I remember the moment I decided to start choosing a financial advisor. My portfolio felt scattered, and I wanted a pro who could help me turn random investments into a long-term strategy. It took me a while to find someone I trusted, but the peace of mind was worth every hour of research.

Below, I’ll walk you through how I did it, step by step. Think of it as a hands-on guide from one person who’s been there to another who’s ready to level up.

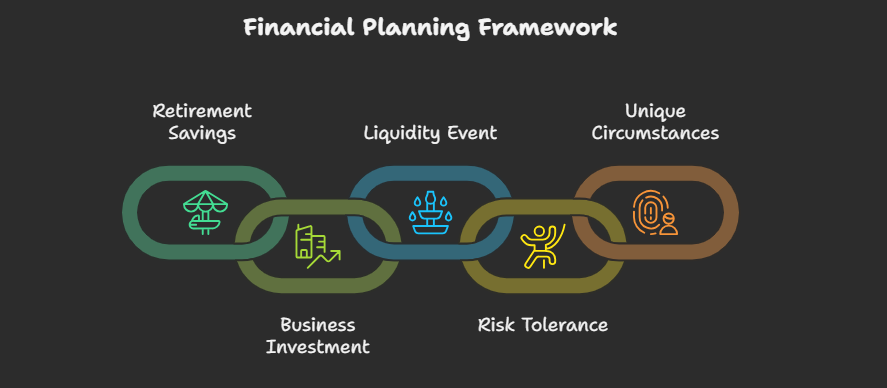

Define Your Financial Goals

Before you even look at specific advisors, nail down what you want to accomplish. Maybe you’re saving for retirement, planning a major business investment, or managing a recent liquidity event. Pinpointing your financial goals gives you a roadmap to share with any potential advisor.

- Make a quick list of immediate and long-term objectives.

- Decide how much risk you’re comfortable taking.

- Note any unique circumstances, such as concentrated stock holdings or family trusts.

Check Advisor Credentials

Next, dive into your advisor’s background. A reputable financial advisor should hold relevant licenses, like the Series 7 or Series 65, which allow them to sell securities or charge fees (Investopedia). You might also see designations like Certified Financial Planner (CFP) or Chartered Financial Consultant (ChFC). These signify extra training and mean they’ve met strict ethical standards.

- Ask how long they’ve been practicing and whether they advise high-net-worth families specifically.

- Check if they need to register with the SEC or a state regulator based on assets under management.

- Curious about the path to becoming an advisor? You can learn more about licensing in my earlier research on how to get financial advisor license.

Learn Their Investment Philosophy

An advisor’s investment approach should align with your goals and risk tolerance. Some focus on market capitalization strategies, while others prefer a contrarian or valuation-driven style (Forbes). If you want to emphasize social impact, look for an advisor who understands Socially Responsible Investing (SRI) (SmartAsset).

- Ask how they handle market ups and downs.

- Discuss whether they prefer active or passive funds.

- Find out if they tailor the approach to your time horizon or unique priorities.

Compare Fees and Costs

Financial advisor fees come in different shapes: assets under management (AUM), flat retainer, hourly rates, or one-time planning fees (NerdWallet). Here’s a quick snapshot:

| Fee Structure | Typical Range |

|---|---|

| Assets Under Mgmt | 0.25% to 2% of portfolio |

| Hourly Rate | $200 to $400 per hour |

| Flat Fee | $1,000 to $3,000 |

| Annual Retainer | $2,000 to $7,500 per year |

Some advisors charge commissions too. Make sure you understand what you’re paying for. If you need ongoing estate-planning guidance, a simple one-time plan fee may not cover all you want. Also, keep the new SEC marketing rule in mind, because it influences how advisors can advertise or show performance data (DWT).

Assess Communication Style

Communication is huge when you’re handing over large sums for someone else to manage. Will you get quarterly check-ins, monthly updates, or just a year-end report? Frequent updates can ease your mind, especially if the market gets choppy (Fidelity Bank Wealth Management Advisor).

- Ask how they’ll share performance and when.

- Find out if they prefer face-to-face or virtual meetings.

- Check if they offer education and resources so you understand your investments.

Clarify Collaboration Approach

Some individuals enjoy being hands-on, while others want an advisor to handle everything. I learned early on that I like to be in the loop, but I also appreciate having an expert to bounce ideas off. For me, that meant choosing an advisor open to frequent discussions about my changing needs.

- See if they’re comfortable working with your accountant or estate attorney.

- Determine whether they take charge of daily decisions or discuss every trade first.

- If you’re seeking a fiduciary, confirm their legal obligation to act in your best interest or learn more by searching for a fiduciary near me.

Make Your Decision

Finally, gather everything you’ve learned and pick the advisor who feels right. If you still have doubts, consider a trial run or a short-term plan before fully committing. It’s okay to interview multiple advisors and request references. After all, you’re entrusting them with your financial future.

If you’re still uncertain about choosing a financial advisor, you might be asking: “How do I track down an advisor with the right specialty,” “Are fees negotiable,” “Do I need to share all my finances,” “Which licenses matter most,” or “Should I start if I’m close to retirement?” I’ve asked all these questions too, and my best advice is to keep digging until you’re confident in your choice.

I hope my journey makes the process feel less daunting. You deserve an advisor who values you, communicates often, and helps you achieve your goals. Once you find that person, it’s a real game-changer. Good luck on your path to financial freedom!

Financial Advisors in Los Angeles to Consider

Finding the right financial advisor can be a pivotal step...

Financial Advisors in New York to Consider

Selecting the right financial advisors in New York can play...