Retirement asset allocation sits at the heart of a sound financial plan, especially for those of us looking to protect our wealth and fund a comfortable lifestyle. We believe it’s not just about spreading your money around different investments. Instead, it’s about building a flexible strategy that can weather market storms and consistently provide income when we need it.

Understand The Basics

What It Means

When we talk about retirement asset allocation, we’re referring to how we divide our nest egg among categories like stocks, bonds, and cash. Each category plays a unique role — stocks aim to grow your money, bonds and cash aim to stabilize it. The right mix usually depends on factors like your timeline, risk tolerance, and total wealth. According to T. Rowe Price, having 11 times your salary saved by retirement might be a good ballpark. This figure can vary, but it highlights how important it is to get started early.

Why It Matters

Allocation helps manage volatility and curb emotional decisions. A portfolio loaded with stocks can rise fast, but it can also fall just as quickly, so having bonds can smooth out that rollercoaster. Meanwhile, a stash of cash or near-cash assets can cover short-term needs so that we don’t have to sell stocks or bonds at the worst possible time.

Shape A Balanced Portfolio

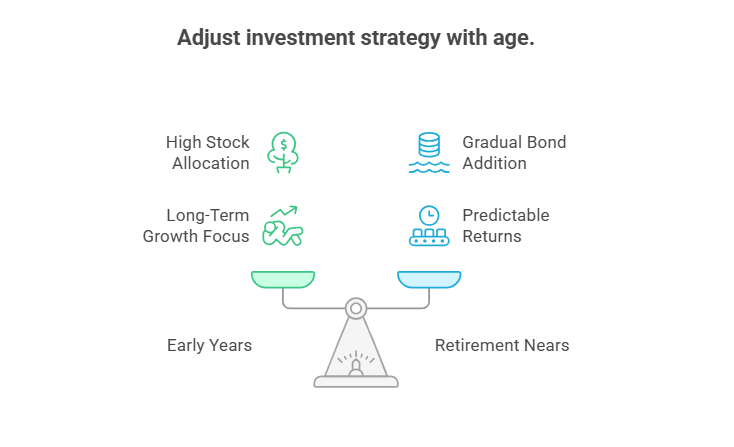

Stocks, Bonds, And More

Most experts advise us to focus on stocks in our early years to capture long-term growth (as Mesirow Financial points out). This can mean an 80 percent or even 90 percent stock allocation if you’re in your 20s or 30s. As retirement nears, gradually adding bonds can help buffer the ups and downs. We might also consider diversifying into real estate or annuities. For instance, a flexible premium deferred annuity can provide a predictable return akin to a bank CD when we’re not ready to draw income.

Handling Market Fluctuations

Timing the market based on headlines can be risky. Fidelity suggests that stocks often recover before the end of recessions, meaning if we bail out too soon, we could miss the rebound. Instead of scampering in and out, consider a bond ladder (where bonds mature at staggered intervals), or spread your money across various sectors, so you don’t rely on just one area for growth.

Protect Your Future Income

Smart Withdrawal Rates

In retirement, how we draw funds can matter just as much as how we invest. A common guideline from FINRA suggests withdrawing 3 to 5 percent each year, especially at the start of retirement. Adjusting for inflation is key so that we maintain purchasing power over time. If you’re exploring how to manage higher sums, you might be asking if you could retire at 60 with 2 million. The answer often hinges on your personal spending habits, expected returns, and how carefully your portfolio is structured.

Useful Tools And Strategies

Besides the typical stocks-and-bonds approach, adding fixed annuities for steady income or adopting specific insurance solutions can safeguard our nest egg. If you’re curious about different retirement investment approaches, we recommend checking out retirement investment options. For bigger decisions, we always weigh factors like tax efficiency, estate planning, and future goals, because we want our strategy to serve not just us but also the next generation.

Take The Next Step

Too often, we see well-meaning investors freeze at the idea of reallocating their assets or adjusting their withdrawal rate. We encourage a balanced approach that accounts for your timeline, helps you navigate inflation, and keeps your future spending goals in check. People often ask us five core questions about retirement asset allocation: how much to save, which investments to focus on, when to adjust, how to handle inflation, and whether they can maintain their lifestyle in retirement. These are crucial issues that deserve personalized attention.

Ultimately, allocating your retirement portfolio isn’t just about picking a few fancy funds. It’s about creating a plan that fits your vision of post-work life, helps you handle the unexpected, and keeps you moving toward the legacy you want to leave. If you’d like to explore more about retirement solutions, you can also visit our guide on how to buy retirement insurance. Here’s to maximizing our resources, preserving wealth for the long haul, and feeling confident every step of the way.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...