Reflect On My Financial Outlook

I used to wonder if financial advisors are good for managing my high-net-worth portfolio. At first, it felt like a big leap to entrust someone else with my money decisions. But once I dove into their range of services, I realized they offer far more than simple stock picks.

You might wonder if financial advisors are good by asking: Are they worth the cost, do you need a certain net worth, can they help reduce taxes, do they offer personalized strategies, and how do you choose a reputable advisor? Those questions popped into my mind too. I soon learned that a good advisor can help with complex planning, taxes, and multi-generational strategies, which is precisely what I needed to secure my finances for the long haul.

Pinpoint My Specific Goals

The first thing I did was get crystal clear on what I wanted. Was I looking for help with estate planning, or did I just need someone to manage my stocks? Did I want tax-saving strategies, or was retirement my main focus?

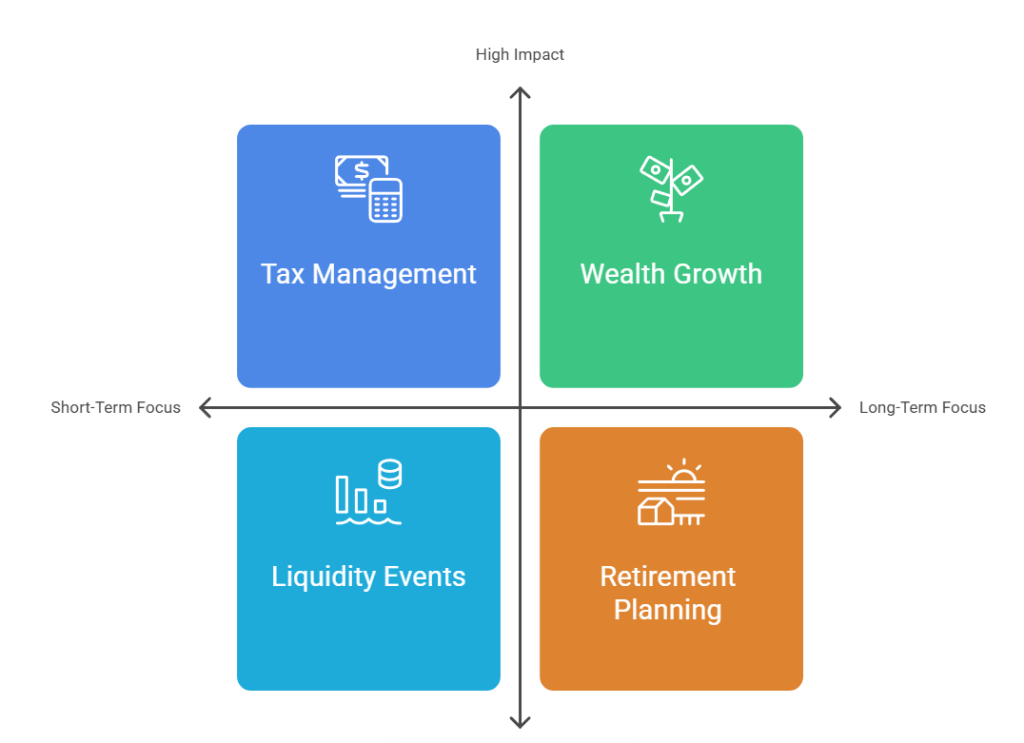

- I wrote down my key priorities: preserve my wealth, grow it over time, and keep my taxes in check.

- I listed any liquidity events on the horizon, like selling company stock or real estate.

- I also noted my preferred timeline. Was I aiming to retire in five years, or did I plan to continue working for the next decade?

By clarifying these points, I knew exactly what to ask potential advisors.

Check Fees And Value

Next, I looked into how various advisors structure their fees. I learned that many charge a fee based on assets under management (AUM). According to the 2024 Kitces Report, the median blended rate is around 1% on portfolios up to $1 million, gradually declining on larger balances (SmartAsset). Hourly arrangements can run about $300 per hour, while subscription-based planning often falls in the $4,500 range annually.

I compared those numbers to fees from robo-advisors, which range from 0.25% to 0.50% of AUM (SmartAsset). However, I wanted advanced strategies—like tax planning and estate coordination—so the human perspective felt valuable. If you want more insights on financial advisor pay scales, you might check out the average salary for financial consultant page.

Research Advisor Types

After nailing down fees, I explored the difference between fee-only and fee-based advisors. Fee-only means they earn no commissions, relying solely on client payments, so they tend to be more transparent about costs. Fee-based advisors might also earn income from commissions on certain products.

- Fee-only appealed to me because I wanted to avoid potential conflicts of interest.

- I also checked whether the advisor had a fiduciary obligation (a legal requirement to act in my best interest) or not.

If you’re not sure who qualifies as a fiduciary in your area, have a look at fiduciary near me. That search helped me confirm I was dealing with someone committed to my goals rather than pushing specific financial products.

Ask About Tax-Planning Support

I learned something important from an AssetMark study: 89% of clients want tax-planning advice, but only 25% get it (AssetMark). That means there’s a big opportunity to find an advisor who will truly dig into tax-efficient investment strategies. Personally, I needed guidance around timing of selling assets and leveraging charitable giving strategies to ease my tax load.

During my advisor interviews, I asked:

- Do you offer projections for future tax implications?

- How do you handle strategies like tax-loss harvesting and charitable gifting?

- Are you comfortable collaborating with CPAs or attorneys when needed?

Their answers showed me who had the expertise I was looking for and who just scratched the surface. If tax efficiency matters to you, it’s worth taking your time here.

Look For A Personalized Approach

I didn’t want a cookie-cutter, one-size-fits-all plan. I needed customization that factored in my personal goals, risk tolerance, and family dynamics. Top advisors, I discovered, often take a goals-based approach—like building a road map accounting for big life events (marriage, inheritance, or sale of a business). They are also adept at providing historical context when markets get bumpy, helping me stay calm and prevent impulsive decisions.

Here’s what I evaluated:

- How deeply they discussed my long-term vision, including transfers of wealth.

- Their comfort level with managing large positions in company stock (essential if you’ve got major liquidity events coming up).

- Their stance on consistent monitoring and communication.

If you’d like more structured tips on reviewing different advisors, check out the recommendations for choosing a financial advisor.

Wrap Up My Key Insights

Overall, I’ve found that a dedicated, fee-only fiduciary advisor has been indispensable in customizing strategies to fit my life. They helped me reduce unnecessary fees, manage my exposure to risk, and stay attuned to tax efficiencies. While the costs can be higher than a robo-advisor, the personal guidance and peace of mind were well worth it for me.

If you’re thinking of enlisting professional help, start by pinpointing your priorities and vetting an advisor’s fee structure and credentials. A solid advisor will keep your best interests in focus, offer robust tax and estate planning advice, and craft a plan tailored to you. With the right approach, you can feel confident that financial advisors are good partners in securing your long-term goals.

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...