Many high-net-worth investors wonder, “Is Edward Jones a fiduciary for every account, do they consistently uphold a best-interest standard, how do fees factor into long-term costs, do certified advisors at the firm provide fiduciary-level advice, and what are the best next steps for verifying fiduciary status?” These questions reflect the complexities of fiduciary duty, especially for those seeking confidence in a financial advisor’s legal obligations. Below is an overview of what fiduciary responsibility means and how Edward Jones fits into that picture.

Understanding Fiduciary Duty

A fiduciary, as defined by the Consumer Financial Protection Bureau (CFPB), is legally required to place a client’s interests above all else. In the investment world, registered investment advisors (RIAs) typically follow this standard, known as the duty of loyalty and care, established by the Investment Advisers Act of 1940. These requirements ensure that a fiduciary cannot pursue personal gain at the expense of the client’s welfare.

Fiduciary obligations can also apply in nonprofit boardrooms or among corporate directors, who must protect stakeholders’ interests. In all situations, this standard is a vital check on conflicts of interest, guaranteeing that decision-makers remain aligned with those who rely on them.

Examining Edward Jones’ Role

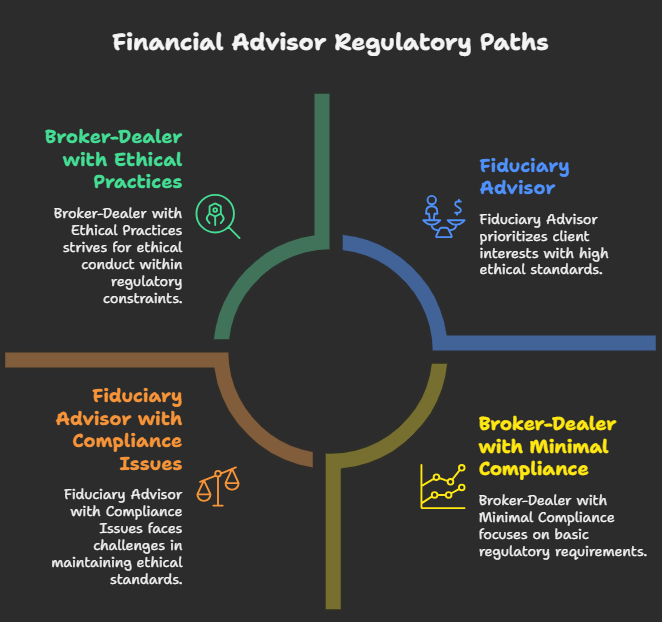

Edward Jones operates both as an RIA and a broker-dealer. When functioning as an RIA, advisors fall under a fiduciary standard regulated by the Securities and Exchange Commission. However, as a broker-dealer, the firm is subject to Regulation Best Interest (BI), which goes beyond previous suitability rules but does not always match the full fiduciary standard.

Some advisors at Edward Jones hold a Certified Financial Planner (CFP) credential, which requires adherence to fiduciary principles. Still, not every individual advisor at the firm must function as a fiduciary in every circumstance. This dual nature means that investors need to clarify which mode applies to their particular situation and whether any conflicts of interest might arise.

Regulation And Conflicts

Regulation Best Interest, introduced by the SEC in 2019, aimed to tighten broker-dealer conduct rules. Yet many critics argue that a consistent fiduciary benchmark for all financial professionals is preferable. Broker-dealers only have to demonstrate that an investment recommendation could benefit a client, while a fiduciary is obligated to place the client’s needs first at all times.

Edward Jones discloses that its compensation structure may create conflicts of interest. In other words, the firm’s revenue streams, including commissions, can affect which products advisors recommend. Investors can mitigate these conflicts by reviewing disclosures, verifying their advisors’ credentials, and learning more about how suggestions are formed before making large financial decisions. Potential conversation points can be explored at things to ask your financial advisor.

Exploring Fee Structures

Edward Jones has been noted for relatively high fees, particularly the 1.35% rate applied to Flex and Fund accounts. According to WallStreetZen, these fees can compound significantly over time, potentially reaching tens of thousands of dollars in total costs. While rates may drop as account balances grow, many high-net-worth individuals remain wary of expenses that might chip away at long-term returns.

Below is a simplified snapshot of how higher fees may add up:

| Account Value | Sample Advisory Fee | Potential Long-Term Effect |

|---|---|---|

| Under $250,000 | ~1.35% annually | Higher proportion of total return used for fees |

| Above $250,000 | Reduced percentage | Still considered high by industry standards |

High-net-worth families often prefer fee-only models to maintain transparency and reduce conflicts. Selecting an RIA that focuses on fiduciary duty can also reduce concerns about additional product commissions.

Considering Alternative Paths

Many ultra-high-net-worth investors look beyond large broker-dealer firms when seeking deep financial planning and wealth management. Some choose self-directed investing, focusing on low-cost index funds or exchange-traded funds (ETFs). Others explore robo-advisor platforms that automatically rebalance portfolios at a fraction of traditional advisory costs.

Hiring a professional with the CFP or CFA designation is another route for families who desire fiduciary-level advice. Local specialized help is often found by searching for a fiduciary near me to ensure personal guidance. Thoroughly choosing a financial advisor means verifying the person’s registration, credentials, and fee arrangement in detail. Those who prefer personalized service can also look into a certified trust and fiduciary advisor for more complex scenarios.

Reviewing Key Takeaways

Edward Jones might act as a fiduciary under certain conditions, particularly when its advisors serve under RIA rules or hold credentials like CFP. However, in broker-dealer roles, the firm abides by Regulation Best Interest and may not align with a strict fiduciary benchmark in every instance. Fee structures also play a major role. Investors who prioritize cost-effectiveness and ironclad fiduciary obligations should consider verifying the advisor’s status and comparing all available pathways.

By examining Edward Jones’ dual role, acknowledging the broader regulatory landscape, and exploring alternatives, high-net-worth individuals can feel more secure in their wealth management decisions. Focusing on fiduciary principles helps align any advice with long-term financial goals, ensuring that care, loyalty, and transparency are at the forefront of every recommendation.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...