We often think about retirement as a calm destination, but the reality is there’s a maze of costs lurking in our 401(k) plans that we might not fully understand. In fact, “401k cost” can go well beyond a straightforward management fee. And sometimes, we’re left asking ourselves: “What are the typical plan fees, how do early withdrawals factor in, do catch-up contributions complicate fees, what if we pay extra for active management, and are these fees ever tax-deductible?” That’s a lot to unpack, but we’ll walk through it step by step so we can spot these hidden charges and keep more of our money where it belongs—in our future.

Understand 401(k) Costs

When we talk about 401(k) fees, we’re looking at three main areas: plan administration, investment management, and potential advisory fees. Each one chips away at our returns. For instance, a seemingly small difference in the annual fee can have a massive impact. According to research from Investopedia, a 0.5% fee over 35 years could mean $157,000 less in retirement savings compared to a zero-fee scenario (Investopedia). That’s not just pocket change, and it underscores why every percentage point truly matters.

Plan administrators typically charge for record-keeping and compliance testing. Meanwhile, mutual funds or ETFs within our plan come with expense ratios. Some charge more than others, so it’s worth checking the fine print. If we don’t pay attention, these expenses can stack up quickly.

Break Down Revenue Sharing

Revenue sharing is a lesser-known fee structure where plan costs hide inside certain mutual funds. Instead of proactively charging a transparent fee, these funds build administrative expenses into fund expense ratios (Employee Fiduciary). We might not even realize how much we’re paying because the true figure isn’t always obvious on our statements.

This setup grows more expensive as our balance increases. The amount we pay is based on a percentage of our plan’s total assets, which means the better our investments do, the more fees we hand over. And if our plan relies solely on revenue sharing funds, we could miss out on lower-cost options like certain index funds or ETFs that often don’t pay revenue sharing. That’s why switching to direct fees can help us see precisely what we’re spending and avoid those markups.

Consider Active Management

Some of us lean toward actively managed funds. The rationale is that professional managers may capture opportunities in less efficient markets or pivot during downturns (Sequoia). They can also provide extra diversification compared to index funds that concentrate heavily on large-cap stocks.

However, it’s no secret that actively managed funds often come with higher costs than their passive counterparts. We need to weigh the potential for outperformance against the drag of these fees, especially over the long term. According to a range of studies, active funds don’t always keep pace with simpler index options, but some investors value the flexibility that active managers can offer during volatile markets. The key is to do our homework so we’re comfortable paying for that expertise.

Focus On Transparency

One of the best ways to control 401(k) cost is to demand full transparency in our plan. When fees are charged directly instead of hidden in the expense ratio, we know exactly where our money is going. Direct fees can also let employers pay plan expenses from a corporate bank account, lowering participants’ overall costs and helping everyone save more (Employee Fiduciary).

It’s natural to wonder whether any of these fees might be deducted on our taxes. If we’re curious about jumping through the necessary hoops, we can check out are investment management fees tax deductible. Understanding which costs are deductible might give us a little relief at tax time, though specific rules vary.

Plan Our Future

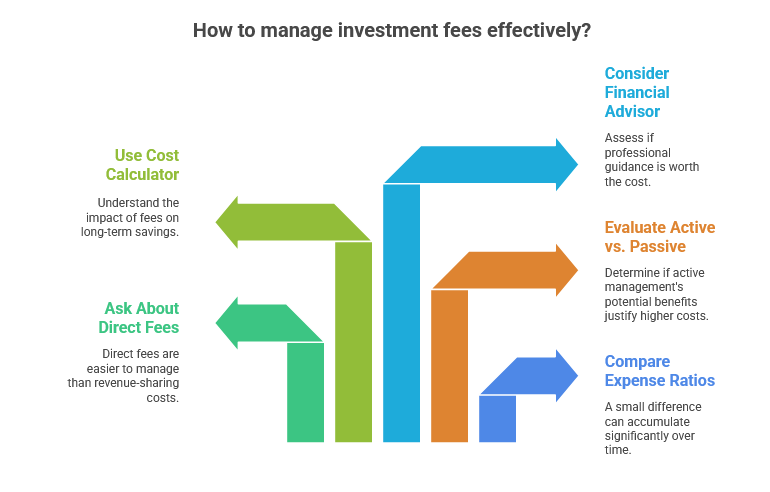

Fees can seem confusing, but there are ways to keep them in check:

- Compare expense ratios: Even a 0.1% difference can add up over the decades.

- Ask about direct fees: They may be simpler to spot and easier to manage than revenue-sharing costs.

- Evaluate active vs. passive: See if the potential upside of active management is worth the higher expense ratio.

- Use an investment cost calculator to see how these fees affect our nest egg.

- If we need personal guidance, learning about the cost of a financial advisor can clarify whether professional help is worth it for our situation.

Once we’re armed with the right information, we’re in a better position to weigh our choices and adjust our savings strategy accordingly. Over time, minimizing fees can free up a substantial chunk of our retirement income. That means more flexibility for what truly matters—like enjoying our next chapter, whatever that looks like for us.

In the end, cutting through the noise around 401(k) cost makes a real difference to our financial security. By exploring plan fees, embracing transparency, and deciding how actively we want our money managed, we protect our hard-earned savings. Let’s keep the conversation going, stay curious about our plan statements, and keep an eye on what we’re really paying. Our future selves will thank us.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...