Set Our Retirement Vision

Retiring at 60 with 2 million may feel both exciting and daunting. We want to ensure that our golden years reflect our lifestyle choices, family obligations, and long-term financial security. According to T. Rowe Price (T. Rowe Price), by age 60 we might need six to eleven times our current salary to stay on track. While this number varies for every household, aiming for around 2 million can be a solid blueprint, especially when paired with smart asset allocation, strategic savings, and tax efficiency.

We begin by clarifying our personal vision. Do we want to travel extensively? Are we considering part-time work or looking to spend more time with family? Clear answers to these questions shape our financial decisions and keep us motivated in our savings journey. When we know our why, we can build a retirement strategy that supports it.

Build a $2 Million Nest Egg

To reach 2 million in savings, we usually need a disciplined plan that starts with contributing 10 to 15 percent of our income each year. This figure often includes any employer match we might receive. Regular contributions to vehicles like 401(k) accounts, IRAs, or even Roth 401(k) plans can harness the power of compounding over time.

- Start Early for Growth

If we begin saving in our 20s or 30s, we give our money more time to compound. Even small additional contributions, such as an extra $50 per month, could translate to tens of thousands more by retirement (SmartAsset). - Revisit the Plan Regularly

Our income and spending habits change. It helps to review retirement contributions at least once a year and adjust upward when possible. If we get a raise or a bonus, adding a portion to our retirement fund can significantly accelerate our progress.

Structure Our Retirement Portfolio

Building a robust portfolio is key to retire at 60 with 2 million. Diversifying among stocks, bonds, and other assets helps balance risk and reward. A common tactic is to shift gradually from more aggressive assets toward conservative holdings as we approach 60.

- Equities vs. Fixed Income

Stocks often drive long-term growth, while bonds tend to provide stability and income. By our 60s, investment models call for a more moderate to conservative equity position, such as 60 percent in stocks and 40 percent in bonds (T. Rowe Price). - International Exposure

Holding positions in developed and emerging markets outside the United States can help further diversify our portfolio. Some asset allocation strategies recommend 25 to 30 percent in international equities, depending on risk tolerance.

For more tips on adjusting our allocations, we can check out ways to refine our retirement asset allocation. Balancing growth and protection can help preserve capital as we gear up for our 60s.

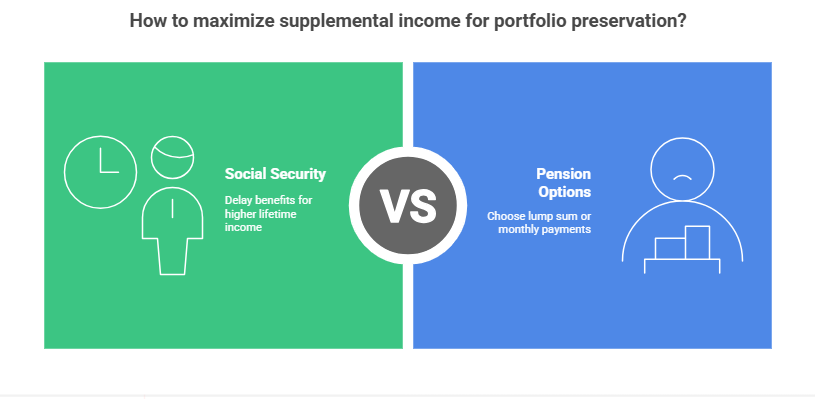

Maximize Supplemental Income

Even with 2 million saved, we might want additional income streams to preserve our portfolio. Between Social Security benefits, rental income, or part-time consulting, every supplemental dollar can delay the need to tap investments.

- Timing Social Security

We can typically claim benefits as early as 62 or wait until 70 for higher monthly payouts. Delaying benefits by even a few years can significantly increase total lifetime income (Farther). - Pension Insights

If we anticipate receiving a pension, we may decide whether a lump sum or monthly payments is best. For more on that, we can explore pension vs annuity or investigate if combining a pension and a 401(k) is possible by learning can you have a pension and 401k.

Stress-Test the Plan

Before finalizing our retirement blueprint, it is wise to run stress tests. Tools like Monte Carlo simulations can estimate how our portfolio might hold up across varying market conditions. For example, a $2 million portfolio may see its probability of lasting 35 years drop significantly if we withdraw $7,000 per month (Covenant Wealth Advisors).

- Simulate Different Scenarios

We should consider best- and worst-case market returns, increases in healthcare expenses, and unexpected life events. By modeling these possibilities, we can pinpoint potential gaps in our plan. - Adjust as Needed

If stress-testing shows our withdrawals might deplete the portfolio too soon, we may decide to reduce monthly spending, add an annuity, or rethink our investment strategy. A flexible premium deferred annuity might be a tool to help secure consistent future income.

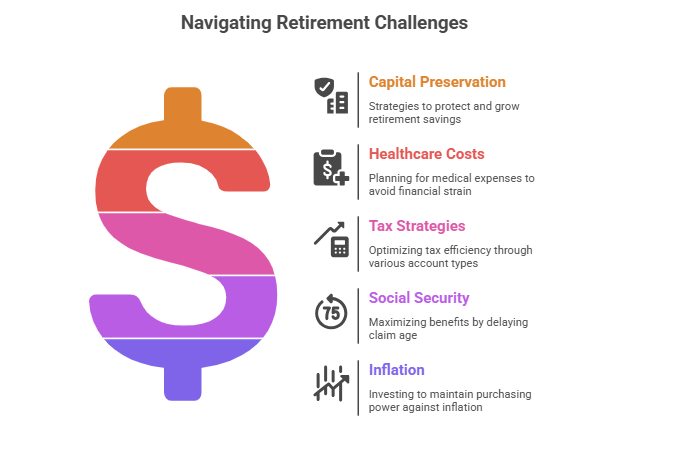

Top Retirement Queries Demystified

In one breath, the five most common queries about how to retire at 60 with 2 million revolve around capital preservation, healthcare costs, tax strategies, Social Security, and inflation. Below, we briefly address each concern:

- Capital Preservation:

We can mitigate downturn risks by diversifying and gradually shifting to more conservative assets. - Healthcare Costs:

Planning for medical bills through Medicare, supplemental insurance, or an HSA is critical to avoid large out-of-pocket expenses. - Tax Strategies:

Using a mix of taxable, tax-deferred, and tax-exempt accounts (like Roth IRAs) may optimize tax efficiency. - Social Security:

Delaying benefits until full retirement age or even 70 often increases monthly payouts. - Inflation:

Investing a portion of our portfolio in equities, inflation-protected bonds, or real assets may help maintain purchasing power.

For broader ideas on retirement living, we can explore what to do when u retire or browse retirement investment options for fresh perspectives.

Building Blocks for a Confident Retirement

Hitting the 2 million mark by age 60 is achievable through clear goal-setting, disciplined saving, and careful investment selection. We want to:

- Contribute consistently, aiming for 10 to 15 percent of our income.

- Diversify our portfolio with both domestic and international equity, plus a balanced bond mix.

- Consider supplemental income streams like part-time work or rental properties.

- Stress-test withdrawal rates and adjust for tax, healthcare, and inflation realities.

Our ultimate objective is to retire confidently without worrying about outliving our resources. By fine-tuning our plan along the way and monitoring changes in our personal and economic environment, we can keep our retirement on track. If we ever need more guidance on broader topics, we can also research top retirement companies or learn how to buy retirement insurance.

We hope these strategies help shine a light on how to retire at 60 with 2 million. Let us remember that every investor’s journey is unique and deserves a personalized approach. After all, retirement is more than a financial milestone, it is our chance to enjoy the life we have worked so diligently to build.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...