Understand Retirement Insurance

Individuals who wonder how to buy retirement insurance tailored to their specific needs can start by looking at the variety of options available, from permanent life insurance to employer-sponsored plans. Retirement insurance generally aims to offer financial stability later in life or provide a death benefit to beneficiaries, ensuring that critical expenses are covered. High-net-worth families often place particular emphasis on selecting solutions that protect significant assets and align with long-term philanthropic and legacy goals.

Why Retirement Insurance Matters

Retirement insurance can safeguard a person’s loved ones from large expenses, such as medical bills or unforeseen costs that arise in later years. According to the Social Security Administration, individuals can begin exploring options for monthly benefits starting at age 62, with full retirement age ranging between 66 and 67. For those seeking more comprehensive protection, a combination of coverage—including private insurance and employer plans—can be beneficial. This layered approach can reduce the risk of outliving one’s savings, which is a growing concern given increased life expectancy.

Popular Insurance Types

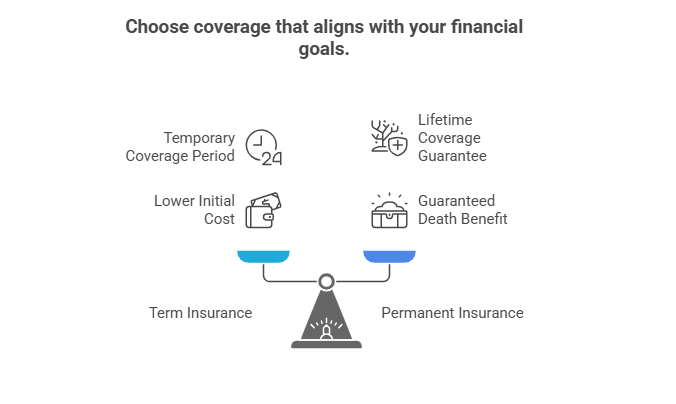

- Term Life Insurance: Provides a death benefit for a defined period, such as 10, 20, or 30 years. Premiums usually start lower than permanent insurance but can rise upon renewal.

- Permanent Life Insurance: Offers lifelong coverage with fixed premiums, cash value accumulation, and potential dividends. According to New York Life, permanent policies can be used to supplement retirement income and meet other financial needs over time.

- Group Plans: Some employers include life insurance as part of their retirement benefit packages. However, the coverage might be limited, so many individuals opt for additional private policies.

Compare Coverage Options

Evaluating coverage options involves understanding personal goals, family structure, and anticipated retirement costs. High-net-worth individuals, for example, may look beyond basic benefits and focus on plans that minimize taxes and protect large estates.

Term Vs. Permanent

Term insurance suits those who want coverage for a set period, perhaps until mortgages or tuition obligations end. Permanent insurance typically appeals to those seeking coverage for a lifetime with a guaranteed death benefit, regardless of changing health conditions. Anyone deciding between these options might also compare them to annuities, discussed in pension vs annuity, to build a balanced strategy that accounts for income needs in retirement.

Combining Insurance With Other Plans

In many cases, retirement insurance works alongside employer-sponsored solutions such as 401(k)s or pensions. Those curious about blending a pension with additional coverage may consult can you have a pension and 401k to explore the best ways to align these options. Some individuals also include specialized products, such as a flexible premium deferred annuity, for added retirement security.

Follow Key Buying Steps

Locking in a suitable policy often depends on assessing coverage amounts, premium affordability, and the insurer’s reputation. For those asking which plan is best, what coverage is optimal, how much it costs, how to sign up, and when to buy retirement insurance, the answers revolve around three main steps: defining coverage goals, comparing premium structures, and checking provider stability.

Define Coverage Goals

A straightforward calculation is multiplying annual income by 10 or 15 to estimate ideal coverage. Others use the DIME formula (debt, income, mortgage, and education) to ensure clarity about total liabilities. According to NerdWallet, subtracting any liquid assets from these sums can help pinpoint a more precise insurance figure.

Compare Premium Costs

Premiums will vary depending on age, health status, and policy duration. Permanent coverage tends to cost more upfront but can prove valuable over time because it accumulates cash value. Term policies are usually cheaper initially, which can be appealing for younger earners aiming to manage multiple financial commitments alongside retirement investment options.

Check Provider Stability

An individual with substantial assets should verify an insurer’s financial health through third-party rating agencies. Solid reviews and high ratings indicate that the provider is more likely to meet policy obligations in the long run. Additionally, checking an insurer’s claim-handling record helps ensure beneficiaries receive timely payouts if a claim is made.

Review Coverage Over Time

Life circumstances change. A policy that was once suitable might need adjustments if someone inherits a large sum, sells a business, or faces increased medical expenses. Periodic reevaluation can help maintain adequate coverage while aligning with overall wealth management plans.

Adjust for Evolving Needs

Individuals may expand or reduce coverage based on changes in family structure, like adding new heirs or no longer needing to ensure children’s education costs. In many cases, older policies can be converted, upgraded, or even replaced to accommodate new financial goals.

Seek Professional Guidance

Consulting an independent financial advisor can help high-net-worth families integrate their insurance strategies with broader retirement plans. Some may opt to diversify with wealth-building vehicles or examine retirement asset allocation strategies. Experienced advisors often bring clarity to complex situations, whether one intends to retire at 60 with retire at 60 with 2 million or preserve a large estate for future generations.

Conclusion And Next Steps

Buying retirement insurance that fits each person’s unique financial goals requires careful consideration of coverage amounts, plan duration, and provider reliability. Reviewing all options, including employer-sponsored benefits and potential supplemental coverage, can provide the confidence needed to secure a strong retirement plan. For further reading, individuals can explore the best state retirement plans or research the top retirement companies for high-net-worth portfolios.

By comparing policy structures, premiums, and long-term advantages, most families can find a solution that suits their wealth management objectives. Those who are uncertain or have particularly complex situations should consider consulting a professional who specializes in retirement insurance and estate planning.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...