I remember the day I first asked myself, “How do I find my pension?” My mind raced with worries that I might have missed out on money I had rightfully earned. If you’re also questioning the status of a long-forgotten retirement plan, I hope my experience helps you track it down and reclaim what’s yours.

You might be asking five different questions in one breath: “Where do I start,” “How do I find a pension from an old job,” “Is my pension covered by PBGC,” “Do I need special documents,” and “Is my plan a multiemployer plan?” Let’s unravel it all step by step.

Begin My Search Online

My first move was to round up any documents hinting at a retirement account. Old pay stubs, company emails, or even tax returns might list a pension or 401(k). Once I gathered everything, I headed online.

- I tested my memory: Did I switch jobs 12 times like the average American, leaving behind multiple retirement accounts?

- I scanned official websites. The Pension Benefit Guaranty Corporation (PBGC) hosts a database of unclaimed retirement benefits (PBGC). I simply typed my last name and the last four digits of my Social Security Number to see if there was a match.

If your results come up empty, don’t panic! My name didn’t pop up on the first try either. I discovered that my plan was a multiemployer one, which meant PBGC might not hold my details. That’s when I knew I had to keep digging.

Contact Pension Regulators

When I realized my plan might not be directly insured by PBGC, I reached out to another crucial ally: the Department of Labor’s Employee Benefits Security Administration (EBSA). EBSA enforces retirement plan rules and offers guidance on lost or unpaid retirement benefits.

- EBSA’s hotline (1-866-444-3272) and their website (askebsa.dol.gov) shed light on retirement plan regulations.

- The Pension Rights Center also provides resources and explains federal laws that set limits on how much we can contribute to retirement accounts.

I learned that certain steps apply if a pension is divided at divorce or changed into an annuity via de-risking (a phase where employers shift pensions to insurance companies). EBSA helped me confirm which scenario applied to me.

Double-Check With Employers

I also tracked down old employers to verify whether they still held any of my retirement funds. Companies can move, merge, or rebrand, but a bit of detective work can pay off.

- I searched for human resources or benefits department contacts, sometimes emailing publicly listed addresses.

- If a company had dissolved, I’d look for any successor firm that might have taken over their retirement plans.

Many times, a standard termination means benefits get paid out or transferred elsewhere. If your old plan was terminated, PBGC’s “What to do before contacting PBGC” page can show you which documents you’ll need to continue your hunt.

Consider Professional Help

If you’re handling larger sums or more complex situations, an expert might be your best friend. A fee-only financial advisor or attorney can help untangle plan documents and clarify your options.

- The federally funded Pension Counseling and Information Program, sponsored by the Administration for Community Living, offers free legal help if you need extra support.

- You can also connect with a retirement plan advisor if the administrative side gets too overwhelming. They’ll point you in the right direction on withdrawals, tax efficiency, or the best way to integrate your pension into your broader portfolio.

My Biggest Retirement Lessons

Finally, after sorting through documents and contacting PBGC and EBSA, I pieced my pension story together. Here’s what I learned:

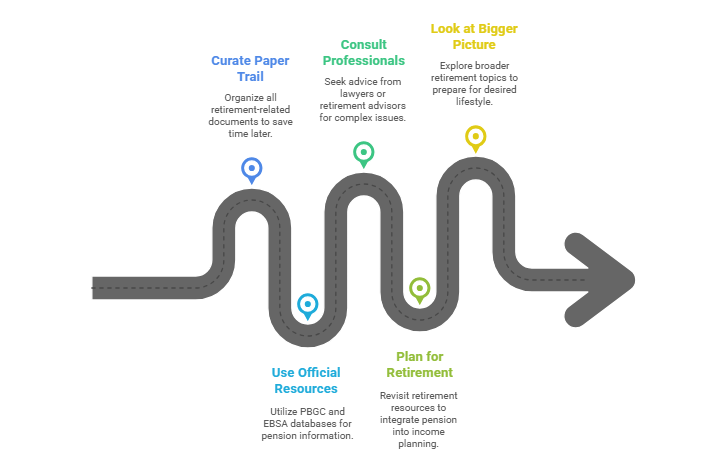

- Curate Your Paper Trail

Keep copies of every letter, pay stub, or statement referencing retirement benefits. Staying organized saves time later. - Use Official Resources

PBGC’s database is an excellent place to begin your search, especially if your plan went through a termination. EBSA also offers direct assistance for employee benefit questions. - Ask Professionals When Needed

For complicated matters, reach out to lawyers, CPAs, or specialized retirement advisors. You’ll feel confident that you’re not missing critical steps. - Plan Ahead for Retirement

It’s worth revisiting all your retirement resources once you’ve located an old pension. You might need to factor it into your retirement income planning or evaluate the best way to get income in retirement. - Look at the Bigger Picture

If you’ve found your pension, great! Next, why not see how to make money in retirement or explore how much money does a couple need to retire? These topics can help you prep for the lifestyle you want.

At the end of the day, there’s no single magic trick to finding lost retirement benefits. My journey was a combination of digital searches, phone calls, and good old-fashioned detective work. But once I saw that final statement confirming my pension, the effort felt totally worth it! If you’re still on the fence, I say go for it—comb through those files, dial a few numbers, and get one step closer to a comfortable, well-planned retirement.

Showcase your recognition by adding our award badge to your website! Simply copy the code below and embed it on your site to highlight your achievement.

Retirement Planners in Los Angeles to Consider

Los Angeles, a city synonymous with opportunity and innovation, is...

Retirement Planners in New York to Consider

Navigating the financial landscape of New York can be overwhelming,...