When you think about shaping a financial plan example that truly reflects your goals, it helps to picture where you stand now—and where you want to end up. Whether you’re a business owner, a tech executive with concentrated stock holdings, or simply someone looking to protect your legacy, crafting a clear road map can give you peace of mind. Interestingly, only about 35% of Americans have a goals-based plan for their finances (Modern Wealth Management). Let’s walk through some practical steps so you can feel confident in your decisions.

Start With A Clear Vision

Before you tackle numbers, lay out your priorities. Are you preparing for retirement, wanting to protect future generations, or rolling the proceeds from a major liquidity event into new ventures? Give yourself permission to dream a little. This big-picture approach ensures that every strategy you choose—like tax planning or establishing regular monthly contributions—connects to your personal aspirations.

Focus On Key Financial Details

- Identify all your income sources, from salary to rental income.

- Jot down expenses and separate them into needs, wants, and savings contributions.

- Keep an eye on debts and how swiftly you want to pay them off. The average household balance hovers around $104,000 in debt (Principal), so it’s a real concern for many.

If you haven’t yet, be sure to talk with a trusted advisor about financial planning services. An extra set of eyes can highlight cost-saving moves, like adjusting your tax filing approach or exploring more efficient ways to manage your assets.

Build Core Elements Into Your Plan

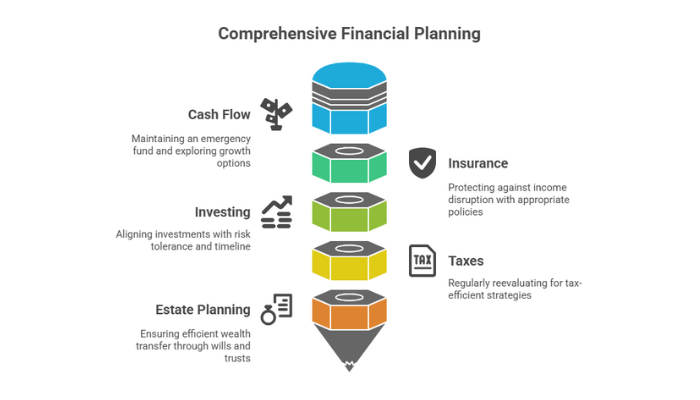

A solid financial plan tends to address these core categories: cash flow, insurance, investing, taxes, and estate considerations. Let’s break them down.

Secure Your Cash Flow

At a minimum, try to maintain an emergency fund that covers three to six months of living expenses. Research shows just over half of adults have three months set aside (Principal), so you’re not alone if you need to boost your safety net. You might also find it helpful to explore investment and financial planning options that can keep your extra cash growing.

Protect With The Right Insurance

One in four 20-year-olds faces a disabling condition before retirement (Principal), which means insurance coverage is more than a box to check. It’s your guardrail if something disrupts your income. Talk with a professional about policies for life, disability, or long-term care. This conversation can also cover the unique needs of high-net-worth families, like you might see in financial planning for families.

Invest For Your Future

Look for an investment strategy aligned with your risk tolerance and timeline. Spreading out your money through diverse assets usually reduces volatility. For truly robust planning, consider stress-testing your portfolio with a Monte Carlo simulation (PlanCorp), which explores how your plan performs under different market conditions. This helps confirm you’re prepared for both smooth and rocky times.

Map Out Taxes Wisely

Tax planning shouldn’t just be a once-a-year consideration. By reevaluating regularly, you can see if you qualify for tax-efficient strategies like Roth conversions or charitable contributions. Given that current tax rates could expire after 2025 (Modern Wealth Management), forward-thinking tax moves can save you substantially in the long run.

Establish An Estate Plan

Even if you’re young, a will prevents confusion about your assets. Larger estates typically require trusts, charitable strategies, or other specialized vehicles that ensure your wealth transfers efficiently. If you’re handling significant assets from stock options or major business sales, estate plans become even more essential.

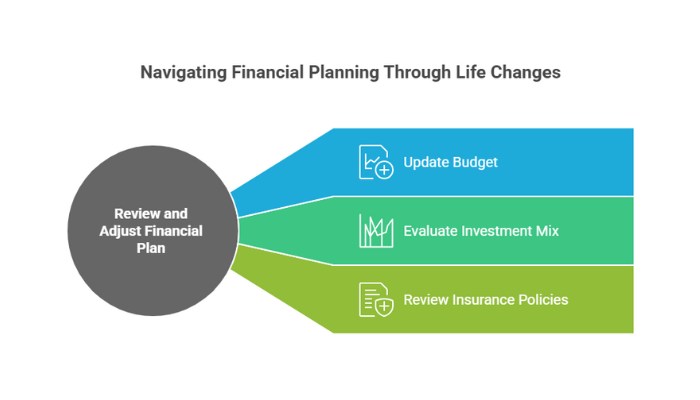

Review And Adjust Often

Once you’ve structured this financial plan example, you’ll want to keep it current. Major life changes like a career shift, the sale of a business, or a family addition all warrant a refresh. Experts recommend re-checking your plan at least once a year or any time your circumstances change significantly (U.S. Chamber of Commerce). During these reviews:

- Update your budget to reflect monthly inflows and outflows.

- Look at your investment mix and decide if you’re comfortable with any recent gains or losses.

- Evaluate insurance policies to see if new coverage is needed.

If markets shift or your personal circumstances change, regular adjustments can help keep your strategy on track. You can also coordinate with omaha financial planners or other specialized advisors if you need localized insight.

Consider A Practical Example

Imagine you’re a tech executive with a large amount of company stock. Your plan might:

- Sell some shares to free up cash for real estate or philanthropic goals.

- Transfer a portion into a retirement vehicle, such as a 401(k) or IRA, and use forward-looking tax strategies to reduce your tax burden.

- Set up a trust for your children’s education, ensuring assets grow with minimal tax hits.

Throughout, you’d regularly revisit and tweak these steps to align with new goals or market conditions. That’s precisely how a detailed yet flexible financial plan example can serve as your guide.

FAQs In A Single Sentence

If you’re exploring a financial plan example, you might ask: how do you begin, how should you handle existing debt, how often do you revisit it, do you need a pro advisor, and what about your estate planning details?

Final Thoughts

Ultimately, your financial plan is the framework for how you navigate wealth management, from immediate needs to long-term security. By setting clear goals, creating a plan that includes insurance, taxes, and estate considerations, and reviewing it regularly, you can feel confident about your progress. If you need more guidance, consider exploring comprehensive finance plans or seeking out financial management advice that’s tailored to your goals.

Try taking one small step today, such as checking your insurance coverage or revisiting your budget. You’ll quickly see that turning your dream scenario into a workable reality is easier when you actively shape and adapt your financial plan over time.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...