We have long relied on an individual investment account to expand our portfolios meaningfully, maintain flexibility over our assets, and keep a close eye on tax considerations. This type of brokerage account, also known as a taxable account, offers a straightforward way to purchase stocks, mutual funds, and exchange-traded funds (ETFs) without the contribution limits of retirement-focused alternatives. From our own experience, it can be an integral piece of a well-rounded wealth strategy.

Explore The Basics

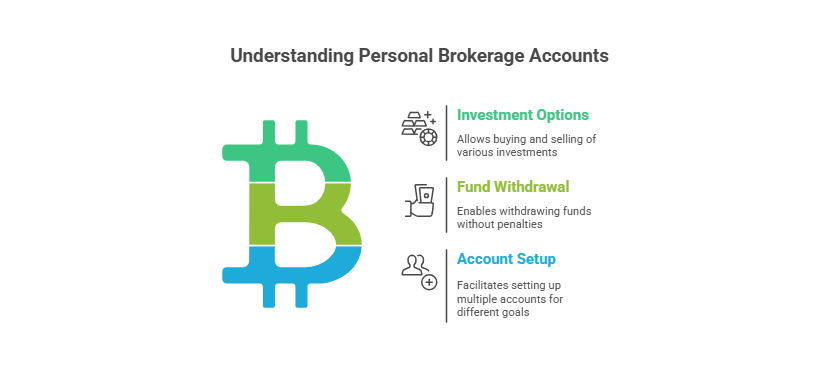

We believe that understanding the simple mechanics of a personal brokerage account is the first step toward making informed decisions. Essentially, it allows us to:

- Purchase and sell a wide range of investments (stocks, bonds, ETFs, and more).

- Withdraw funds at any time without early withdrawal penalties (although capital gains taxes may apply).

- Set up multiple accounts for different purposes, whether for our everyday investment needs or more specialized goals.

For those seeking in-depth background, you can check out our investment education resources. Meanwhile, some providers, such as TIAA, have introduced zero-commission options for listed stocks and ETFs, lowering barriers for both new and seasoned investors.

Compare Different Brokerages

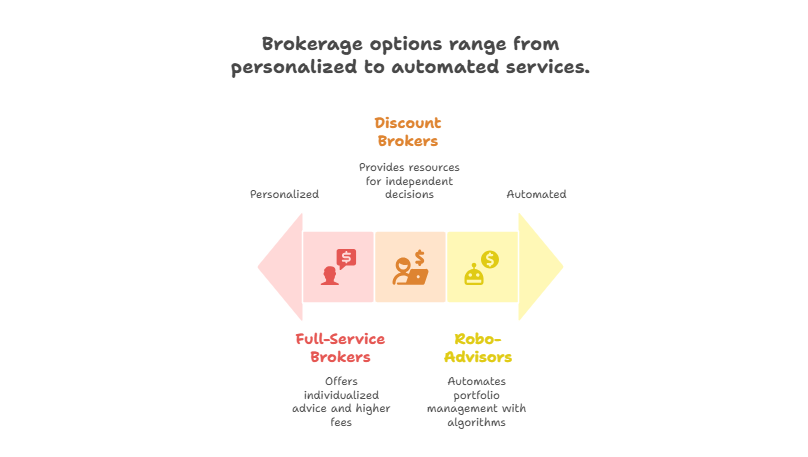

We all know that choosing where to open a brokerage account can be daunting. Different firms offer varying fee structures, research tools, and levels of advisory support. Here are three broad categories we have explored:

- Full-Service Brokers

- Provide individualized advice

- Often charge higher fees or commissions

- May be suitable for those seeking extensive guidance

- Discount Brokers

- Usually have lower fees

- Offer resources to help us make our own decisions

- Good fit for confident, hands-on investors

- Robo-Advisors

- Automate portfolio management with algorithms

- Typically invest in ETFs but limit personal customization

- Lower overall costs, but less flexibility

If you are just starting out, it might be worth reviewing the best brokers for beginners to see which platform aligns with your comfort level.

Balance Taxes And Growth

One major difference between a personal brokerage account and certain retirement accounts is tax treatment. When we sell assets at a profit, taxes depend on whether we held them short-term or long-term. Short-term gains tend to incur higher rates, while long-term gains are generally taxed at a more favorable rate (TurboTax). Although we cannot avoid these taxes entirely, we can manage them smartly:

- Maintain a mix of short-term and long-term positions where appropriate.

- Harvest losses to offset gains in a given tax year.

- Consider tax-advantaged investments, like municipal bonds, if it suits our overall plan.

Robo-advisor algorithms sometimes handle tax-loss harvesting automatically. However, if we prefer direct control, a discount or full-service broker might make it easier to monitor and optimize taxable events.

Expand With Retirement Options

An individual account works well on its own, but many of us also use IRAs (Individual Retirement Accounts) or company-sponsored plans alongside it. That way, we can simultaneously benefit from tax-advantaged growth for retirement while keeping a portion of our wealth liquid for other ventures. For instance:

- A Roth IRA allows after-tax contributions and often tax-free withdrawals in retirement.

- Traditional IRAs or 401(k)s delay taxes on contributions until retirement.

- A taxable account remains flexible, covering near-term goals or sudden opportunities.

According to Avidian Wealth Solutions, retirement accounts and brokerage accounts can complement one another, giving us a wider array of tools for both short- and long-range objectives.

Maximize Your Wealth Potential

We have found that a personal brokerage account is an excellent vehicle for investing beyond typical retirement parameters. Whether we want to capture timely market opportunities or diversify into new sectors, the account’s flexibility can keep us prepared. Here are a few ways we put it to use:

- Reinvest dividends to harness compounding returns

- Allocate a portion of assets to higher-growth stocks or alternative investments

- Combine with fee-only advisory services for tailored planning

Curious about other ways to enhance your financial foundation? Sometimes, exploring what are brokerage services can reveal further opportunities for growth and personalization.

One-Sentence FAQ Roundup

“What is an individual investment account, how does it differ from other brokerage accounts, are there tax advantages, who is eligible to open one, and when is the best time to set it up?”

We often hear these questions from individuals who want to make the most out of their investment journey. Getting clarity on each of these points can streamline your decision process and help you avoid costly surprises down the road.

Conclusion And Next Steps

We like to think of a taxable brokerage account as the workhorse in our overall portfolio. It grants us freedom to invest when and how we see fit, ensuring our wealth strategy aligns with our evolving goals. Whether you are looking to expand beyond retirement accounts or simply invest more proactively, consider how this flexible approach might support your ambitions.

If you are still refining your investment plan, try diving deeper into understanding investments. Also, feel free to speak with an independent advisor about customizing solutions that balance risk, liquidity, and returns. Ultimately, an individual investment account can be the key to opening new opportunities, strengthening long-term financial health, and fueling your next stage of growth.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Investment Firms in Los Angeles to Consider

Los Angeles is home to a diverse and dynamic financial...

Investment Firms in New York to Consider

Choosing the right investment firm is crucial for achieving your...