Step 1: Clarify My Financial Goals

I’ve learned that my first step is to understand what I really want from a financial advisor. Do I need help managing a sudden liquidity event, like the sale of a business? Am I hoping to reduce taxes or protect assets for my family down the line? Since finance can feel complex, it helps to write down my specific priorities. Having this list upfront keeps me focused when I start interviewing potential advisors.

You may ask how to choose a financial advisor with confidence: how do I find a fiduciary, which credentials matter, how do fees work, when should I seek references, and how do I measure trustworthiness, all in one sentence!

Step 2: Check Advisor Credentials

Once I know my goals, I look for professionals who can guide me accurately. Many reputable advisors start by earning a four-year degree in finance or accounting, often followed by specialized licenses like the Series 7 or Series 65 (per Investopedia). Designations such as Certified Financial Planner (CFP) or Chartered Financial Analyst (CFA) also indicate that they’ve passed rigorous exams and must uphold high ethical standards. If I want to see the typical path to becoming an advisor, I glance at resources like how to become a financial advisor.

Step 3: Compare Fee Structures

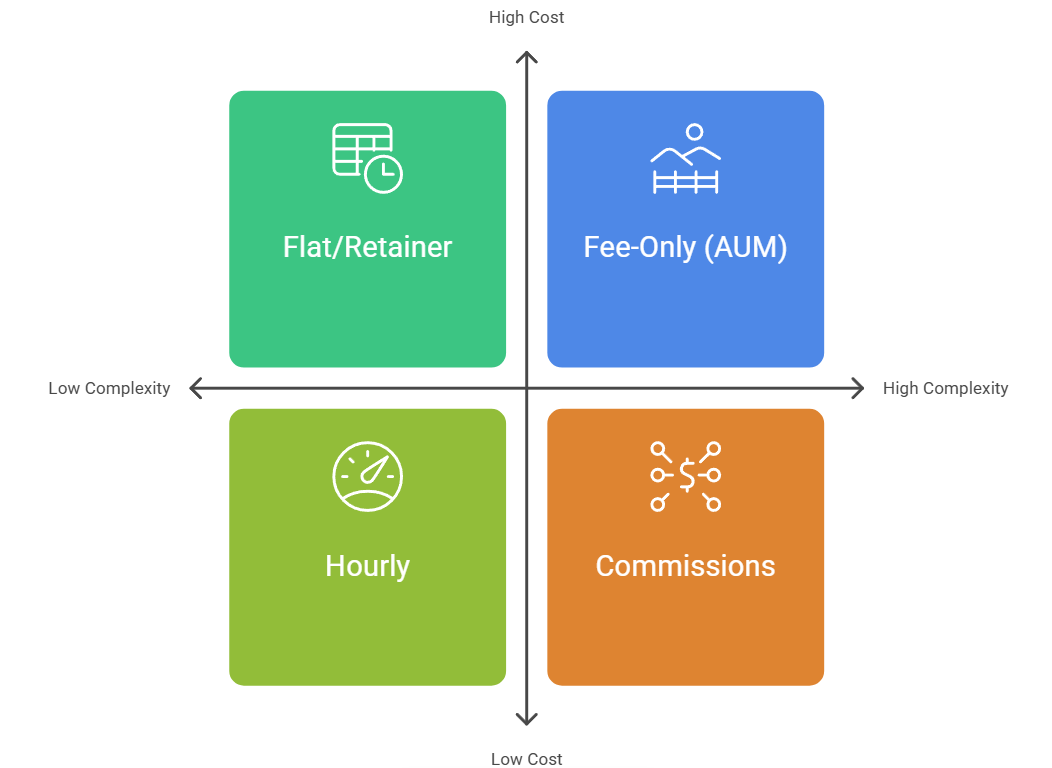

There are multiple ways financial advisors charge clients. I realize it’s crucial to know whether an advisor is “fee-only” (no commissions) or “fee-based” (may include product commissions). According to NerdWallet, typical fees can vary greatly depending on the structure:

| Fee Structure | Typical Range |

| Fee-Only (AUM) | 0.50% to 2.00% of assets per year |

| Flat/Retainer | $2,000 to $7,500 annually |

| Hourly | $200 to $400 per hour |

| Per-Plan Fee | $1,000 to $3,000 |

| Commissions | Often 3% to 6% of investment transactions |

I aim to ask questions about each advisor’s compensation model. If someone is fee-only, I know they’re paid only by me, not by third-party product commissions. For my own high-net-worth goals, a fee-only advisor can offer extra peace of mind that they act strictly in my best interest.

Step 4: Schedule A Screening Call

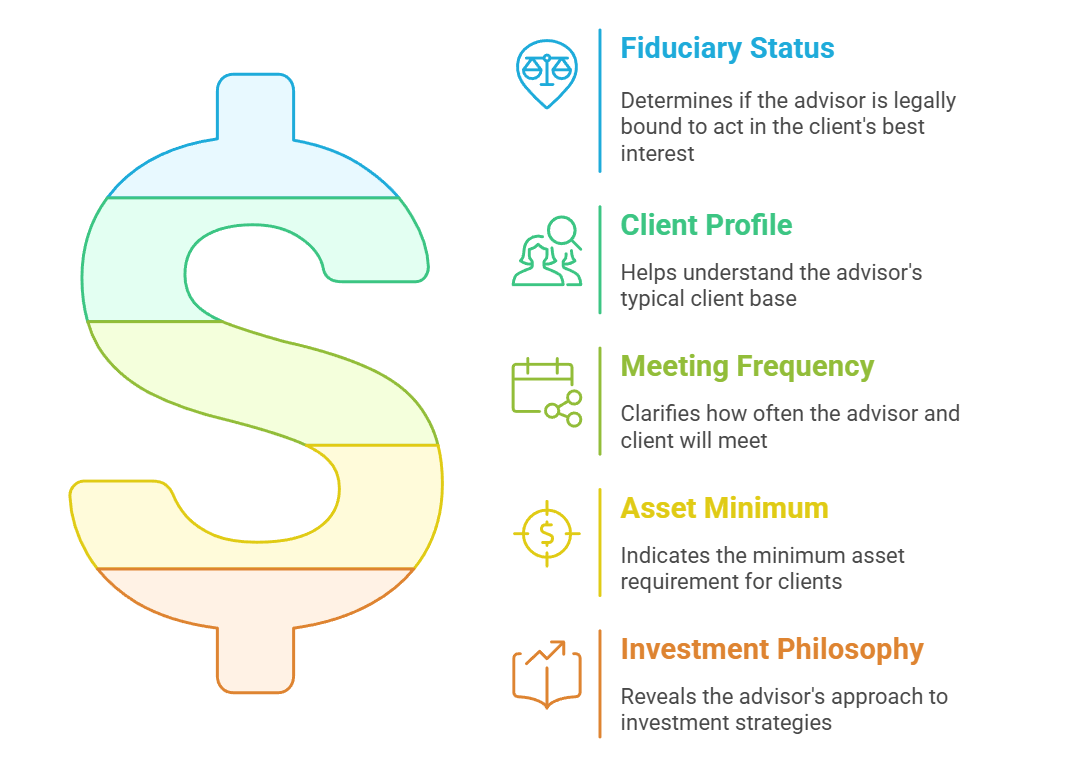

Before committing to extended meetings, I like to hop on a quick call to see if an advisor really fits. In fact, Kitces suggests using screening calls to gauge whether an advisor’s services match my assets and objectives. During this call, I typically ask:

- Are you a fiduciary?

- What’s your typical client profile?

- How often will we meet in a typical year?

- Do you have an asset minimum?

- What is your investment philosophy?

These questions help me decide if it’s worth proceeding. If the advisor seems distant, unclear, or reluctant to provide details, I consider looking elsewhere. If our conversation clicks, I’m more confident scheduling a longer consultation. Meanwhile, I also check references or see if they offer personal advisor services that align with my exact needs.

Step 5: Make My Decision

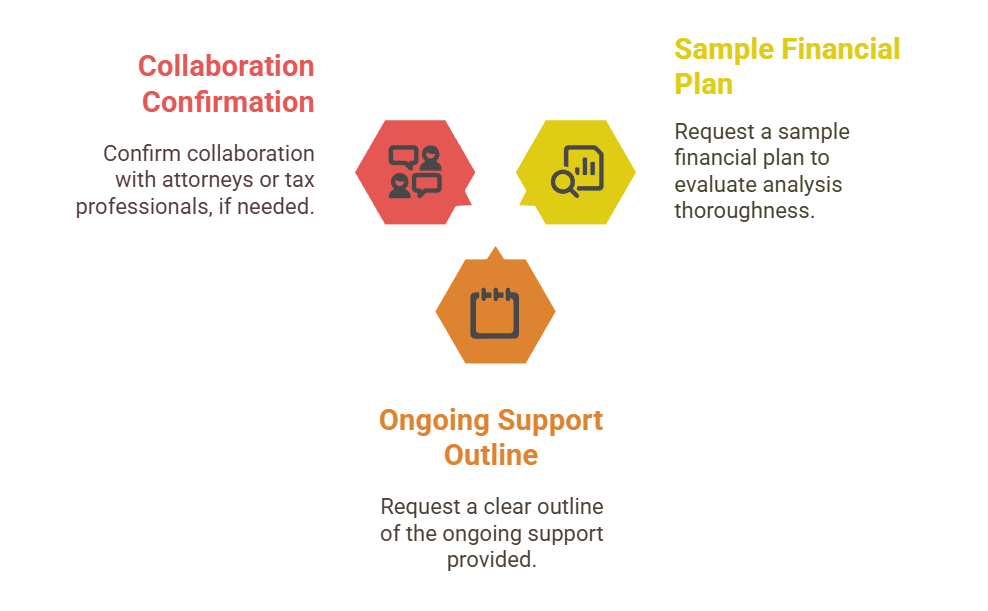

Once I’ve interviewed at least two or three prospective advisors, I weigh all the factors—fee structure, credentials, communication style, and references. By then, I typically have a clear sense of which advisor puts my interests first. If I come across an advisor who’s well-versed in wealth protection and estate planning, that extra knowledge may clinch it for me.

- I usually ask for a sample financial plan. This shows how thorough their analysis is.

- I request a clear outline of ongoing support, whether it’s quarterly check-ins or more frequent discussions.

- I confirm whether they collaborate with estate attorneys or tax professionals if that’s relevant to my family’s needs.

By this point, I’m ready to finalize my choice. Sometimes that means scheduling a face-to-face meeting to sign agreements or handle logistical details.

Quick Tips And Next Steps

- Never be afraid to ask direct questions about how someone is licensed or whether they have a financial broker license.

- Check references from current or past clients to get a sense of real-world experiences.

- If you’re still wrestling with big-picture financial questions, consider checking resources on who can i ask for financial advice.

Choosing an advisor is a personal decision that goes beyond mere qualifications. It’s about finding someone who understands my goals, communicates well, and is motivated to work for my best interest. I try not to rush the process. After all, this is about my long-term financial security.

I hope this tutorial helps you make a smart decision the next time you’re wondering how to choose a financial advisor. Ultimately, a trustworthy partnership can bring clarity, confidence, and consistent progress toward your biggest financial goals!

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...