquidity events. The right mix can support long-term security, estate planning, and lifestyle aspirations.

Investors who seek more detailed guidance might review what to do when u retire or explore additional resources that address specialized concerns, whether that’s how to manage concentrated stock positions or how to minimize taxes during retirement. Professional consultation helps tailor these decisions to an individual’s unique circumstances.

Ultimately, pensions reward long service and loyalty with structured benefits, while annuities let individuals craft a personalized income stream that fits their future plans. Having a clear grasp on each option’s pros and cons encourages confident decisions about how to secure a stable, fulfilling retirement.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...