I remember feeling overwhelmed when I first started looking into retirement investment options. There were so many plans, each with its own twists. Over time, I settled on a handful that I truly believe in for sustained growth. In this post, I’ll share my personal shortlist and why each one earns my trust.

My Go-To Retirement Investment Options

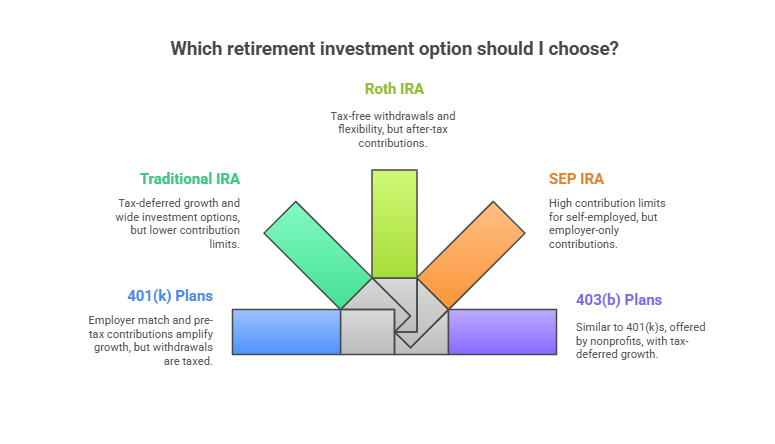

401(k) Plans

I’ve always liked the structure of 401(k) plans. They’re employer-sponsored program(s) where you can contribute pre-tax funds, and many employers offer a matching percentage. The IRS outlines several variations, including traditional 401(k)s and Roth 401(k)s (IRS).

- Why I trust them: Consistent employer match helps turbocharge my contributions.

- Growth factor: Pre-tax contributions let you invest more upfront, and that can amplify compounding over time.

- Potential pinch point: You’ll owe taxes at your ordinary income rate during retirement if you use a traditional 401(k). For Roth 401(k)s, however, qualified withdrawals come out tax-free.

Traditional IRA

A Traditional Individual Retirement Arrangement (IRA) is another key piece of my portfolio. Contributions may lower your taxable income in the current year, but you’ll pay taxes at withdrawal.

- Why I trust it: I can pick from a wide range of investment products, from mutual funds to blue-chip stocks.

- Growth factor: Tax-deferred compounding can add significant momentum to my nest egg.

- Potential pinch point: The annual contribution limit is lower than most 401(k) plans. Still, I find it a great companion to my employer-sponsored account.

Roth IRA

I love the flexibility of Roth IRAs because contributions are made with after-tax dollars, but qualified withdrawals are tax-free (U.S. Bank).

- Why I trust it: Once I pay taxes upfront, my earnings can grow untouched. In retirement, tapping this account doesn’t raise my taxable income.

- Growth factor: Those tax-free withdrawals are especially handy if I anticipate higher tax rates later in life.

- Potential pinch point: If I need the money early, I can remove my contributions (but not earnings) without an early withdrawal penalty, as long as I follow IRS guidelines.

SEP IRA

When I took on consulting work, I discovered the benefits of a Simplified Employee Pension (SEP) IRA. It offers higher annual contribution limits, which is ideal for self-employed individuals or small-business owners (Investopedia).

- Why I trust it: The generous contribution ceiling lets me squirrel away more money whenever I experience a good year.

- Growth factor: A flexible option that keeps compounding the same way a Traditional IRA does.

- Potential pinch point: Only employers or self-employed individuals can contribute, so it’s not an option for everyone.

403(b) Plans

Sometimes called tax-sheltered annuities, these are similar to 401(k)s but typically offered by certain nonprofit organizations and public schools (IRS).

- Why I trust it: I like that 403(b) plans mirror much of a 401(k)’s convenience but cater to roles in education or charitable work.

- Growth factor: Contributions can grow and compound tax-deferred, and some employers match funds.

- Potential pinch point: Like a 401(k), the withdrawals are taxed at ordinary income rates unless you opt for a Roth 403(b).

How I Balance Risk And Growth

I’ve learned that no single plan guarantees smooth returns forever. For me, it’s about finding the right blend. Younger savers can lean into more aggressive investments, such as equities, because they have time to recover from market downturns (Ascensus). Closer to retirement, I plan to favor steadier assets like bonds or dividend-paying stocks. Finding harmony here is important, so if you’re wondering how to allocate everything, retirement asset allocation might be worth exploring.

By spreading money across multiple accounts, I also gain flexibility in how and when I withdraw. For instance, I can tap salted-away funds in a Roth IRA without immediately bumping into a higher tax bracket, and I can preserve my Traditional IRA or 401(k) balances until required minimum distributions kick in. If you’re curious whether you can divide contributions between a pension and a 401(k), check out can you have a pension and 401k for more details.

My Final Word

Retirement accounts are more than just a savings hold; they’re my primary engine for long-term security. I combine multiple options, prioritize consistent contributions, and keep an eye on tax considerations. This strategy helps me pursue growth while staying nimble enough to make adjustments as I inch closer to retirement.

Still have questions about retirement investment options in just one sentence, like which is best to start with, how to manage risk, whether you can roll over funds penalty-free, how to handle taxes, or when to rebalance your portfolio? My best advice: chat with a trusted financial professional and map out a plan that fits your lifestyle and needs.

No single option outperforms in every scenario, but with a balanced approach, I’ve found that these plans can deliver the growth I need. If you’re still weighing your choices or looking for new angles, you might also check out pension vs annuity for additional insights. Here’s wishing you success in your own retirement journey!

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...