I recently learned more than I ever imagined by working with a financial planner for small business owners. Before our first meeting, I assumed I just needed general investment advice. Instead, I discovered a guide who helped me manage my business finances, tax planning, and my personal retirement outlook in ways I hadn’t considered. Here’s my personal review of the experience.

My Search For A Planner

Finding someone who truly understands small business finances turned out to be quite a quest. I was juggling inconsistent income streams and had trouble separating personal and business accounts. According to Investopedia, many entrepreneurs keep up to 80% of their wealth tied up in their companies. That fact alone convinced me I needed specialized help, not just random pointers.

Why I Chose A Specialized Pro

I saw that financial planners who focus on small business challenges can help with cash flow projections, risk management, especially business-related insurance, and—even more important—tax avoidance pitfalls. I also discovered the CFP Board holds certified planners to a higher standard of care, which reassured me about ethical responsibilities. If you’re curious to understand more about the range of planner types, you might want to check out the types of financial advisors.

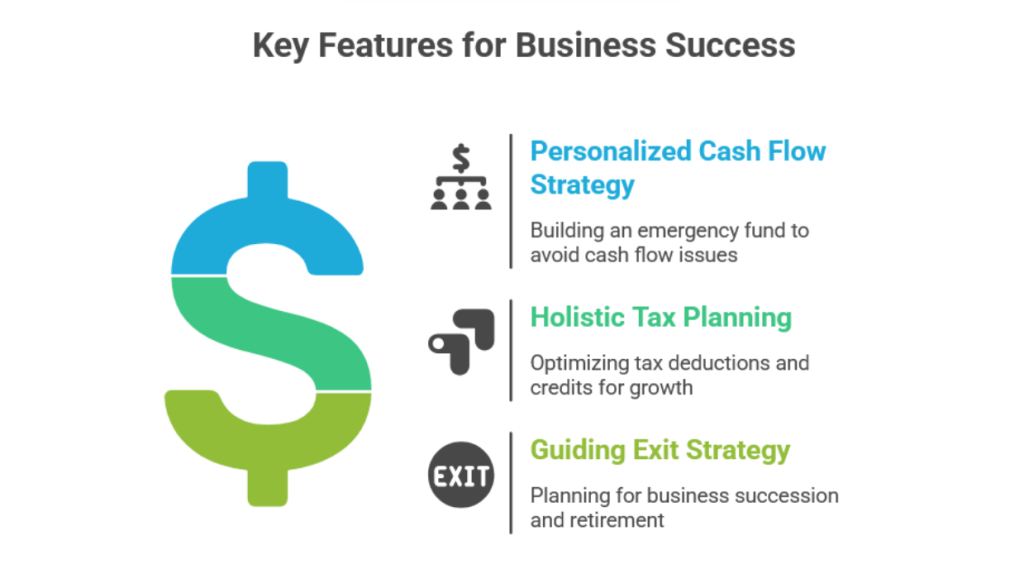

Key Features That Helped Me

After meeting my planner, I realized just how many money leaks can show up when you’re running a small operation. Below are some standout points I found most helpful.

Personalized Cash Flow Strategy

My planner introduced me to the practice of setting aside at least six months of operating expenses in an emergency fund. It felt impossible at first, but seeing the numbers on paper—and hearing about how 82% of business failures stem from poor cash flow management (based on a U.S. Bank study)—motivated me to start building that cushion.

Holistic Tax Planning

I knew taxes were complex, but I didn’t realize how much I could legally write off until I got a professional analysis. We reviewed everything from quarterly estimates to potential business credits. Instead of seeing a giant chunk of yearly expenses with no rhyme or reason, I now had a strategy that stayed aligned with my growth plan.

Guiding My Exit Strategy

I’m not selling my business next week, but I appreciated that my planner was already talking about exit and succession plans. Small business owners often rely on their eventual sale for retirement, but the stats show less than 30% of businesses on the market actually find buyers. Hearing that number made me realize I should also prioritize retirement accounts separate from the business.

Pros And Cons I Experienced

Not everything was picture-perfect, so here’s a quick snapshot of my experience:

| Aspect | My Take |

| Deep Expertise | Found out about hidden tax benefits, risk planning, and more |

| Personalized Attention | Enjoyed one-on-one sessions that targeted my business challenges |

| Higher Fees | Specialist planners may charge more than generic advisors |

| Ongoing Time Commitment | Meetings, paperwork, and check-ins can be time-consuming |

| Better Peace Of Mind | Confidence in a stable long-term plan made the effort worthwhile |

My Overall Verdict

So, was it worth it? Absolutely. I learned that bringing a pro on board let me focus on my real job—growing my business—while leaving the intricate money details to someone trained for exactly that. If you’re still wondering whether a specialized planner is right for you, consider reading about the financial advisor vs financial planner distinction to see which service better matches your goals.

When it comes to a financial planner for small business owners, you might have five common questions—how do they handle cash flow, are they certified by organizations like CFP Board, can they help with retirement, do they manage taxes, and what if you plan to sell your business?

Final Thoughts

Working with a planner took the burden of sifting through endless spreadsheets off my plate. Now I have ways to control my company’s cash flow, save for the future, and recover from unexpected curveballs. My biggest takeaway is that if you own a small business, the right financial partner is not a luxury—it’s almost a necessary safety net. And if you’re aiming for a relationship that lasts over the long haul, be sure to look for planners who understand the unique dance between personal wealth and business assets.

I hope my experiences shed some light on the value of partnering with an expert handpicked for a small business context. If you’ve ever considered getting professional guidance, go for it. My planner gave me the mix of confidence and structure that I wasn’t able to find anywhere else, and that combination has been game-changing in both my personal and business life.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...