Financial planning in retirement can feel like a balancing act. We want to preserve our hard-earned wealth, minimize taxes, and still enjoy our golden years. The good news is that, with some clear strategies, it’s possible to create a blueprint that addresses all these priorities. Below, we’ve compiled an essential guide for high-net-worth individuals, outlining the steps we believe are vital to secure financial peace of mind.

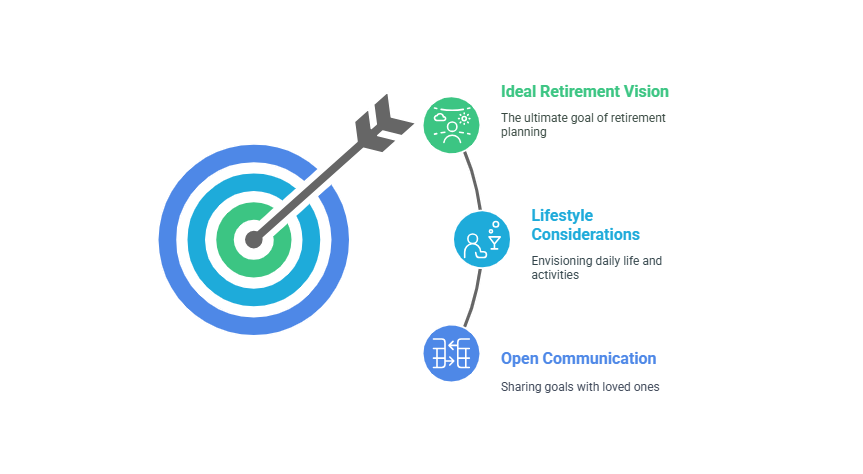

Set Your Retirement Vision

Before honing in on numbers and tax brackets, it helps to start with a clear picture of your ideal retirement. Are you planning to travel, support a family business, or leave a sizeable inheritance for the next generation? Understanding your goals allows you to shape your financial plan accordingly. If you’re seeking additional context on foundational concepts, we recommend reviewing our retirement planning basics.

Clarify Personal Priorities

- Consider your lifestyle: Where do you envision living, and what activities take priority?

- Talk openly with loved ones so everyone understands shared goals.

- Write these objectives down as a guide, then revisit them each year to track progress.

Plan Your Savings Targets

For most of us, the next step is to determine specific savings milestones. Various guidelines suggest saving roughly 15% of annual income toward retirement, including employer contributions, though high-net-worth individuals may need to adjust that figure based on personal circumstances (Fidelity).

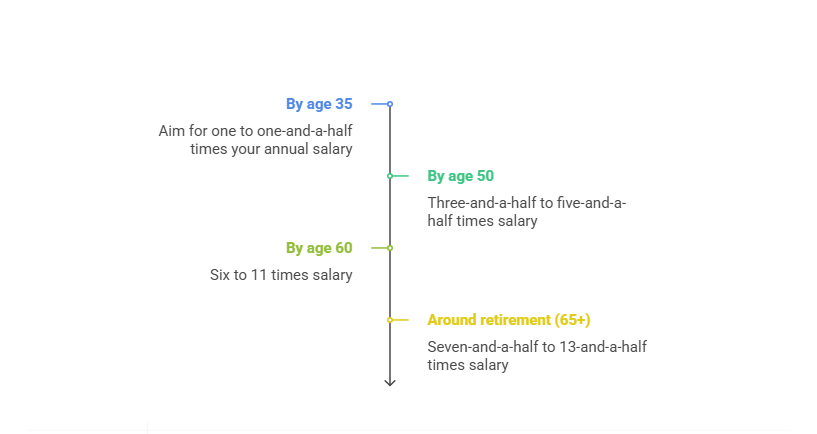

Consider Age-Based Benchmarks

- By age 35: Aim for one to one-and-a-half times your annual salary.

- By age 50: Three-and-a-half to five-and-a-half times salary.

- By age 60: Six to 11 times salary.

- Around retirement (65+): Seven-and-a-half to 13-and-a-half times salary (T. Rowe Price).

These numbers serve as rough markers. If you’re unsure where to start, our retirement questions to ask might help you re-evaluate your personal timeline.

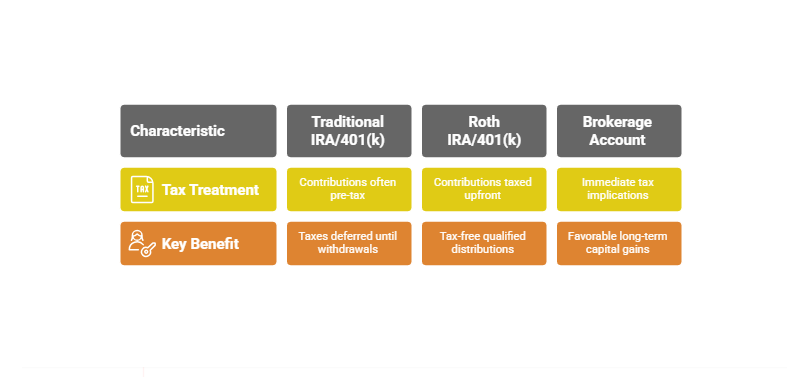

Select Tax-Advantaged Accounts

| Account | Tax Treatment | Key Benefit |

| Traditional IRA/401(k) | Contributions often pre-tax | Taxes deferred until withdrawals, can reduce current taxable income |

| Roth IRA/401(k) | Contributions taxed upfront | Tax-free qualified distributions, no required minimum distributions |

| Brokerage Account | Immediate tax implications | Longer-term capital gains rates can be favorable, flexibility in withdrawals |

Retirement accounts are not created equal. From Traditional IRAs to Roth 401(k)s, each has unique tax implications that can significantly influence long-term outcomes (IRS).Strategy Tips

- Diversify across accounts to manage taxable income in retirement (Synchrony).

- Consider Roth conversions strategically during lower-income years.

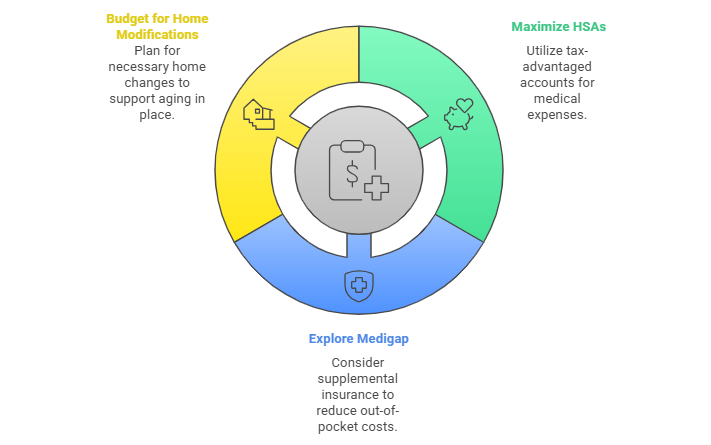

Factor In Healthcare Costs

Healthcare can be a major financial wildcard. A couple might spend hundreds of thousands on medical care throughout retirement, and Medicare doesn’t cover everything (Sammons Retirement Solutions).

Steps to Prepare

- Max out Health Savings Accounts (HSAs) if available, for tax-deductible contributions and tax-free qualified medical withdrawals.

- Explore Medigap or supplemental insurance to limit out-of-pocket expenses.

- Budget for potential home modifications if aging in place is a goal.

Account For Unexpected Events

We all hope for smooth sailing, but an emergency fund, typically covering at least six to twelve months of living expenses, can shield retirement portfolios from sudden costs (Mutual of Omaha).

Common Surprises

- Home repairs or renovations for accessibility

- Supporting adult children through financial or health challenges

- Market downturns that affect investment returns

Diversify Your Retirement Income

Relying on a single income stream might leave you vulnerable. Allocating assets across stocks, bonds, annuities, real estate, or part-time business ventures can offer greater stability (U.S. Bank).

- Annuities can guarantee monthly payments.

- Dividend-paying stocks can provide periodic income.

- Rental real estate offers potential appreciation and regular cash flow.

We often hear questions about withdrawal schedules, strategic tax moves, handling rising healthcare costs, earning more income post-retirement, and estate distribution details, all tied to the broader conversation of financial planning in retirement.

Review And Refine Regularly

Your plan should evolve with life changes, tax law updates, or shifts in personal goals. Setting a routine to revisit your budget, investment performance, and estate plans is key.

Annual Check-In

- Re-assess risk tolerance and asset allocation, especially if markets fluctuate.

- Update beneficiary designations and estate documents.

- Adjust withdrawal strategies to stay within safe withdrawal rates of 4%–5% (Fidelity).

If you’d like a simple refresher, see our retirement planning checklist. It can keep you on track and give you peace of mind.

Conclusion

We hope these ideas bring more clarity to your financial planning in retirement. The goal is to shape a strategy that supports your lifestyle while preserving your legacy for future generations. If you’re looking for inspiration on finding a new sense of purpose after exiting the workforce, you might enjoy our article about building a purposeful life after retirement.

As with any major financial decision, we encourage you to consult with professionals who understand your goals and can offer bespoke advice. With ongoing attention and smart choices, retirement can be the fulfilling chapter you’ve always imagined.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...