Many high-net-worth individuals realize that a thoughtful creative planning fee schedule can safeguard their wealth by promoting trust, clarity, and long-term value. This arrangement outlines exactly what services they are paying for, whether it involves building comprehensive strategies, handling assets, or coordinating multi-generational estates. With so many options available, understanding why fees matter and how they can influence overall financial management is essential.

Understanding a Creative Planning Fee Schedule

A fee schedule typically reveals how an advisory firm or wealth manager structures its charges. In many cases, the firm might use an annualized asset-based formula, adding more transparency to the overall cost. According to an overview from MagnifyMoney, Creative Planning charges 0.25% to 1.20% of assets under management, with the highest percentage applying to the first tier of assets.

Why Transparency Matters

A transparent schedule helps clients see:

- What portion of fees covers advisory services.

- Whether the firm charges separately for brokerage or sub-advisory.

- How the total cost might scale down as assets grow.

Being upfront about fees not only boosts accountability, but it also reduces surprises. This is especially relevant for families eyeing multi-generational plans, large liquidity events, or complex financial planning services.

Minimum Asset Requirements

Firms like Creative Planning often specify a minimum investment. Reports indicate they require at least $500,000 in investable assets, which ensures a certain level of net worth among clients. For individuals who meet these requirements, the firm includes comprehensive planning—covering everything from a financial plan example to estate-related nuances—without additional charges at certain portfolio thresholds.

Key Components to Consider

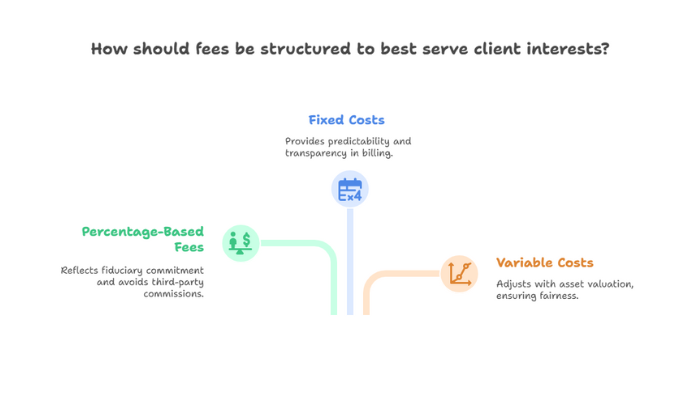

Most fee schedules account for advisors’ expertise, overhead, and profit margins. In the case of Creative Planning, the fee remains strictly percentage-based, without commissions from third parties (Creative Planning). This structure reflects a fiduciary commitment to act in the client’s best interest.

Fixed and Variable Costs

- Annual or quarterly charges are typically calculated based on the final day’s asset valuation.

- Administration fees like brokerage or transaction costs go to actual service providers, not the advisory firm.

- Periodic reviews ensure that these fees stay aligned with agreed-upon rates.

Staying mindful of each line item is vital for those who want to protect their estate and potentially pass assets on to future generations. Comprehensive planning often entails close attention to taxes, trusts, and financial management advice.

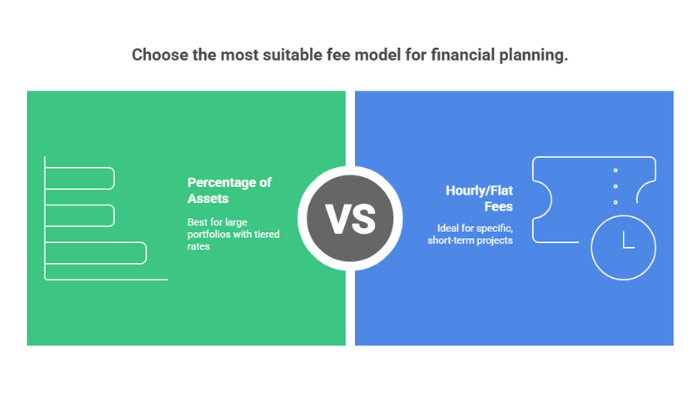

Comparing Common Fee Models

Although many high-net-worth households gravitate toward an annualized approach, a range of models exists. Some financial planners adopt hourly or project-based fees, while others prefer value-based strategies. Not all align equally with advanced strategies like investment and financial planning.

Percentage of Assets Under Management

This model charges a percentage based on the total investable assets. Families with significant portfolios often find that the more they invest, the lower the marginal percentage. For instance, Creative Planning uses a progressive tier system, so the rate might drop after the first $500,000 of assets.

Hourly or Flat Fees

Some prefer flat fees for tasks such as estate planning or business succession consulting. This approach offers budget certainty, though it might become costlier for larger, ongoing projects like financial planning for families who need deeper, consistent support.

Linking Fees to Value

Wealthy households frequently prioritize services like tax optimization, estate strategies, and risk management. A well-structured schedule ensures individuals pay proportionate to the expertise and commitment their advisors offer. This alignment creates better synergy and fosters loyalty, which can be crucial for a multi-year or multi-generational partnership.

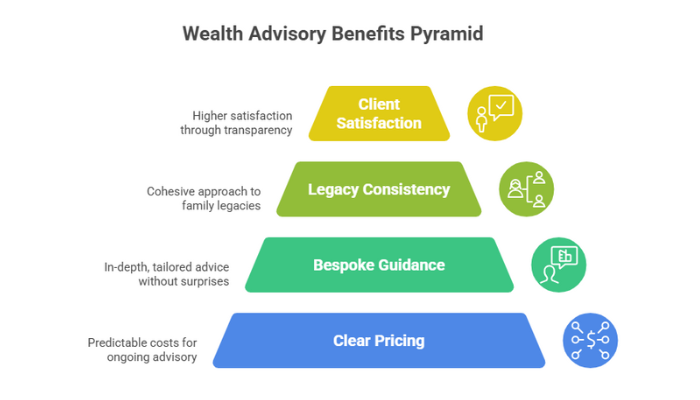

Potential Long-Term Benefits

- Clear, predictable pricing for ongoing advisory.

- In-depth, bespoke guidance without unexpected charges.

- Consistency in nurturing family legacies, especially if the approach remains cohesive.

Firms that focus on transparency often cite higher satisfaction among clients (BuzzBoard). Meanwhile, some might wonder how a creative planning fee schedule is structured, who benefits the most, whether it includes hidden charges, how it compares to commission-based models, or what the minimum investment requirement might be—all top considerations when evaluating an advisory firm.

Final Thoughts on Scheduling

A creative planning fee schedule shapes trust for many individuals managing substantial wealth. It typically outlines whether charges are all-inclusive or whether separate costs (brokerage, administrative, or transaction fees) might arise. By focusing on transparent cost breakdowns, experienced advisors can support high-net-worth families over the long haul.

Those who want customized estate strategies, ongoing reviews, or comprehensive finance plans can benefit from exploring how different firms handle fees. For instance, a percentage-of-assets model might fit individuals with evolving portfolios, while a flat fee may appeal to anyone needing one-time assistance. Ultimately, comparing schedules and confirming fiduciary obligations can lead to a wise partnership that bolsters generational wealth and peace of mind.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...