Many of us face situations where we prefer conservative but effective short term investment plans for 6 months. Perhaps we anticipate a significant expense soon, or we simply want a safe place to hold funds briefly without sacrificing every potential gain. In this discussion, we will review various investments that can fit a half-year strategy and guide you on balancing risk, return, and liquidity. Our perspective is rooted in helping high-net-worth households preserve capital while setting the stage for long-term goals.

Understand These 6-Month Plans

Short-term investments often prioritize safety and flexibility over higher returns. We know that protecting principal is essential for anyone expecting a liquidity event or simply parking funds briefly. While short-term options generally carry lower yields than longer-horizon products, they cushion against market volatility and allow quick access to cash whenever needed.

Short-term investment vehicles are especially useful when you cannot afford to tie up capital for years. Six months might be enough time to wait out a transitional phase, finalize a business sale, or prepare for another major purchase. In these scenarios, it is critical to select products that balance growth with liquidity and maintain a risk level that aligns with your tolerance.

Explore Key Vehicles

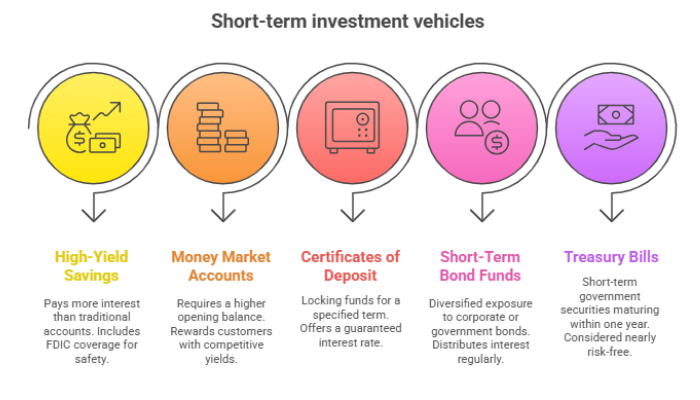

High-Yield Savings Accounts

A high-yield savings account pays more interest than most traditional savings accounts, and it often includes Federal Deposit Insurance Corporation (FDIC) coverage for safety. Many of these accounts have no strict minimum balance requirements, and the money remains accessible at any time. According to Bankrate, this investment type is ideal for risk-averse individuals who prefer straightforward account management and a predictable rate of return.

Key benefits:

- FDIC-insured up to $250,000

- Easy access to funds

- Straightforward setup and minimal fees

Money Market Accounts

Money market accounts are another popular bank product that generally require a higher opening balance but reward customers with competitive yields and, in many cases, check-writing or debit card privileges. They allow quick access to cash, making them ideal if you have unplanned expenses in the next six months.

Key benefits:

- FDIC-insured, provided it is a bank product

- Often offers a higher interest rate than standard savings

- May include check-writing capabilities

Certificates of Deposit

Certificates of Deposit (CDs) involve locking away funds for a specified term, such as 3, 6, or 12 months, in exchange for a guaranteed interest rate. For a six-month timeframe, CDs can offer a useful balance between predictability and rate of return. However, early withdrawal penalties do apply. If you are certain your funds can stay untouched for exactly six months, a CD might work well.

Key benefits:

- Guaranteed interest for the entire term

- FDIC-insured at most banks, up to $250,000

- Predictable returns that often surpass base savings rates

Short-Term Bond Funds

Short-term corporate bond funds or U.S. government bond funds can be suitable for those looking to diversify. Corporate bond funds bundle multiple bonds from different companies, distributing interest on a regular basis. Government bond funds invest in products such as Treasury bills or Treasury notes, typically offering lower yields but also lower risk, as they are backed by the U.S. federal government (Bankrate).

Key benefits:

- Diversified exposure to either corporate or government bonds

- Monthly or quarterly interest payments

- Low-to-moderate risk depending on bond quality

Treasury Bills

Treasury bills, often called T-bills, are short-term government securities typically maturing within one year. They are considered nearly risk-free, and investors can buy them directly from the U.S. Treasury or via brokerage accounts like Fidelity or Charles Schwab (CNBC Select). If you prefer extreme stability and have a strictly defined six-month horizon, T-bills can fill that need effectively.

Key benefits:

- Backed by the U.S. government

- Highly liquid

- Short maturity terms, sometimes as brief as a few weeks

Weigh Risk And Liquidity

Our advice is to weigh each option’s yield against the level of access you may need. If you anticipate sudden cash requirements, high-yield savings accounts or money market accounts provide ample flexibility. If you have precise timing for your next financial step, a short-term bond fund or a CD with a six-month maturity can offer potentially higher returns. For the ultimate safety net, T-bills and government bond funds present minimal credit risk but typically offer modest growth.

When selecting products, you should also think about your broader investment strategies. Some individuals use short-term vehicles to preserve capital while they explore alternative investment solutions. Others keep a portion of their liquidity in these instruments for everyday needs, ensuring long-term holdings remain untouched.

Manage Our Six-Month Strategy

We typically recommend diversified allocations to offset market changes. Pairing a high-yield savings account with a short-term bond fund can optimize both accessibility and a moderate income stream. If you have a fixed date for needing funds, consider combining a six-month CD with a money market account as backup liquidity.

A question you might have is, “Are they safe, how quickly can funds be accessed, are taxes complicated, do yields vary, and which account is best for short term investment plans for 6 months?” The answers depend on your daily cash flow demands, tolerance for interest rate shifts, and how comfortable you are locking in your money.

Many of our clients prefer to build an emergency cushion equal to six or more months of expenses, placing part of it in easily accessible options while letting the remainder earn a higher yield. This layered approach ensures that any urgent need for cash can be met without derailing long-term goals.

Final Thoughts

Short-term investment plans, especially those structured for a six-month horizon, fit well for preserving capital without sacrificing every potential return. By mixing manageable risk with liquidity, our clients maintain the flexibility to act on new opportunities. Whether you opt for a high-yield savings account, T-bills, or a carefully timed CD, your overarching goal should be to protect your principal and keep financial options open.

If you would like to explore more sophisticated allocations or discuss how these short-term tactics might complement your estate planning, take a look at our broader investment strategies or reach out to us directly. A six-month plan can be a small but impactful part of a larger portfolio designed to meet both short- and long-range goals.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Investment Firms in Los Angeles to Consider

Los Angeles is home to a diverse and dynamic financial...

Investment Firms in New York to Consider

Choosing the right investment firm is crucial for achieving your...