Most people do not mess up their money because they are lazy or careless. They just do not know what they do not know. Between managing financial obligations, everyday expenses, and surprise bills like unexpected expenses, it is easy to make financial decisions that feel right in the moment but end up causing you to lose money or delay your path to financial success. The problem is not one bad purchase. It is the pattern of small mistakes that quietly drain your wealth, threaten your financial stability, and keep you from building lasting financial security.

If you want better financial health, it is not just about earning more. It is about making smarter choices with what you already have, avoiding traps like buying depreciating assets that lose value over time. That means recognizing common money pitfalls, breaking bad habits, and learning how to put your money to work for you. Whether you are trying to get out of debt, save for the future, or just stop feeling stressed every payday, avoiding these mistakes is the first step to taking control of your financial life.

Introduction to Financial Planning

Understanding the importance of financial planning is the foundation for achieving long-term stability and security. Without a clear plan, it’s easy to drift from paycheck to paycheck without making real progress. A solid financial plan helps you prepare for emergencies, reduce stress, and build a life where money supports your goals instead of holding you back.

Part of that plan means setting clear financial goals. Whether it is saving for retirement, paying off debt, or buying a home, knowing what you are aiming for makes it easier to make decisions and stay motivated. From there, creating a realistic budget is key. It helps you manage your monthly expenses, avoid overspending, and make sure your money is going where it matters most. Avoiding common mistakes such as not saving enough or relying too much on credit can make a huge difference. And if you are not sure where to start, getting advice from a financial professional can help you build a plan that fits your life and moves you closer to financial freedom.

31 Common Money Mistakes That Quietly Wreck Your Finances

Most people don’t go broke overnight. It happens slowly—one poor decision, one ignored habit, one missed opportunity at a time. If you’re serious about improving your financial health, you need to know what not to do just as much as what to do. Here are 31 common financial mistakes that can quietly drain your wealth, stall your progress, and keep you stuck:

1. Living Paycheck to Paycheck

When every dollar is spent before the next one arrives, you’re one emergency away from disaster. There’s no cushion, no breathing room, and definitely no plan. It creates constant stress and zero progress. Even a small buffer can change everything.

2. Not Tracking Your Spending

If you don’t know where your money’s going, you can’t control it. Most people underestimate how much they spend until they look. Tracking creates awareness, and awareness leads to better choices. It’s the easiest financial fix that most people skip.

3. Using Credit Cards to Fund Your Lifestyle

If you need debt to support your day-to-day life, you’re spending more than you earn. That gap adds up fast with interest. What feels like freedom now becomes a future headache. Use credit as a tool, not a lifeline.

4. Skipping an Emergency Fund

Emergencies aren’t rare—they’re just unpredictable. Without a backup plan, one surprise expense can wipe you out. A $1,000 buffer can prevent thousands in debt. It’s not exciting, but it’s essential.

5. Making Only Minimum Payments on Debt

Minimum payments keep you in debt forever. They’re designed to benefit the lender, not you. You’ll pay way more in interest than you realize. Paying extra, even a little, makes a big difference.

6. Not Saving for Retirement Early Enough

Waiting to save means you miss the power of compound growth. Time matters more than how much you contribute. The earlier you start, the less you need later. Procrastination is expensive.

7. Thinking Budgeting Is Optional

Without a budget, your money runs the show. Budgeting isn’t about cutting joy—it’s about telling your money what to do. It helps you avoid overspending and reach your goals faster. Clarity beats chaos every time.

8. Impulse Buying

Buying without thinking feels good in the moment and bad later. It’s often emotional, not logical. Over time, those small “treats” drain serious cash. Pause before you purchase. Ask yourself if it fits your goals or just your mood. Ten seconds of thinking can save you hundreds.

9. Relying on “Buy Now, Pay Later” Plans

These plans seem harmless, but they’re just debt in disguise. They make it easy to overspend and lose track. You’re committing future money you haven’t earned yet. That’s a slippery slope. You’ll barely feel the payments until they stack up. Convenience now, regret later.

10. Not Having Clear Financial Goals

If you don’t know what you want, you’ll waste money on what doesn’t matter. Goals give your money direction and purpose. Without them, progress is random. Specific targets create better habits. You can’t improve what you don’t measure. Goals turn hustle into results.

11. Trying to Look Rich Instead of Being Rich

Spending to impress others is a losing game. Real wealth is quiet—flashy spending often hides financial stress. Focus on assets, not appearances. Long-term peace beats short-term praise. No one cares as much as you think they do. Impress yourself, not strangers.

12. Borrowing Money for Things That Lose Value

Debt should buy value, not depreciation. Cars, gadgets, and vacations don’t grow your wealth. When you finance these things, you pay more for items that become worthless. It’s a costly habit. Use debt for investments, not indulgences. Buy things that make money, not just spend it.

13. Not Investing at All

Saving is safe, but it doesn’t grow fast enough. Inflation eats your cash if it’s just sitting. Investing builds wealth over time through compound growth. Waiting too long costs you more than bad timing. You don’t need to be a genius—just consistent. Starting is more important than being perfect.

14. Panic Selling Investments

When markets dip, emotions run high. Selling out of fear locks in your losses. Long-term investing means riding out the storms. Stay calm, stay invested. Timing the market rarely works. Patience pays way more than panic ever will.

15. Putting Off Estate Planning

No one likes to think about death, but avoiding it creates messes for your family. A will, insurance, and basic legal documents can protect everything you’ve built. It’s not just for the rich. It’s about responsibility. Even a simple plan is better than nothing. Protect your family from chaos.

16. Depending Too Much on One Income Source

If your one paycheck stops, everything falls apart. Multiple streams give you security and options. Even a small side income helps. Don’t put all your eggs in one basket. You’re more vulnerable than you think. A backup plan buys freedom.

17. Not Negotiating Your Salary

Most people leave money on the table by not asking. One raise compounds over years. You earn what you’re brave enough to request. Know your value and speak up. Even a small bump adds up. Closed mouths don’t get fed.

18. Ignoring Your Credit Score

Your credit score affects loans, rent, and even job offers. Bad credit makes everything more expensive. Checking it regularly helps you catch errors and improve. Don’t wait until you need it to fix it. It’s a silent reputation with real consequences. Protect it like your money depends on it—because it does.

19. Co-signing Loans for Others

You’re responsible if they don’t pay. It’s not just a favor—it’s a financial risk. Your credit, your money, and your stress are on the line. Think twice before saying yes. Most co-sign stories don’t end well. Help in other ways that don’t cost your future.

20. Underestimating Small Expenses

$5 here and $12 there feels harmless. But those “little” charges add up to hundreds each month. Review your spending and you’ll be surprised. Cutting small leaks creates big wins. Subscriptions, takeout, and fees are silent killers. Trim the fat without losing your lifestyle.

21. Not Setting Financial Boundaries with Friends or Family

Guilt spending can wreck your budget. Helping others is great, but not at your own expense. You can say no and still be supportive. Protect your own stability first. Your peace is more important than their short-term approval. Don’t go broke trying to be the hero.

22. Buying a House Before You’re Ready

Homeownership sounds smart, but it’s not always the right move. It comes with hidden costs, maintenance, and commitment. If you’re not financially stable, it becomes a burden. Rent while you prepare. There’s no shame in waiting. Owning at the wrong time costs more than renting at the right time.

23. Chasing Quick Money Schemes

If it promises fast riches, it’s probably a scam. You can’t shortcut experience or discipline. Most “get rich quick” traps end in loss. Build wealth the real way—slow and steady. Speed is sexy, but sustainability wins. Trust time-tested paths, not hype.

24. Avoiding Financial Conversations with Your Partner

Money silence leads to money fights. Being on the same page avoids stress and surprises. Set goals together and talk often. It builds trust and better decisions. Financial peace is a team sport. If you’re in it together, act like it.

25. Not Adjusting Your Budget When Income Changes

Earn more? Spend smarter. Lose income? Cut fast. A stagnant budget doesn’t reflect your real life. Keep it flexible and current. Life changes—your plan should too.

26. Falling for Lifestyle Inflation

More income doesn’t mean more spending. If your costs rise with your salary, you never get ahead. Keep your lifestyle steady and invest the difference. That’s how wealth is built. Don’t upgrade every time you level up. Let your money grow instead.

27. Skipping Insurance Coverage

Insurance feels unnecessary until you need it. Without coverage for your car, health, or home, one accident or unexpected expense can wipe out your financial stability. If you get in a car accident without insurance, for example, you could lose money fast and set back your progress. Paying a little now protects your financial security later.

28. Letting Fear Stop You from Starting

Waiting for the “perfect time” means you’ll never begin. Progress comes from doing, not overthinking. Start small and build. Action beats perfection. Every expert was once a beginner. You can’t win if you don’t play.

29. Confusing Wants with Needs

Be honest about what’s truly essential. That difference saves you thousands. Needs keep you alive—wants just make you feel better. Know the line and live below it. The more you control your desires, the freer you become. Simplicity builds wealth.

30. Not Learning About Money

Most schools don’t teach it, so you have to learn it yourself. Financial literacy is a superpower. Books, podcasts, mentors—pick one and start. What you know will shape what you grow. Avoiding it doesn’t protect you—it weakens you. Invest in knowledge, and everything else follows.

31. Blaming Your Income for Everything

It’s easy to say, “I just don’t make enough.” But many problems come from spending, not earning. Even small incomes can be managed well. Focus on control before chasing more. You don’t need six figures to build wealth—you need discipline. Master your current money first.

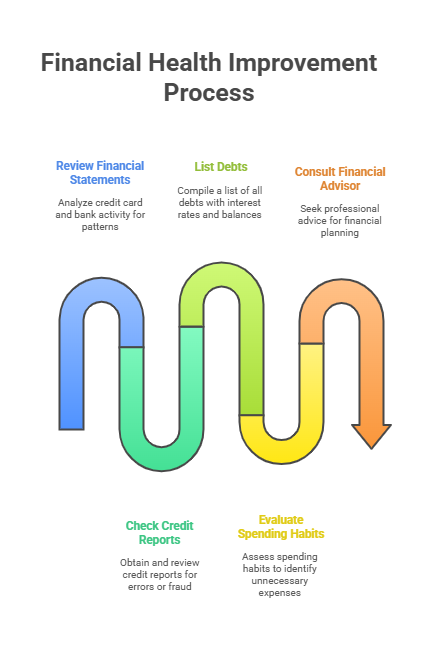

Assessing Current Financial Situation

Before you can fix your money, you need to know where it’s going. Most people avoid looking too closely, but this is where change starts. A few simple reviews can open your eyes to habits, leaks, and opportunities you’ve been missing. Here’s what to focus on:

- Review your credit card statements and bank activity. Go through at least the last 30 to 90 days. Spot any patterns—daily coffee runs, random Amazon splurges, subscriptions you forgot about. This isn’t about guilt—it’s about awareness. You can’t fix what you don’t track.

- Check your credit reports. You’re entitled to a free report from each bureau once a year at AnnualCreditReport.com. Look for errors, old accounts, or any signs of fraud. Identity theft can wreck your financial progress if you catch it too late. Make this a routine habit.

- List out all your debts. Include credit cards, student loans, car payments—everything. Knowing the interest rates and balances helps you prioritize what to tackle first. This step isn’t fun, but it’s necessary to build a real plan. Most people guess wrong on how much they owe until they see it in black and white.

- Evaluate your spending habits. Ask yourself: What are you spending on that doesn’t actually improve your life? Cut the fluff, not the joy. Often, trimming the excess gives you instant breathing room without feeling like a sacrifice. A few canceled expenses can unlock hundreds a month.

- Consider talking to a credit union or financial advisor. You don’t have to do this alone. Some professionals offer free or low-cost consultations to help you build a realistic plan. A second opinion might reveal options or strategies you never considered. It’s not a sign of failure—it’s a smart move.

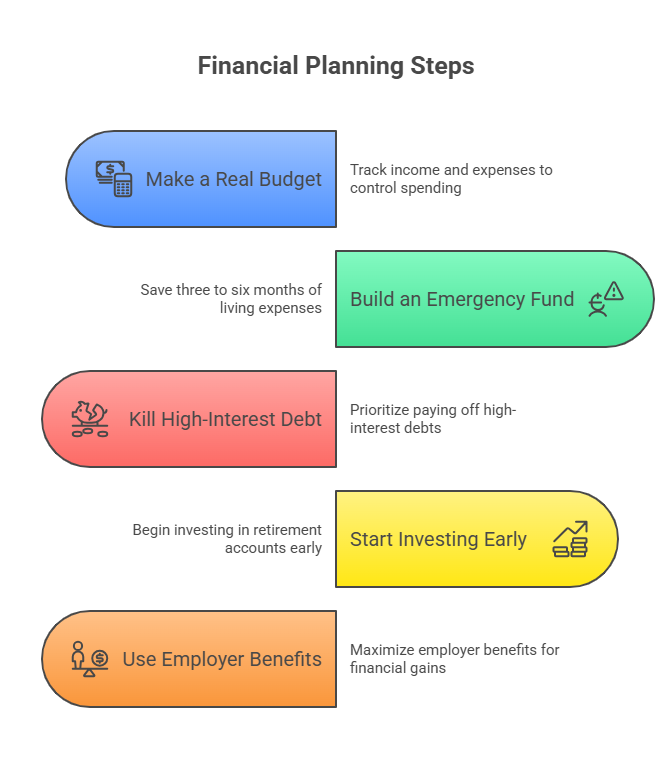

Building a Strong Financial Foundation

Getting your finances in order starts with mastering the basics. A strong foundation isn’t flashy — it’s stable, consistent, and sets you up for everything else. Before thinking about investing or growing your income, make sure these core habits are in place.

- Make a Real Budget

Your monthly budget should track every dollar you earn and spending money on essentials like rent, utility bills, food, and even streaming services. Including these helps you stay on top of your bills and avoid surprises. Setting up automatic payments for regular expenses ensures nothing gets missed, saving you from late fees or service interruptions. This budget isn’t about restriction but about control, helping you avoid impulse purchases driven by instant gratification and focus your money where it matters. - Build an Emergency Fund

Aim to set aside three to six months of living expenses as extra cash in a separate account. This fund acts as your safety net for unexpected events like medical bills, car repairs, or job loss. Having this cushion reduces the need to borrow or rely on credit cards when life throws curveballs. - Kill High-Interest Debt

Tackle high-interest debts first, like credit card balances. Clearing these frees up more money in your budget for saving and investing. It also reduces financial stress and improves your overall financial health. - Start Investing Early

Even small contributions to a retirement account, such as a Roth IRA or 401(k), matter. Thanks to compound growth, starting early builds wealth over time. Focus on steady progress instead of waiting for the perfect moment or big purchases that can derail your plan. - Use Employer Benefits

If your employer offers matching retirement contributions, make sure to take advantage. It’s like getting free money and boosting your savings effortlessly. Look out for all benefits you qualify for — combining these can lead to significant gains in the long run.

Taking Control of Debt and Credit

Debt isn’t a dirty word. It can be a tool if you manage it right but left unchecked it’s a trap. High-interest credit card debt is the first thing you want to tackle because it silently eats your budget. Create a plan that works for you whether that means paying down the highest interest first or knocking out the smallest debts for quick wins. Avoid common pitfalls like missing payments or late payments which can lead to costly late fees and cause serious financial problems down the line. Also, steer clear of risky shortcuts like payday loans or co-signing for friends because those moves can wreck your credit and cost you in the long run.

Your credit score matters more than most people realize. It’s not just about loans it affects everything from insurance rates to job prospects. One way to stay on top of your credit health is by regularly checking your free credit report for mistakes or fraud. Paying your bills on time keeping your credit card balances low and reviewing your credit report regularly are small habits that make a big difference over time.

Avoiding the Usual Money Traps

One of the fastest ways to tank your finances is by falling into common money traps. Overspending is easy when you don’t have a plan, and impulse buying can wreck even the best budgets. Get comfortable with delaying gratification — that means waiting before you buy something you want. It’s not about denying yourself but about spending smarter. Also, borrowing at sky-high interest rates like payday loans? That’s a quick way to make a bad situation worse.

Keep an eye on your financial accounts regularly. It’s surprising how often people miss recurring charges or errors on their credit reports. Catching these early can save headaches down the road.

Making Your Money Work for You

Saving alone won’t build wealth — investing is where the real growth happens. But don’t jump into the deep end blindly. Diversify your investments so you’re not putting all your eggs in one basket. Low-risk options like index funds or bonds might not be flashy, but they’re steady players over time. Tax-advantaged accounts like 401(k)s or IRAs give you a leg up, too, so don’t leave those benefits on the table.

Steer clear of anything that promises instant riches. True financial growth takes time, patience, and sometimes professional advice. A good financial advisor can help you build a plan that fits your risk tolerance and life goals, so you don’t have to guess.

Planning for the Long Haul

Long-term planning isn’t just about retirement — it’s about making sure your money lasts as long as you need it to. Setting up a solid retirement plan early gives you freedom later and peace of mind. This includes regularly putting money into a retirement account or retirement fund, which grows over time to support your future needs. Don’t forget to also keep some funds accessible in a savings account for emergencies or unexpected expenses.

Think beyond just retirement savings. Healthcare costs and potential long-term care expenses often catch people off guard, so factor those into your overall financial picture. Keep your plan flexible and review it at least once a year to adjust your goals, contributions, and investments as your life changes. Staying disciplined with your retirement savings is key — consistency over time will help you build a strong financial foundation for the future.

Bouncing Back from Setbacks

No one’s financial journey is perfectly smooth. Whether it’s a job loss, medical bills, or unexpected repairs, setbacks happen. That’s why an emergency fund is your best friend — it buys you time and keeps you out of debt. If things get really tough, don’t hesitate to reach out for professional help. A fresh perspective and expert advice can make a huge difference in bouncing back.

Keep Learning and Adjusting

Building a strong financial future isn’t about getting everything perfect right away. It’s about regular check-ins, small course corrections, and staying focused over time. This section covers the key habits that help you stay disciplined and keep moving in the right direction—even when life throws a few punches.

- Review your financial progress regularly.

Don’t just set goals and forget about them. Check your budget, debt, savings, and investments at least once a month. This helps you spot leaks early and make smarter adjustments while you still have time to course-correct. - Avoid money traps like overspending and under-saving.

These habits sneak up on you if you’re not watching. Use tracking tools or apps to see where your money really goes. The goal isn’t to deprive yourself—it’s to make sure your money aligns with what you actually care about. - Have a plan for financial setbacks.

Emergencies will happen. Job loss, medical bills, or family issues can hit hard. Having a backup plan—like an emergency fund or a list of expenses you can immediately cut—gives you peace of mind and a faster recovery. - Talk to a financial professional if you’re stuck.

There’s no shame in asking for help. A financial advisor can offer a fresh perspective, spot gaps in your plan, and help you make smarter long-term decisions. It’s especially useful when your goals start to get more complex. - Stay focused on long-term goals.

Big wins don’t happen overnight. Whether it’s paying off debt or retiring early, consistency beats intensity. Keep reviewing your progress, adjusting your plan, and showing up month after month. That’s how real wealth is built.

Stay Consistent, Stay in Control

Building a strong financial foundation isn’t about perfection—it’s about momentum. The small decisions you make daily, like checking your spending or putting aside a little more for savings, are what move you forward. When you build habits around reviewing your finances, avoiding common mistakes, and planning for the unexpected, you stay in control no matter what life throws your way. Consistency wins over time, even if the progress feels slow at first.

It’s not just about saving money—it’s about creating the kind of life you want. Financial freedom doesn’t happen overnight, but it does happen when you stay focused, keep learning, and adapt your plan along the way. Whether you’re just getting started or refining your strategy, keep showing up. The effort you put in now builds the freedom and options you’ll enjoy later.