Who can I ask for financial advice? I get this question often, and it makes sense. Whether I’m handling a substantial portfolio, preparing for a retirement transition, or juggling multiple income streams, the right advice can feel like a lifeline. I want to walk through key considerations so you can identify the guidance that truly fits your needs.

Identify Possible Advice Sources

Banks, brokerage firms, and even government agencies offer various forms of assistance. For instance, the Federal Deposit Insurance Corporation (FDIC) publishes resources that explain fundamental financial concepts and regulations. Your employer might also provide access to a 401(k) consultant or personalized guidance, especially if you work at a firm that values financial education. Some individuals prefer digital solutions, such as robo-advisors, for automated portfolio management. Others rely on human professionals who can give comprehensive wealth-planning feedback.

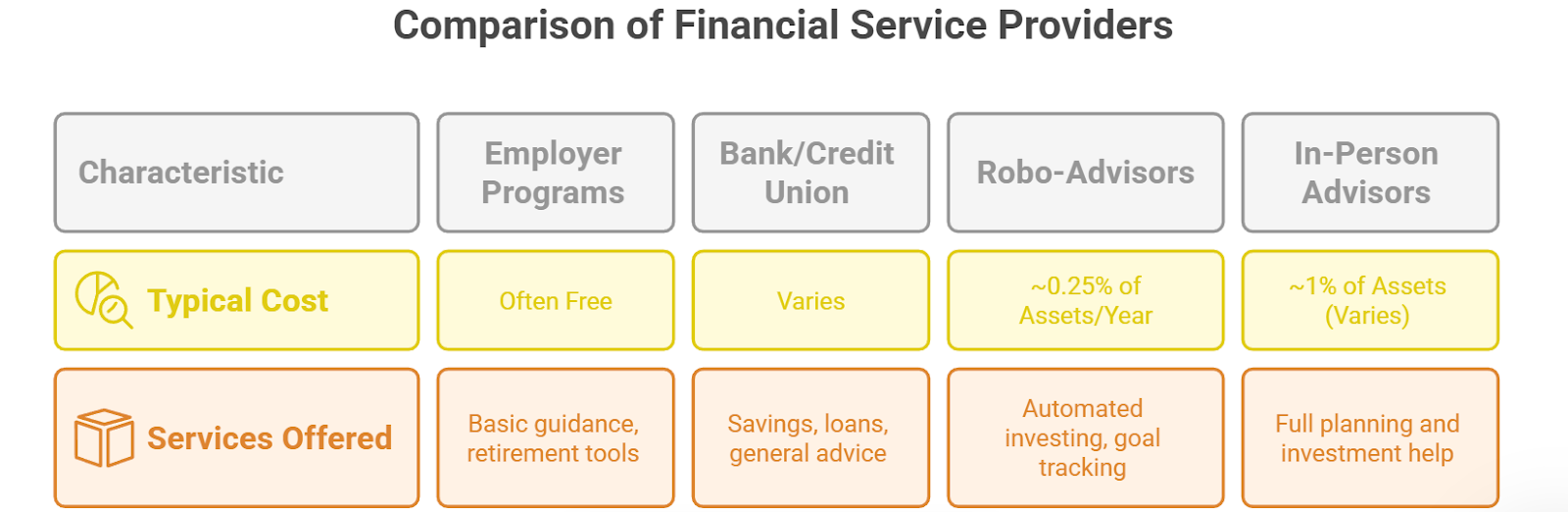

Comparing Popular Options

| Source | Typical Cost | Services Offered |

| Employer Programs | Often Free for Employees | Basic investing guidance, retirement tools |

| Bank or Credit Union | Sometimes Free, Sometimes Fee | Savings, loans, general advice |

| Robo-Advisors | ~0.25% of Assets/Year | Automated investing, goal tracking |

| In-Person Financial Advisors | ~1% of Assets (Varies) | Full suite of planning and investment help |

I know cost matters, but so does the breadth of expertise. It’s worth weighing both before moving forward.

Consider Advisor Fee Structures

| It can be confusing to figure out how advisors get paid. Some work on commissions for selling certain products, while others charge a percentage of assets under management. Fee-only advisors charge you directly, reducing potential conflicts of interest. Platforms like NerdWallet (NerdWallet) highlight that fee-only models often align more closely with a client’s best interests, particularly when big life events or larger asset bases are involved. If you’re curious about deeper personalized approaches, you might explore personal advisor services to get an idea of how these fee structures play out. |

Check Professional Credentials

| Licenses and certifications help me gauge an advisor’s expertise. In the United States, advisors typically must pass exams such as the Series 7 or Series 63 to sell securities (Investopedia). If they charge advisory fees, the Series 65 exam, or the Uniform Investment Advisor Law exam, is often required. Certifications like the Certified Financial Planner (CFP) or Chartered Financial Analyst (CFA) demonstrate additional training and a commitment to ethical standards. CFP: Focuses on comprehensive financial planning, including taxes, retirement, and estate planning. CFA: Specializes in investment analysis and portfolio management. Series 7, 63, 65: Core licenses that allow advisors to work across multiple states, charge fees, and sell various investment products. Before selecting someone, I always verify their license status and do a quick background check for any regulatory incidents or red flags on their Form ADV. |  |

Explore Free Or Low-Cost Help

| If you’d prefer to start small or simply test the waters, free and affordable choices abound. Some employers partner with financial education platforms, while online resources from the Federal Trade Commission (FTC) cover budgeting and consumer protection topics. Free consultations can also be found through certain advisory groups, which provide an initial assessment of your financial goals. These sessions let you see if an advisor’s style aligns with your comfort level before you commit. |

Seeking additional guidance on your career path in finance? You could read about how professionals enter the field on pages like how to become a financial advisor or financial advisory jobs. Even if you’re just curious about their background, it’s reassuring to know what training is common in the finance industry.

Look For Fiduciary Responsibility

A financial advisor’s fiduciary duty is crucial to me. It means they are legally obligated to put my interests first, regardless of product affiliations or commissions. Registered Investment Advisors (RIAs) and Certified Financial Planners (CFPs) often operate under this standard, so I pay close attention to that designation during my search. According to Savant Wealth Management, verifying fiduciary status can help me ensure that advice on asset protection, estate planning, and retirement strategies is truly unbiased.

Summary: Make An Informed Choice

With so many points to consider, it’s easy to feel overwhelmed. But the real question remains, who can I ask for financial advice and feel confident about it? My suggestion is to start by clarifying your main needs: retirement, estate planning, liquidity events, or long-term wealth management. Then, vet potential experts based on their credentials, fee structure, and regulatory standing. Always confirm they’re looking out for your best interests by checking for a fiduciary commitment. When you’re ready, you can also review specific steps for hiring a professional in how to choose a financial advisor.

When it comes to “who can I ask for financial advice,” people often ask in one breath about fee-only models, whether banks are trustworthy, how often to consult a pro, if robo-advisors suffice, and which credentials truly matter. If you keep those five questions in mind and match them with everything above, you’ll be well on your way to the guidance you deserve.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...